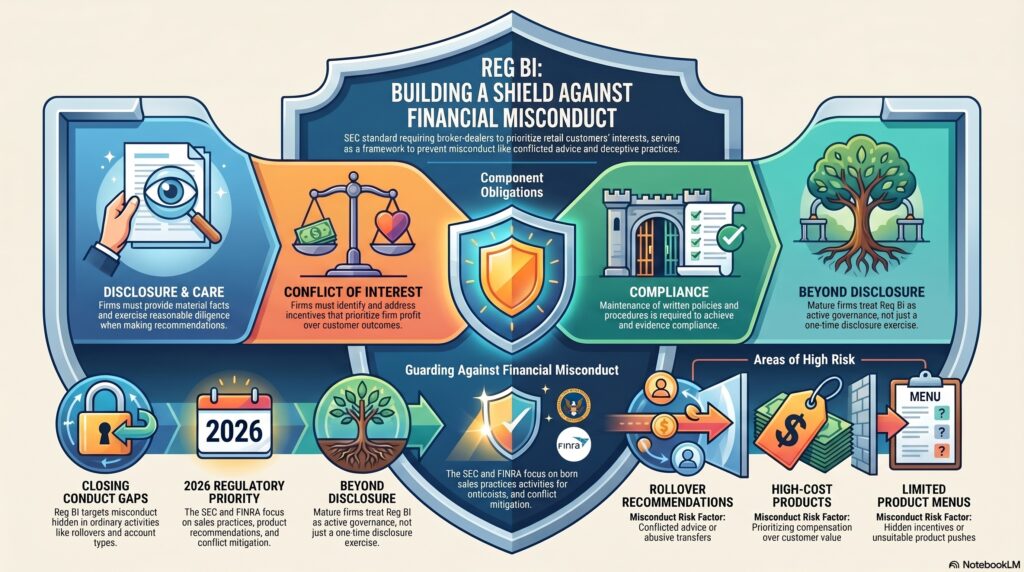

Regulation Best Interest (Reg BI) is the U.S. Securities and Exchange Commission standard of conduct that applies when a broker-dealer or associated person makes a recommendation to a retail customer involving a securities transaction or investment strategy, including recommendations about account type. FINRA’s current Reg BI overview states that the rule establishes a “best interest” standard of conduct for broker-dealers and associated persons under the Securities Exchange Act of 1934.

In the financial crime environment, Reg BI is significant because it strengthens the conduct, conflicts, and supervisory framework around retail recommendations. It is not an AML rule in the narrow sense, but it is highly relevant to financial crime because many harmful schemes, unsuitable recommendations, conflicted product pushes, and deceptive sales practices sit at the boundary between conduct failure and financial misconduct. A weak recommendation framework can expose customers to fraud, conflicted advice, abusive rollovers, opaque products, or misleading account arrangements, all of which can create customer harm and erode trust in securities markets. This is an inference supported by Reg BI’s investor-protection purpose and FINRA’s supervisory treatment of the rule.

From a professional perspective, Reg BI is best understood as a retail investor protection rule focused on recommendation conduct. FINRA explains that Reg BI requires broker-dealers and associated persons to act in the retail customer’s best interest at the time a recommendation is made, without placing the financial or other interest of the firm or associated person ahead of the customer’s interests. That matters in the financial crime environment because misconduct often arises when firms or individuals prioritize compensation, product placement, account retention, or internal incentives over fair customer outcomes.

Watch on YouTube: Regulation Best Interest (Reg BI)

A core feature of Reg BI is that it is built around four component obligations: Disclosure, Care, Conflict of Interest, and Compliance. FINRA’s Reg BI materials and SEC guidance both frame the rule through those obligations. In practical terms, this means firms must provide material facts about the recommendation and relationship, exercise reasonable diligence and care, identify and address conflicts, and maintain written policies and procedures reasonably designed to achieve compliance.

This has direct financial-crime relevance because conflicts and weak supervision are common enablers of misconduct. If firms fail to identify incentive conflicts, fail to review recommendations properly, or allow product and account recommendations that benefit the firm ahead of the customer, the result may not always be classic fraud in the criminal sense, but it can still create serious misconduct risk and customer harm. The SEC’s FY 2026 Examination Priorities state that examinations will continue to focus on broker-dealer sales practices related to Reg BI, including product and investment-strategy recommendations, account and rollover recommendations, conflict identification and mitigation, and review processes.

That supervisory focus matters because Reg BI is a live control area, not a historical implementation project. FINRA’s 2026 Annual Regulatory Oversight Report includes a dedicated Reg BI and Form CRS topic to inform member firms’ compliance programs, and the SEC continues to prioritize Reg BI in examination work. This shows that regulators still view recommendation conduct, conflicts management, and supervisory implementation as active areas of risk.

In the financial crime environment, Reg BI is especially relevant where misconduct hides inside apparently ordinary brokerage activity. Recommendations about rollover accounts, higher-cost products, limited product menus, or account types may not look like fraud on the surface, but can still reflect conflicted, unsuitable, or harmful conduct if the firm’s incentives or controls distort the recommendation process. The SEC’s FY 2026 priorities specifically highlight conflicts in recommendations involving accounts, rollovers, and limited product menus.

A mature firm therefore treats Reg BI as more than a disclosure exercise. It requires recommendation governance, conflict management, supervision, training, and evidence of compliance. FINRA’s materials emphasize that member firms should build their compliance programs around the rule’s obligations, and its annual oversight reporting is intended to help firms identify findings and strengthen controls. In a wider financial crime sense, that helps reduce the space in which conflicted retail conduct can become abusive, deceptive, or harmful.

Ultimately, Regulation Best Interest matters in the financial crime environment because it helps shape the standards for how broker-dealers recommend securities transactions and strategies to retail customers. It does not replace AML, anti-fraud, or market-abuse rules, but it strengthens the conduct and conflicts framework that helps prevent retail harm, deceptive sales practices, and recommendation-driven misconduct. For that reason, Reg BI should be understood as a core investor-protection and supervisory rule with real relevance to the broader control environment for financial misconduct.