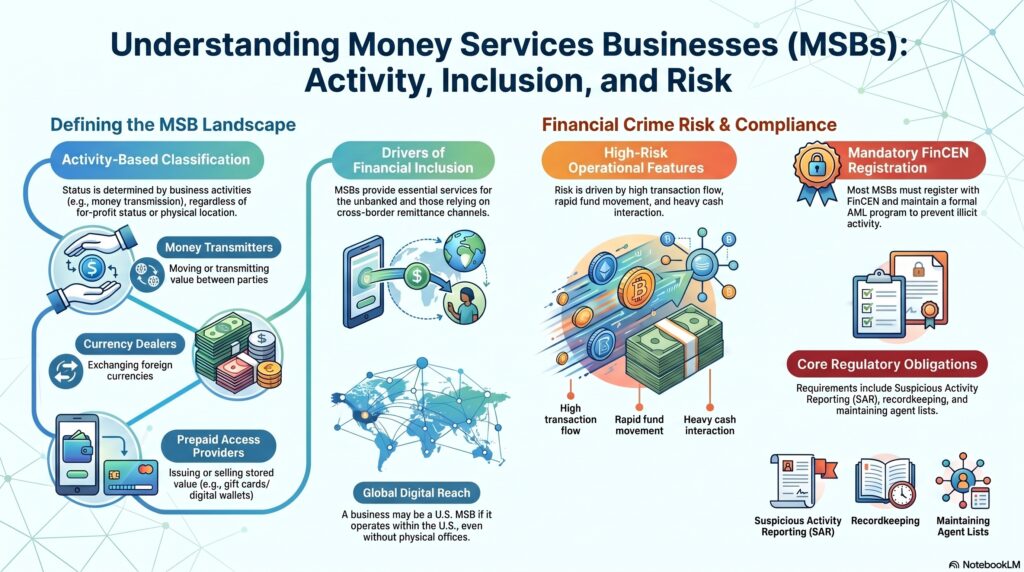

A Money Services Business (MSB) is a category of non-bank financial business under the U.S. Bank Secrecy Act framework. FinCEN and the eCFR define an MSB by activity, not by what the firm calls itself, and the definition includes businesses engaged in one or more regulated capacities such as dealer in foreign exchange, check casher, issuer or seller of traveler’s checks or money orders, provider or seller of prepaid access, money transmitter, and the U.S. Postal Service in specified respects. FinCEN also states that if a business is an MSB, it must comply with BSA requirements applicable to MSBs.

In the financial crime environment, MSBs are significant because they provide services that move, convert, store, or transmit value outside the traditional bank model. That makes them commercially important, especially for remittances, currency exchange, check cashing, and other services used by customers who may not rely on conventional banking channels. FinCEN has expressly noted that MSBs play an important role in a transparent financial system, particularly because they often serve people less likely to use traditional banking services and because of their role in remittance activity.

From a professional financial crime perspective, the importance of an MSB lies in the combination of high transaction flow, rapid movement of funds, cash interaction, and cross-border utility. Those features are commercially legitimate, but they can also create exposure to money laundering, fraud, structuring, sanctions evasion, and terrorist financing if controls are weak. The FFIEC BSA/AML materials identify MSBs as a distinct non-bank financial institution category with specific AML relevance, and FinCEN’s rules require each MSB to maintain an AML program reasonably designed to prevent the business from being used to facilitate money laundering and terrorist financing.

Watch on YouTube: Money Services Business (MSB)

A key professional point is that MSB status depends on what the business does, not on whether it is licensed, incorporated in a particular way, or even operating for profit. FinCEN’s 2011 clarification states that it is the activities performed that cause a person to be categorized as an MSB, and that this does not depend on factors such as whether the person is licensed as a business, has employees, or is engaged in a for-profit venture. That activity-based approach matters because firms can fall within the MSB perimeter even where they do not think of themselves as traditional money transmitters or exchange businesses.

This is why MSBs are a major focus for AML compliance and registration. FinCEN’s MSB registration materials state that businesses falling within the definition generally must register, and the regulations impose additional obligations such as AML programs, suspicious activity reporting, agent-list obligations where applicable, and other recordkeeping and reporting requirements. In practical terms, an MSB is not simply a payments business; it is a regulated financial institution category under the BSA.

MSBs are also important because they often sit close to cash, remittances, and prepaid value, all of which can create heightened financial crime risk depending on the product and customer base. The FFIEC notes that MSBs include providers or sellers of prepaid access, and prepaid access itself is identified as an MSB-relevant risk area. In operational terms, this means firms dealing with MSBs, or operating as MSBs, need to assess not only customer identity and activity but also the design of products, channels, and agent relationships through which value is moved.

Another critical issue is that MSB exposure can be cross-border. FinCEN has clarified that a person may qualify as an MSB based on activities within the United States even if none of its agents, agencies, branches, or offices are physically located in the United States. That matters because digital and cross-border value movement can bring a business into the U.S. MSB framework without a conventional physical footprint.

For financial institutions that bank MSBs, the issue is not that MSBs are inherently improper, but that they are a customer type requiring strong due diligence and monitoring. FinCEN’s 2014 statement made clear that banking organizations can serve the MSB industry while meeting their BSA obligations, which is important because MSBs provide legitimate services and are part of the regulated financial ecosystem. The real question is whether the MSB’s business model, controls, customer base, geography, and transaction patterns are properly understood and risk-managed.

Ultimately, an MSB is a legally defined non-bank financial institution category that plays an important role in payments and value transfer, but also carries distinct AML and financial crime risks because of the services it provides. In the financial crime environment, MSBs should be understood as both legitimate financial-service providers and high-relevance control subjects requiring registration, AML governance, suspicious activity controls, and proportionate supervision.