The General Data Protection Regulation (GDPR) is the core EU legal framework governing how personal data is processed, protected, and transferred. The European Commission describes GDPR as part of the EU data protection legal framework, and the Council of the EU states that it governs how the personal data of individuals in the EU may be processed and transferred.

In the financial crime environment, GDPR is significant because financial crime controls depend heavily on personal data. Customer due diligence, sanctions screening, fraud monitoring, transaction monitoring, communications surveillance, suspicious activity investigations, employee screening, and case management all involve processing personal information. GDPR does not remove the need for those controls, but it requires firms to carry them out lawfully, proportionately, securely, and transparently. That makes GDPR a governance framework for how financial crime controls use data, not a barrier to financial crime prevention itself. This is an inference supported by the GDPR’s broad application to processing personal data and the ICO’s guidance on lawful basis and the UK GDPR principles.

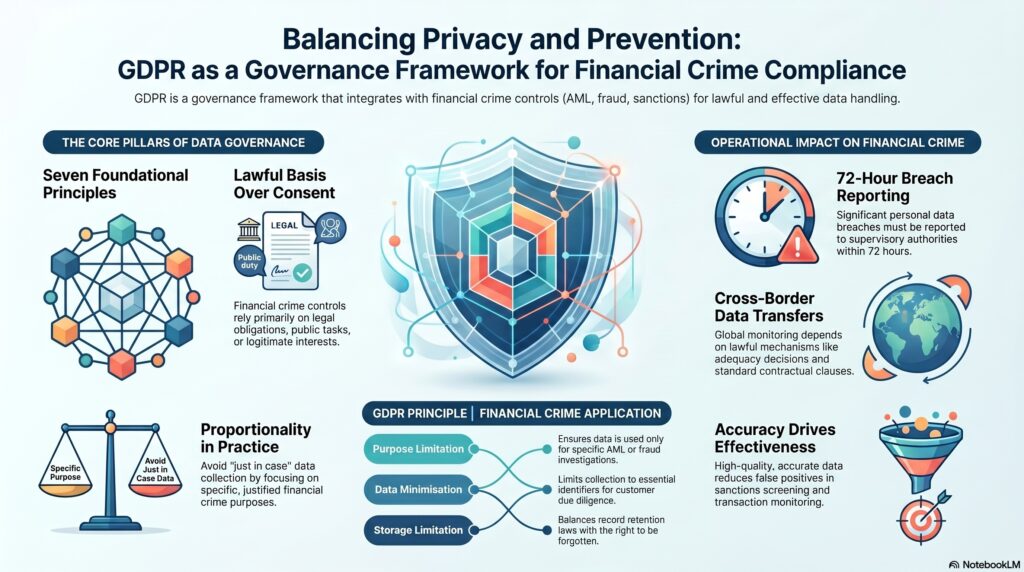

From a professional compliance perspective, GDPR is most relevant where firms are tempted to treat financial crime prevention as justification for unlimited data collection or unrestricted data reuse. The regulation does not work that way. The ICO states that the UK GDPR is built around seven principles: lawfulness, fairness and transparency; purpose limitation; data minimisation; accuracy; storage limitation; integrity and confidentiality; and accountability. Those principles are highly relevant to financial crime operations because AML, fraud, and sanctions teams often process large, sensitive, and long-retained datasets.

A key concept is lawful basis. Financial crime controls usually rely less on consent and more on legal obligation, public task, or legitimate interests, depending on the context and jurisdiction. The ICO’s lawful basis guidance makes clear that organizations must identify the correct legal basis for processing rather than treating all processing as automatically permitted. In the financial crime environment, this matters because a firm needs to know why it is screening customers, monitoring transactions, retaining records, or using data in fraud analytics, and it must be able to justify that reasoning if challenged.

Watch on YouTube: General Data Protection Regulation (GDPR)

GDPR is also important because it affects data quality and proportionality in financial crime systems. If a firm holds inaccurate customer data, fragmented records, or outdated identifiers, both privacy compliance and financial crime effectiveness suffer. Poor data can increase false positives in sanctions screening, weaken transaction monitoring, and create poor outcomes for customers. At the same time, collecting excessive data “just in case” can breach minimisation and purpose-limitation principles. In practical terms, GDPR pushes firms toward more disciplined data governance, which can strengthen as well as constrain financial crime controls. This is an inference supported by the GDPR principles framework.

Another major area of relevance is international data transfer. Financial crime investigations and controls often require cross-border sharing of personal data, whether within a financial group, with vendors, or across jurisdictions. The European Commission notes that the GDPR provides specific mechanisms for transfers outside the EU, including adequacy decisions, standard contractual clauses, and binding corporate rules. In the financial crime environment, this matters because global monitoring, correspondent banking oversight, multinational fraud investigations, and centralized sanctions screening frequently depend on lawful transfer arrangements.

There is also a strong relationship between GDPR and record retention, customer rights, and exemptions. Financial crime teams often retain information for long periods because of AML, audit, or litigation requirements. They may also need to respond to subject access requests while protecting sensitive investigative material or complying with statutory restrictions. The ICO’s guidance on subject access, exemptions, and documentation shows that these issues are operationally significant rather than theoretical. In practice, firms need clear governance to reconcile privacy rights with legal duties to retain records, report suspicious activity, and avoid prejudicing investigations.

Security is another obvious intersection. The ICO’s breach guidance states that certain personal data breaches must be reported to the supervisory authority within 72 hours where feasible, and that affected individuals must also be informed when the risk is high. In the financial crime environment, data breaches can directly expose firms to fraud, identity theft, account takeover, and sanctions-screening disruption, so GDPR’s integrity and confidentiality principle is closely aligned with financial crime resilience.

A professionally mature view therefore treats GDPR as a coexisting framework, not a competing one. Financial crime obligations and data protection obligations usually operate side by side. A firm should be able to explain what personal data it uses for AML, fraud, sanctions, and surveillance purposes; why that use is lawful; how long the data is retained; how it is protected; when it is shared; and how customer rights are handled without undermining legal reporting or investigative duties. That balance is central to credible governance in modern financial services. This is an inference supported by the Commission’s description of GDPR as the core EU data framework and the ICO’s operational guidance.

Ultimately, GDPR matters in the financial crime environment because nearly every serious financial crime control depends on personal data. The regulation does not prevent firms from managing financial crime risk, but it requires them to do so in a way that is lawful, proportionate, secure, and accountable. For that reason, GDPR should be understood as a foundational governance framework for the use of data within AML, fraud, sanctions, and wider financial crime operations.