Machine learning is a branch of artificial intelligence in which systems learn patterns from data and use those patterns to classify, score, predict, or detect outcomes without relying solely on fixed, manually coded rules. In the financial crime environment, machine learning is important because firms and authorities are trying to detect increasingly complex fraud, money laundering, market abuse, and identity-related risks across large volumes of data and fast-moving channels. FATF’s guidance on new technologies for AML/CFT states that machine learning can support customer identification and verification, behavioural and transactional analysis, and ongoing monitoring.

From a professional perspective, machine learning is not a single tool or a complete control framework. It is a set of analytical techniques that can support financial crime functions such as fraud detection, transaction monitoring, screening, alert prioritization, digital identity proofing, communications surveillance, and investigative triage. The FCA’s current financial crime materials note active work on AI and machine learning in market abuse surveillance and broader financial crime contexts, while FATF’s digital-transformation work highlights the use of machine learning to process large volumes of structured and unstructured data more effectively.

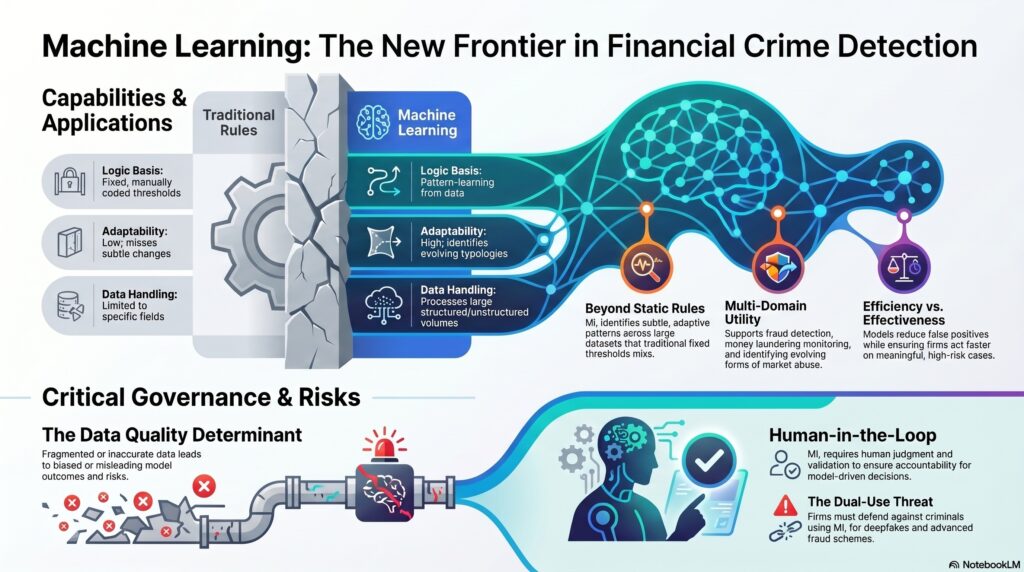

In practical terms, machine learning is most valuable where traditional rules struggle. Static thresholds and scenario rules remain important, but they can miss patterns that are subtle, adaptive, or spread across many signals. Machine learning can help identify anomalies, group similar behaviour, detect unusual account activity, prioritize higher-risk alerts, and surface patterns that do not fit known typologies neatly. FATF specifically notes that machine learning can be used for behavioural and transactional analysis by placing customers with similar behaviour into groups and then identifying deviations from those norms.

This makes machine learning relevant across multiple financial crime domains. In fraud, it can support account takeover detection, payment-risk scoring, scam intervention, and synthetic-identity assessment. In AML, it can help identify suspicious flows, unusual customer behaviour, and network patterns that may not be visible through simple rules. In market-conduct settings, the FCA’s Market Abuse Surveillance TechSprint explored how AI and machine learning could help detect evolving forms of market abuse.

Watch on YouTube: Machine Learning

Machine learning is also important because the threat environment itself is becoming more ML-enabled. FinCEN issued an alert in November 2024 on fraud schemes involving deepfake media created with generative AI and machine learning, showing that firms are not only using these technologies defensively but are also facing criminal misuse of them. In other words, machine learning is both part of the control toolkit and part of the threat landscape.

A key professional point is that machine learning does not remove the need for judgment, governance, or accountability. FATF’s technology guidance emphasizes the conditions, policies, and practices needed for technology to improve AML/CFT outcomes, and its collaborative analytics work notes that validation is particularly difficult in AML/CFT because confirming whether a pattern really indicated criminal conduct can take years. This is why machine learning must be treated as a controlled component of the financial crime framework, not as an autonomous decision-maker.

Data quality is one of the biggest determinants of success. Machine learning models depend on reliable customer, transaction, device, communications, and case data. If those inputs are fragmented, inaccurate, biased, or weakly labeled, the model may produce poor or misleading outcomes. FATF’s guidance repeatedly links successful use of new technologies to the quality of implementation, data, and supporting governance.

There is also an important distinction between efficiency gains and effectiveness gains. Machine learning may reduce false positives, improve alert triage, or speed up review processes, but those benefits only matter if the firm is also identifying more real risk or acting faster on meaningful cases. FATF’s guidance highlights opportunities to improve both efficiency and effectiveness, and FinCEN’s innovation work has noted the challenge of obtaining suitable training data for AI and machine learning solutions in AML/CFT.

Governance is therefore central. Firms need clear ownership for model design, training data, validation, calibration, monitoring, explainability, and remediation when outputs drift or perform poorly. The FCA’s broader AI approach is principles-based and outcomes-focused, and its financial crime materials continue to focus on system effectiveness rather than novelty. In practice, that means firms remain responsible for the consequences of models they deploy, even where those models are technically complex.

Ultimately, machine learning is significant in the financial crime environment because it can help firms and authorities detect patterns that are difficult to identify through manual review or simple rule sets alone. It can strengthen fraud prevention, AML monitoring, market abuse surveillance, and identity-risk management. But its value depends on something more than advanced mathematics: good data, strong validation, clear governance, and informed human oversight. Without those, machine learning can create the appearance of sophistication without delivering a genuinely stronger financial crime control outcome.