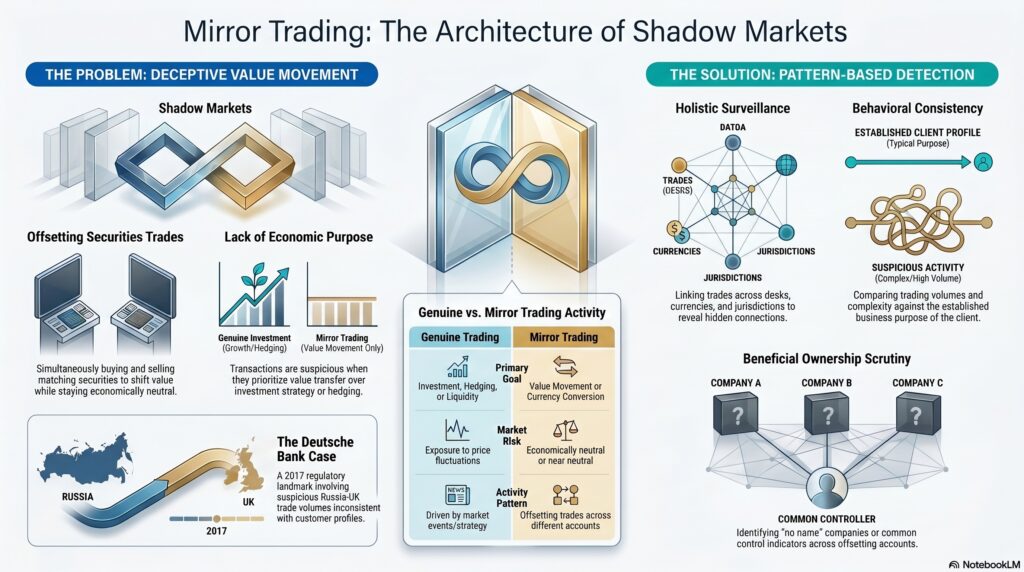

Mirror trading is a trading pattern in which one party buys a security in one market or account while another party simultaneously or near-simultaneously sells the same or a closely matching security in another market or account, so that the trades offset economically while value is shifted across entities or jurisdictions. In regulatory and AML contexts, it is often discussed as a technique that can be used for concealed currency conversion, capital movement, or laundering through securities transactions rather than for genuine market exposure. FINRA’s AML guidance lists “mirror trades or transactions involving securities used for currency conversions, potentially through the use of offsetting trades” as a red flag.

In the financial crime environment, mirror trading matters because it can make illicit fund movement look like legitimate trading activity. Instead of transferring funds directly from one party or jurisdiction to another, the actors use offsetting securities trades to create the appearance of ordinary market transactions while achieving a non-market objective, such as moving value, changing currency, obscuring beneficial ownership, or distancing funds from their origin. The FCA’s 2025 review on money laundering through markets states that money laundering through markets is the use of capital markets to launder funds so they appear legitimately generated from trading activity, and it specifically references Deutsche Bank’s AML failings relating to mirror trading.

From a professional perspective, the key issue is economic purpose. Genuine trading is usually driven by investment strategy, hedging, liquidity needs, client execution, or market-making. Mirror trading, by contrast, is suspicious where the transactions are economically neutral or near-neutral from a market-risk perspective but effective for moving value between accounts, affiliates, beneficial owners, or jurisdictions. That is why regulators and firms look at whether the apparent trading rationale matches the commercial reality of the activity. FINRA’s red-flag guidance places mirror trades alongside securities-based currency-conversion patterns, which reflects this concern.

Watch on YouTube: Mirror Trading

Mirror trading is particularly important because it can sit at the intersection of AML risk, sanctions-adjacent risk, and market-integrity risk. Even where a mirror-trading pattern does not amount to classic market abuse on its own, ESMA noted in its MAR review that such schemes can still have negative impacts on market integrity because integrity is broader than just preventing formal market abuse. The FCA’s capital-markets AML review likewise treats market-based laundering typologies as a rising threat.

The Deutsche Bank case is the best-known regulatory example. The FCA fined Deutsche Bank in 2017 for serious AML control failings, and the Final Notice describes a suspicious mirror-trading scheme involving customers in Russia and the UK, with large trading volumes inconsistent with customer profiles and concerns that one customer was trading on behalf of “no name” companies. The FCA later referred back to this case in its thematic review on money laundering through markets.

Operationally, mirror trading is challenging because each individual trade may look ordinary when viewed in isolation. The suspicious pattern emerges when firms connect the trades across accounts, desks, affiliates, jurisdictions, currencies, timestamps, beneficial owners, or common control indicators. This means effective detection depends on surveillance and AML controls that can link related activity rather than reviewing transactions one by one. The FCA’s money-laundering-through-markets review emphasizes that capital markets facilitate the movement of vast amounts of capital and that this complexity makes detection difficult.

A mature control response therefore needs several layers: strong customer due diligence and beneficial ownership analysis, monitoring for offsetting or paired trades with little apparent market rationale, review of securities used primarily as conversion tools, scrutiny of unusual cross-border client relationships, and escalation where trading activity appears inconsistent with the customer profile or stated business purpose. FINRA’s AML red flags and the FCA’s thematic work both support this broader, pattern-based approach.

Ultimately, mirror trading is significant in the financial crime environment because it uses the appearance of legitimate securities trading to conceal the movement and transformation of value. It is a reminder that capital markets can be misused not only for market abuse, but also for laundering and covert transfer of funds when firms do not connect the economic reality of trades to the identities, relationships, and purposes behind them.