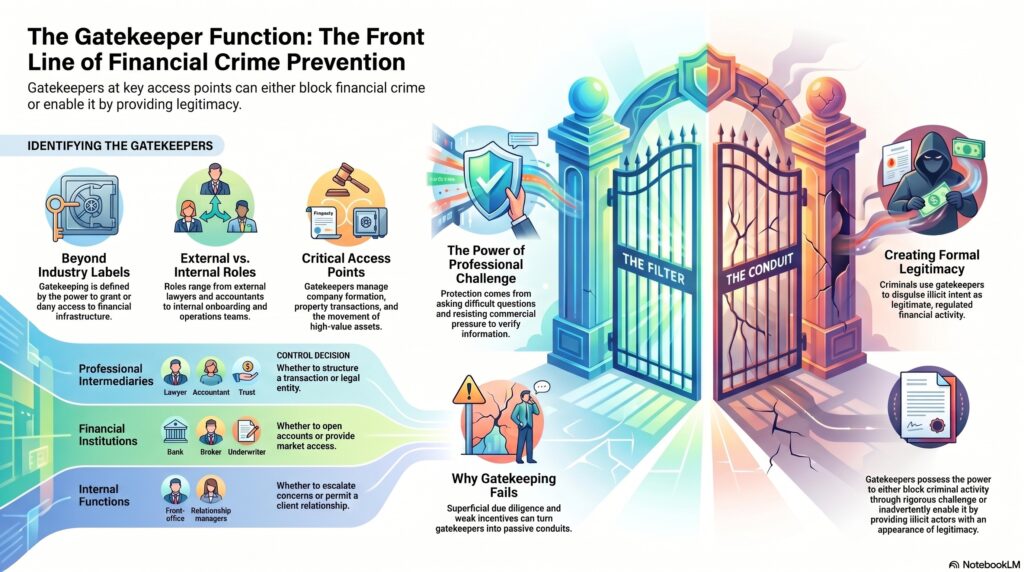

In the financial crime environment, gatekeepers are the individuals, firms, and control functions that stand at key access points to the financial system and can either prevent or enable illicit activity. The term is commonly used for professionals and institutions whose services can help establish companies, move funds, structure transactions, verify customers, provide market access, or otherwise create legitimacy. FATF has repeatedly highlighted the role of professional intermediaries and other non-financial businesses and professions in preventing misuse of legal persons, assets, and financial channels, while the UK National Risk Assessment describes certain professional services as gatekeepers to the financial and corporate system.

From a professional perspective, the importance of gatekeepers lies in their position, not merely their industry label. A gatekeeper is important because they can decide whether access is granted, whether information is challenged, whether suspicious activity is escalated, and whether a structure or transaction is allowed to proceed. That role may be performed by banks, lawyers, accountants, company formation agents, trust and corporate service providers, estate agents, dealers in high-value goods, brokers, introducers, or internal control functions inside a firm. FATF’s standards and guidance on DNFBPs and beneficial ownership are built around exactly this concern: that intermediaries who create, manage, or validate access to financial and corporate structures can either reduce or amplify financial crime risk.

In the financial crime environment, gatekeepers matter because criminals rarely rely only on direct confrontation with the regulated financial system. More often, they seek legitimacy through intermediated access. A company may be incorporated through a service provider, a trust may be arranged through professional advisers, an account may be opened with the support of an introducer, a property transaction may be facilitated through professionals, or a market transaction may be routed through a regulated firm. If the gatekeeper asks the right questions, verifies ownership properly, and escalates concerns, the scheme may be stopped early. If the gatekeeper is careless, conflicted, complicit, or too commercially driven to challenge the customer, the criminal gains entry with an appearance of legitimacy. This is an inference supported by FATF’s repeated focus on gatekeeper professions and the misuse of legal persons and arrangements.

Watch on YouTube: Gatekeepers

A key distinction is that gatekeepers are not always external professional advisers. Internal teams can also play gatekeeper roles. Front-office staff, onboarding teams, relationship managers, payment approvers, control-room functions, compliance reviewers, and operations teams may all sit at points where they can permit or block risky activity. In that sense, gatekeeping is a function as much as a profession. The question is whether the person or team controls access to something the criminal wants: a customer relationship, a transaction, a legal structure, a regulated service, or confidential information. This is consistent with the FCA’s broad framing that firms themselves are a vital line of defence against financial crime and must maintain effective systems and controls.

Gatekeepers are especially relevant in areas such as beneficial ownership, customer due diligence, company formation, trust structures, property transactions, correspondent relationships, and market access. These are all areas where formal legitimacy can be created even when the underlying purpose is illicit. FATF’s beneficial ownership guidance is particularly clear that opaque legal persons and arrangements can be exploited by money launderers, tax evaders, corrupt actors, and sanctions evaders, and that gatekeeper professions and institutions have an important role in preventing that opacity from succeeding.

This is why gatekeeper risk is closely linked to professional judgment and challenge. A gatekeeper does not protect the system simply by being present. The protective value comes from the willingness and ability to ask difficult questions, verify explanations, identify red flags, resist commercial pressure, and escalate concerns. Where incentives are weak, due diligence is superficial, or accountability is unclear, gatekeepers can become passive conduits rather than effective filters. In more serious cases, they may become active facilitators. FATF and national risk assessments both highlight that professional enablers and service providers can be misused, whether knowingly or unknowingly, when their controls are weak.

A mature financial crime framework therefore treats gatekeepers as a control concept that requires clear standards, training, escalation routes, and oversight. Firms need to know which roles act as gatekeepers, what decisions they control, what information they must verify, and when they must refuse or escalate business. They also need to manage conflicts of interest, commercial pressure, and weak challenge culture, because these are often the conditions under which gatekeeping fails. This is an inference from the cited regulatory focus on systems, controls, and the gatekeeper role of intermediaries.

Ultimately, gatekeepers matter in the financial crime environment because they are the people and institutions that stand between criminal intent and financial-system access. They can prevent misuse of companies, accounts, markets, property, and payment channels, or they can allow it to enter the system with the appearance of legitimacy. For that reason, gatekeepers should be understood not as a vague ethical category, but as a core control layer in AML, sanctions, fraud, and wider financial crime prevention.