Payment screening is the process of reviewing payment messages and related transaction data to identify whether a payment involves a sanctioned person, prohibited counterparty, restricted jurisdiction, or other financial crime concern before or during processing. In practice, it is most closely associated with sanctions compliance, but it also supports broader transaction transparency and risk management. OFAC’s sanctions guidance and Wolfsberg’s payment transparency standards both make clear that transparent payment data is essential for sanctions screening and for identifying unusual or suspicious activity.

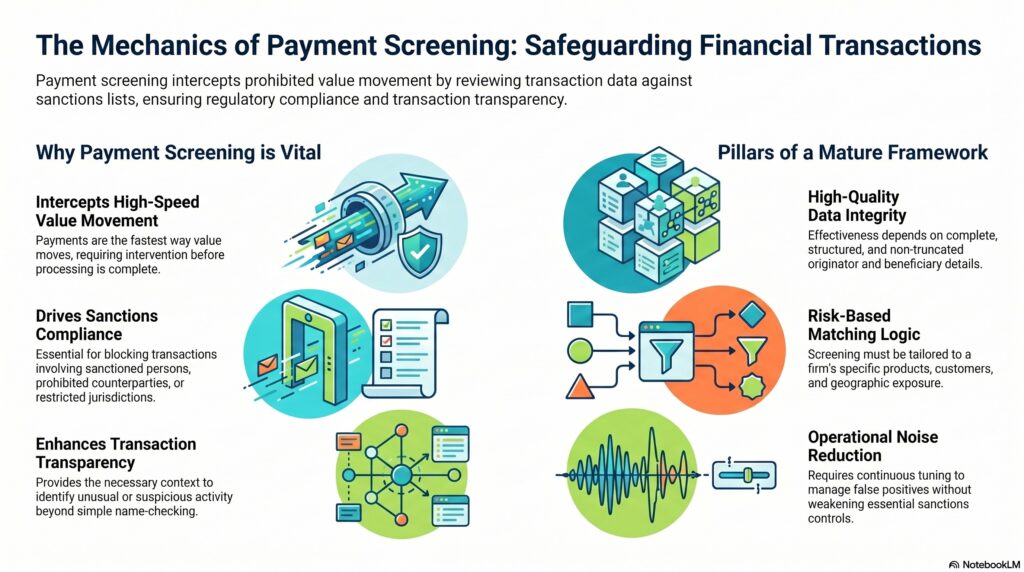

In the financial crime environment, payment screening matters because payments are one of the fastest and most direct ways value moves through the financial system. If a firm cannot identify who is sending funds, who is receiving them, what jurisdictions are involved, and whether any of those parties are restricted or suspicious, it may process prohibited or high-risk transactions before intervention is possible. OFAC states that sanctions can require blocking or prohibiting transactions involving targeted persons, countries, or sectors, which is why payment screening sits at the center of many sanctions-control frameworks.

From a professional perspective, payment screening is not just “name checking.” A mature screening framework looks at parties, counterparties, banks, jurisdictions, narratives, and payment attributes across the payment chain. That includes originator, beneficiary, intermediary institutions, and other related parties where the payment format supports that information. Wolfsberg’s payment transparency standards emphasize that payment transparency is necessary not only for sanctions screening but also for transaction monitoring, because it enables firms to understand the parties and context behind the transfer.

Watch on YouTube: Payment Screening

This is why payment transparency and payment screening are closely linked. Screening quality depends heavily on the quality and completeness of the data inside the payment message. If originator or beneficiary details are truncated, missing, inconsistent, or poorly structured, the screening process becomes weaker and the firm may miss a true sanctions hit or fail to understand suspicious movement of funds. Wolfsberg’s recent guidance specifically links transparency to the ability to screen payments effectively against sanctions lists.

Payment screening is especially significant in instant and real-time payment environments. OFAC’s guidance for instant payment systems notes that these systems have unique characteristics and that financial institutions should adopt a risk-based approach to sanctions compliance in light of the speed and immediacy of such payments. In practical terms, faster payment rails reduce the time available for manual intervention, which increases the importance of strong front-loaded screening, data quality, and escalation logic.

A professionally mature payment-screening framework therefore depends on several elements working together. It needs accurate and current sanctions data, appropriate matching logic, clear rules for handling potential matches, timely escalation, and good integration with payment operations. It also needs to reflect the firm’s products, customers, geographies, and transaction volumes. OFAC’s Framework for Compliance Commitments states that a risk-based sanctions compliance program should take account of a company’s customers, products, services, transactions, and geographic locations.

False positives are a major operational issue. Payment screening systems often generate alerts on names or locations that resemble sanctioned parties but prove unrelated after review. Some level of false positives is unavoidable in any meaningful screening process, but excessive noise can overwhelm analysts and delay decision-making. This is why firms need tuning, quality assurance, and review processes that improve precision without weakening sanctions compliance. This is an inference supported by the broader OFAC risk-based framework and Wolfsberg’s emphasis on effective payment transparency and controls.

Payment screening also overlaps with broader transaction monitoring and financial crime controls. A payment may not trigger a sanctions match and still be suspicious because of unusual routing, inconsistent counterparties, rapid pass-through behavior, or unexplained high-risk geography exposure. Wolfsberg explicitly notes that payment transparency supports both sanctions screening and transaction monitoring to identify unusual or suspicious activity. That means payment screening should not be treated as a standalone filter isolated from AML and fraud functions.

Ultimately, payment screening is a core control in the financial crime environment because it helps firms decide whether a payment can be processed lawfully and safely. It protects against sanctions breaches, supports transaction transparency, and strengthens the institution’s ability to detect suspicious fund movement before value is transferred. For that reason, payment screening should be understood not just as a technical filter, but as one of the key control points where payments operations and financial crime prevention meet.