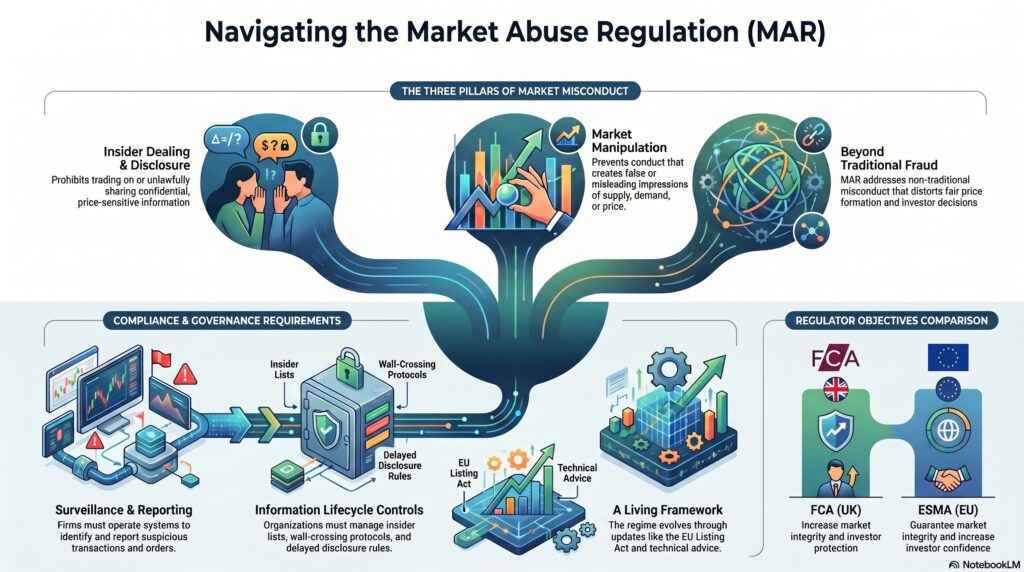

The Market Abuse Regulation (MAR) is the market-integrity regime that governs insider dealing, unlawful disclosure of inside information, market manipulation, and related issuer and market obligations. In the UK, the FCA says the UK Market Abuse Regulation (UK MAR) aims to increase market integrity and investor protection, while ESMA states that the market abuse framework is intended to guarantee the integrity of European financial markets and increase investor confidence.

In the financial crime environment, MAR is significant because it addresses a category of misconduct that can be highly damaging even when it does not look like traditional fraud or money laundering. Market abuse undermines fair price formation, distorts investor decisions, weakens confidence in markets, and can allow insiders or manipulators to profit unfairly from privileged information or deceptive trading behavior. The FCA’s market-abuse pages describe behavior such as insider dealing and market manipulation as market abuse and emphasize the safeguards firms must have in place.

From a professional perspective, MAR is best understood as a market-conduct and market-integrity framework rather than a classic AML regime. Its core function is to reduce misconduct in capital markets by setting prohibitions and disclosure obligations, and by requiring firms and issuers to operate surveillance, information controls, and escalation mechanisms. That said, MAR is directly relevant to the wider financial crime environment because market abuse often overlaps with insider misuse of information, front running, communications misconduct, conflicts of interest, weak governance, and failures in market surveillance. This is an inference supported by the FCA and ESMA descriptions of MAR’s purpose and scope.

A central feature of MAR is that it covers three core forms of abuse: insider dealing, unlawful disclosure of inside information, and market manipulation. ESMA’s market integrity page describes the framework in exactly those terms. In practical terms, this means MAR is concerned both with misuse of confidential, price-sensitive information and with conduct that creates false or misleading impressions about supply, demand, or price.

Watch on YouTube: Market Abuse Regulation

MAR is also important because it does more than prohibit bad behavior after the event. It creates a wider operating framework around inside information, issuer disclosure, delayed disclosure, insider lists, suspicious transaction and order reporting, and market-sounding or related information-handling controls. The FCA’s overview says UK MAR covers the regulation’s application and structure, offences, and exemptions, while ESMA continues to publish Q&As and review work on how the regime should operate in practice.

This matters in the financial crime environment because many market-abuse risks arise from weak control over information rather than from a single obvious trade. A firm may fail to identify inside information properly, allow it to move too freely across desks, apply weak wall-crossing controls, or fail to restrict trading when sensitive information is held. In such cases, the problem is not merely individual misconduct; it is a control failure in the market-integrity framework. FCA best-practice material notes that MAR is the UK’s civil market abuse regime and emphasizes identifying, controlling, and disclosing inside information properly.

MAR is particularly relevant to surveillance and governance. Firms operating in markets covered by MAR need systems and controls capable of identifying suspicious orders and transactions, managing access to inside information, and escalating potential abuse. The FCA continues to stress the importance of safeguards and has recently signaled a strategic focus on combating market abuse, while its Market Conduct sourcebook remains a key reference point for how firms should approach insider dealing, unlawful disclosure, and manipulation risks.

There is also a current-evolution point worth noting. MAR is not static. ESMA’s 2025 technical advice and 2026 simplification consultation reflect continuing refinement of the regime, including changes linked to the EU Listing Act. For example, ESMA noted in February 2026 that one prior delayed-disclosure condition about “not misleading the public” had been removed by the Listing Act and replaced with a different requirement. That shows MAR remains a live and developing framework rather than a fixed historical rule set.

In the UK, MAR also sits within a broader legal architecture. Regulation (EU) No 596/2014 remains the core legislative source, and UK implementation and related enforcement provisions are supported by domestic instruments and FCA rules. The FCA’s pages and the legislation sources show that MAR is part of the operative UK market-abuse regime, alongside related rules and criminal frameworks.

Ultimately, the Market Abuse Regulation matters in the financial crime environment because it protects the integrity of financial markets against misuse of inside information, manipulative conduct, and related failures of disclosure and control. It is a core framework for ensuring that markets remain fair, orderly, and trustworthy, and for requiring firms and issuers to build the surveillance, governance, and information-control arrangements needed to support that outcome.