Financial statement fraud is the deliberate misrepresentation of an organization’s financial condition through intentional misstatement or omission in its financial statements or related disclosures. The Association of Certified Fraud Examiners defines it as the deliberate misrepresentation of the financial condition of an enterprise through intentional misstatement or omission of amounts or disclosures in the financial statements to deceive users.

In the financial crime environment, financial statement fraud is significant because it is not simply an accounting failure. It is a form of deception that can distort investor decisions, mislead creditors and counterparties, conceal liquidity or solvency problems, support unlawful fundraising, mask operational losses, and in some cases enable broader fraud, corruption, or market misconduct. The SEC maintains a dedicated set of Accounting and Auditing Enforcement Releases for financial-reporting-related enforcement actions, which reflects how seriously U.S. regulators treat this type of misconduct.

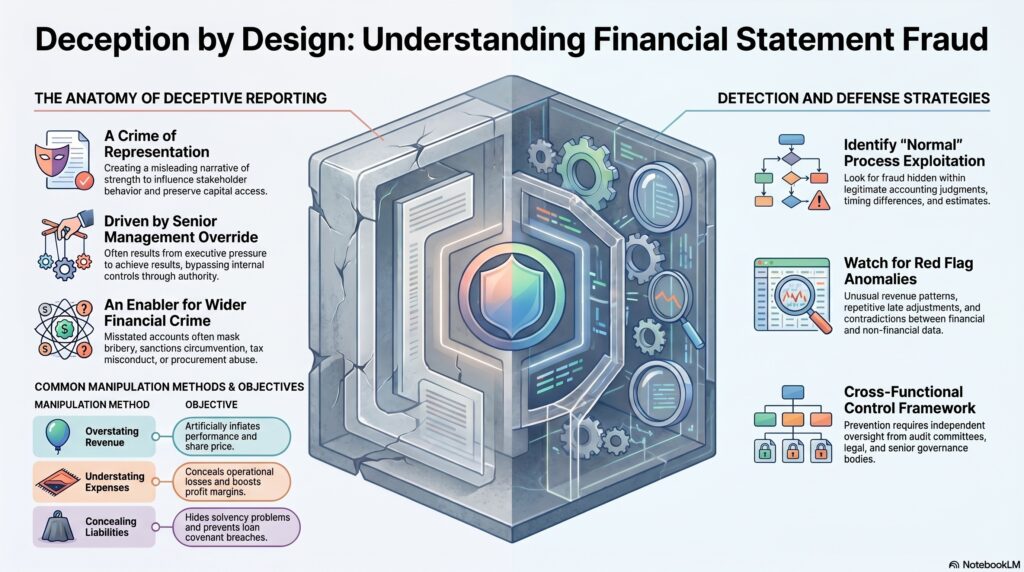

From a professional perspective, financial statement fraud is best understood as a crime of representation. The organization is presenting a false picture of performance, position, cash generation, liabilities, or prospects in order to influence how investors, lenders, auditors, regulators, boards, or other stakeholders behave. Unlike asset misappropriation, which often involves direct theft, financial statement fraud is usually about creating a misleading narrative of legitimacy, strength, or control. That narrative can preserve access to capital, support executive remuneration, avoid covenant breaches, maintain share price, delay regulatory scrutiny, or hide the economic effects of other misconduct. This is an inference supported by the ACFE definition and the SEC’s focus on financial reporting and accounting fraud enforcement.

Watch on YouTube: Financial Statement Fraud

In practical terms, financial statement fraud can take several forms. Revenue may be overstated, expenses understated, liabilities concealed, reserves manipulated, asset values inflated, impairments delayed, disclosures omitted, or transactions structured to create a misleading accounting result. It can also involve fraudulent presentation rather than pure number manipulation, for example by concealing related-party arrangements, misrepresenting segment performance, or omitting facts necessary to make the overall picture fair and not misleading. AICPA training materials on financial statement fraud point to internal-control weaknesses, management override, and pressure to achieve particular financial results as recurring enabling factors.

That last point is especially important in the financial crime environment: financial statement fraud is often driven by pressure, opportunity, and rationalization at senior levels of an organization. Because the reporting process sits close to management, this form of fraud frequently depends on override of internal controls, suppression of challenge, manipulation of judgments, or intimidation of finance staff. It is therefore as much a governance failure as an accounting one. When financial statement fraud occurs, it often indicates deeper weaknesses in tone from the top, audit committee effectiveness, internal challenge culture, and control independence. This is an inference supported by the AICPA’s focus on internal-control weaknesses and management override, and by the SEC’s continuing accounting-fraud enforcement activity.

Financial statement fraud also has a strong connection to the wider financial crime ecosystem. False financial reporting can support securities fraud, market manipulation, bribery concealment, procurement abuse, sanctions circumvention, tax misconduct, and the masking of losses tied to other criminal activity. If a firm misstates revenue, cash, or liabilities, the distorted accounts may be used to raise funds, sell securities, secure loans, justify bonuses, or reassure counterparties under false pretences. In this sense, financial statement fraud is not only a reporting problem; it can be an enabling mechanism for wider deception and illicit financial gain. This is an inference based on the SEC’s treatment of accounting and disclosure fraud as an enforcement priority and the nature of fraudulent financial representations.

For compliance, audit, and anti-fraud professionals, the challenge is that financial statement fraud may be concealed within apparently normal reporting processes. It often exploits legitimate accounting judgments, timing differences, estimates, reserves, and disclosure practices rather than obviously fabricated ledgers. That means detection depends heavily on skepticism, challenge, control testing, trend analysis, and attention to inconsistencies between reported results and underlying business reality. Unusual revenue recognition patterns, unexplained margin changes, repetitive late adjustments, aggressive assumptions, contradictory non-financial data, or pressure around reporting deadlines may all be relevant indicators. AICPA materials on auditing fraud risk and financial statement fraud specifically highlight revenue, liabilities, expenses, and disclosures as areas where fraud is commonly identified.

A mature control framework therefore treats financial statement fraud as a cross-functional risk involving finance, compliance, internal audit, external audit, legal, and senior governance bodies. Prevention depends on strong internal controls over financial reporting, segregation of duties, challenge over significant judgments, whistleblowing arrangements, audit committee oversight, and a culture that does not reward distorted reporting. Detection depends on anomaly review, journal-entry testing, disclosure challenge, forensic analysis where needed, and escalation routes that are independent of management influence. The SEC’s continued publication of accounting and disclosure enforcement actions and the ACFE’s professional training emphasis both support the need for strong fraud-detection capability in this area.

Ultimately, financial statement fraud is a serious financial crime because it corrupts one of the most important trust mechanisms in the financial system: reliable reporting. Investors, lenders, employees, regulators, and counterparties all depend on financial statements to make decisions. When those statements are manipulated deliberately, the harm extends beyond accounting accuracy to market confidence, capital allocation, customer and investor protection, and the integrity of corporate governance itself. For that reason, financial statement fraud should be treated not as a narrow technical accounting issue, but as a major form of financial deception with direct relevance to the wider financial crime framework.