An originator is the person or entity that initiates a payment or transfer of funds. In ACH payments, Nacha defines the originator as the consumer, business, or entity that agrees to initiate transactions into the payment system, and in wire-transfer standards FATF explains that the originator is the account holder who requests the transfer, or, where there is no account, the natural or legal person that places the order with the ordering institution.

In the financial crime environment, the originator is significant because originator information is central to payment transparency, traceability, sanctions screening, fraud detection, and AML controls. A payment instruction is much harder to assess if the institution cannot establish who actually initiated it, on whose behalf it was sent, and whether that person or entity is consistent with the account, relationship, or stated transaction purpose. FATF’s wire-transfer guidance is built around this principle, which is why Recommendation 16 focuses so heavily on complete originator and beneficiary information accompanying transfers.

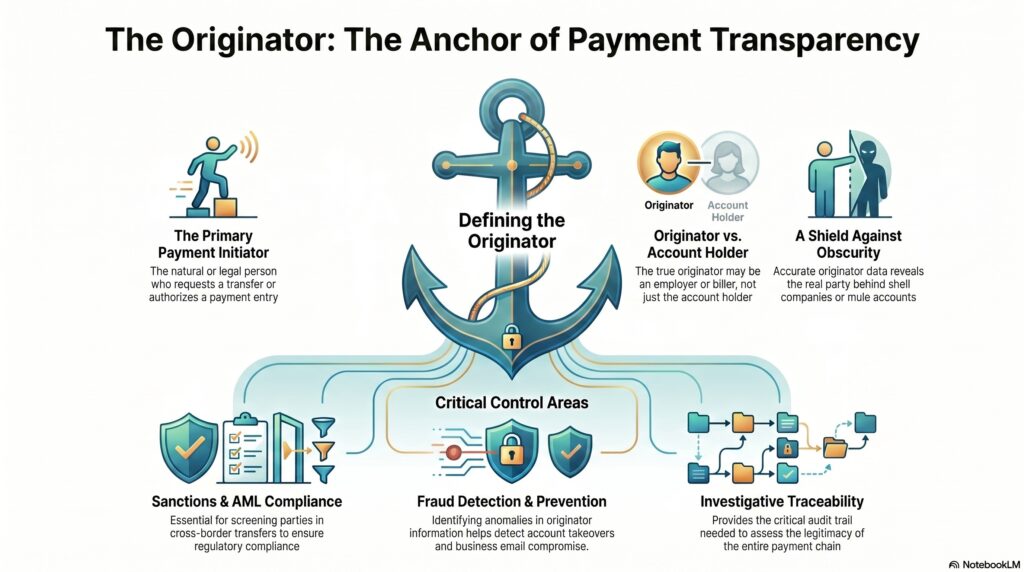

From a professional perspective, the originator concept matters because it answers one of the most important operational questions in payments: who is really sending the money? That is not always as simple as identifying the account number from which funds are debited. In some contexts, the originator may be the account holder. In others, it may be a business, employer, biller, or payment initiator acting through a bank or third-party sender. Nacha’s ACH materials make this clear by describing the employer in direct deposit as the originator and the bank as the ODFI.

Watch on YouTube: Originator

This distinction is highly relevant in the financial crime environment because criminals often try to obscure the true originator of funds. They may use mule accounts, third parties, shell entities, compromised accounts, or layered payment arrangements so that the visible account holder and the real initiating party are not the same in substance. That is why originator information is not just a formatting requirement in a payment message. It is a core part of understanding whether a payment is legitimate, suspicious, or prohibited. This is an inference supported by FATF’s emphasis on originator information in wire-transfer transparency.

Originator information is especially important in cross-border wire transfers. FATF’s revised explanatory note for Recommendation 16 says that originator refers to the account holder requesting the wire payment or value transfer from that account, or, where there is no account, the person placing the order with the ordering institution. The purpose of this standard is to ensure payment chains carry enough information to support sanctions compliance, suspicious activity detection, and investigative traceability across jurisdictions.

It is also important in ACH and domestic payments. Nacha’s rules and educational materials define the originator in relation to the party authorizing the ODFI to send entries to the receiver’s account. That matters because many domestic fraud and AML questions depend on whether the originator is genuine, properly authorized, and behaving consistently with the customer relationship. A valid account debit or credit can still be problematic if the apparent originator is acting without authority, using deceptive authorization, or fronting for another party.

For financial institutions, the practical significance of the originator lies in several control areas. One is screening and sanctions compliance, because the institution needs to know who is sending the funds. Another is fraud prevention, because originator anomalies may indicate account takeover, business email compromise, ACH abuse, or unauthorized payment initiation. A third is AML monitoring, because repeated transfers from inconsistent or obscured originators may suggest layering, mule activity, or misuse of payment channels. These are professional inferences grounded in the transparency purpose of FATF’s originator requirements and Nacha’s definition of who initiates ACH entries.

Ultimately, the originator is a foundational concept in the financial crime environment because it identifies the party at the start of a payment chain. Without reliable originator information, firms lose a critical part of the audit trail needed to assess legitimacy, detect suspicious activity, comply with sanctions obligations, and support investigations. For that reason, “originator” should be understood not as a minor payment-field label, but as one of the key anchors of payment transparency and financial crime control.