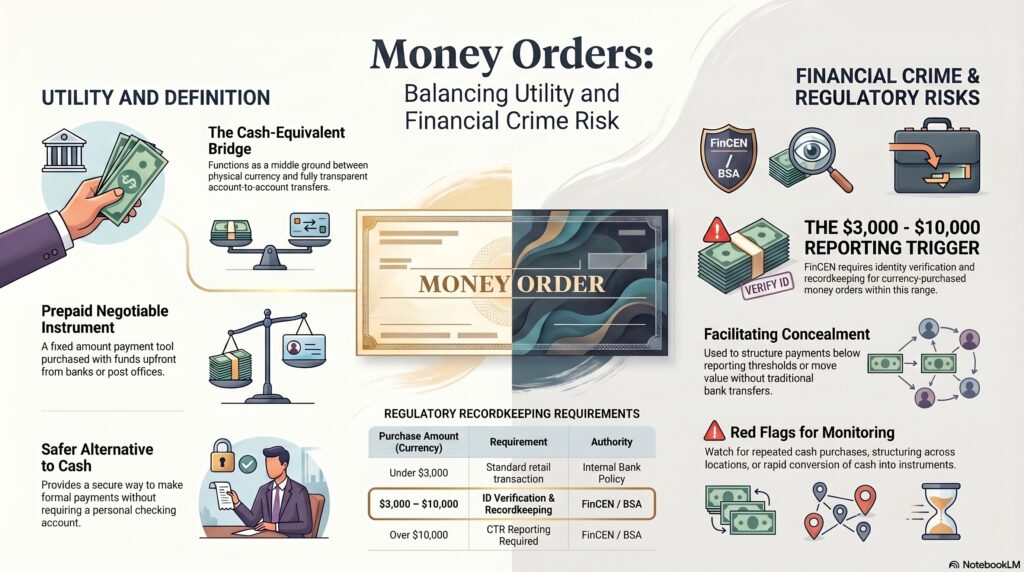

A money order is a prepaid negotiable instrument used to make a payment for a fixed amount. USPS describes money orders as a safer alternative to cash and personal checks, and Cornell’s Legal Information Institute defines a money order as a prepaid negotiable instrument that can be purchased from banks, post offices, and other businesses, usually subject to face-value limits.

In the financial crime environment, money orders matter because they sit between cash and fully account-based payments. They are legitimate and widely used, but they can also be attractive in fraud and money-laundering contexts because they can convert cash into a more portable, more acceptable, and sometimes less transparent payment instrument. Under the U.S. BSA framework, certain money orders are included within the broader regulatory concept of monetary instruments, which is why they appear in AML recordkeeping and reporting rules.

Watch on YouTube: Money Order

From a professional perspective, the significance of a money order is not that it is inherently suspicious. The significance is that it can be used as a cash-equivalent instrument in ways that reduce immediate visibility compared with ordinary account-to-account transfers. FinCEN guidance states that financial institutions must verify identity and retain records before issuing or selling money orders purchased with currency in amounts between $3,000 and $10,000 inclusive, which reflects the recognized AML risk in this product category.

Money orders are therefore relevant in several financial crime scenarios. They may be used to make payments that appear more secure or more formal than cash, to structure purchases below reporting thresholds, to fund scams, or to move value across parties without using a traditional bank transfer. They also appear in fraud schemes where victims are sent fraudulent money orders or persuaded to purchase and send them. The FFIEC’s red-flag materials emphasize that banks should look for suspicious patterns associated with money laundering and terrorist financing, and money-order activity can be part of those patterns when it is inconsistent with customer profile or economic purpose.

For firms, the control issue is usually context. A money order purchased for a normal personal payment may present little concern. Repeated purchases with currency, use by customers with no clear legitimate need, structuring across multiple locations or days, or rapid conversion of cash into negotiable instruments can all increase risk. Because money orders can function as a bridge between cash and negotiable payment, they remain operationally important in AML, fraud, and customer-risk monitoring even though they are an older payment product.

Ultimately, a money order is a legitimate prepaid payment instrument, but in the financial crime environment it is also a product that can facilitate concealment, structuring, and movement of value if controls are weak. For that reason, money orders should be understood not just as a retail payment convenience, but as a payment instrument with specific AML and fraud-control relevance.