A Limited Liability Company (LLC) is a business structure created under state law that combines elements of corporate limited liability with flexible ownership and tax treatment. The IRS states that an LLC is a business structure allowed by state statute, and the SBA explains that it combines features of corporation and partnership structures while generally protecting owners’ personal assets from business liabilities.

In the financial crime environment, an LLC is important because it is a common and legitimate legal vehicle that can also be misused to obscure ownership, control, and the true purpose of a business relationship. An LLC may be entirely ordinary and low risk, but it can also be used as a shell, front, nominee-held entity, or transactional conduit if due diligence is weak. FATF’s beneficial ownership guidance warns that legal persons can be used to obscure the identity of criminals, the true purpose of accounts or property, and the source or use of funds, particularly where ownership and control structures are layered or opaque.

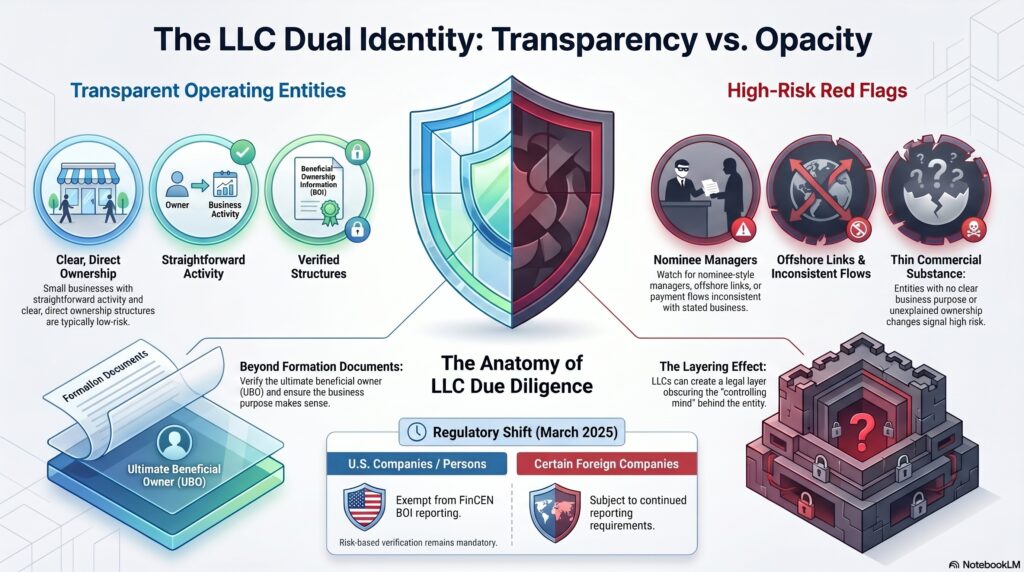

From a professional perspective, the significance of an LLC lies less in the legal form itself and more in the flexibility the form allows. The IRS notes that most states do not restrict ownership and that members may include individuals, corporations, other LLCs, and foreign entities, and many states permit single-member LLCs. That flexibility is commercially useful, but it also means that the legal owner on paper may not immediately reveal the ultimate beneficial owner or the real controlling mind behind the entity.

Watch on YouTube: Limited Liability Company (LLC)

This is why LLCs are particularly relevant to customer due diligence, beneficial ownership review, source-of-funds assessment, and sanctions screening. A firm onboarding an LLC cannot usually rely on the entity’s name, registration, or formation documents alone. It needs to understand who the members are, who controls the company, whether that control is direct or indirect, and whether the stated business purpose makes commercial sense. FATF’s beneficial ownership guidance and best-practices materials specifically highlight the misuse of anonymous shell companies and layered ownership structures to hide illicit activity.

An LLC can therefore be both ordinary and high-risk, depending on context. A small operating business with transparent ownership, straightforward activity, and normal transactional behavior may present limited financial crime concern. By contrast, an LLC with nominee-style managers, offshore links, unexplained changes in ownership, thin commercial substance, or payment flows inconsistent with its stated business can present significantly higher risk. This is an inference from the legal flexibility described by the IRS and the opacity risks described by FATF.

The U.S. regulatory picture around LLC transparency has also changed recently. FinCEN states that, as of March 2025, U.S. companies and U.S. persons are exempt from the requirement to report beneficial ownership information to FinCEN under the revised BOI rule, while certain foreign companies remain subject to reporting requirements. That change affects the BOI reporting regime, but it does not remove the need for firms to understand LLC ownership and control for AML, sanctions, fraud, and wider risk-management purposes.

For financial institutions, the practical issue is that an LLC may create a layer between the customer relationship and the real person behind it. That layer can be perfectly legitimate, but it can also reduce transparency if the firm does not collect and verify the right information. A mature control framework therefore looks beyond formation documents and asks who ultimately owns or controls the LLC, what the entity actually does, why it needs the product or service, and whether its activity remains consistent with that explanation over time. This is an inference supported by FATF’s focus on beneficial ownership and legal-person transparency.

Ultimately, an LLC is a standard business structure, not a financial crime indicator by itself. Its relevance in the financial crime environment comes from the fact that it can offer both legitimate business flexibility and opportunities for opacity. For that reason, LLCs should be treated as legal entities that require proportionate but often careful scrutiny around ownership, control, purpose, and ongoing activity.