A Financial Intelligence Unit (FIU) is the national center responsible for receiving, analyzing, and disseminating financial intelligence related to money laundering, associated predicate offenses, and terrorist financing. FATF Recommendation 29 requires countries to establish an FIU with exactly that role, and the Egmont Group uses the same FATF-based definition in its charter and public materials.

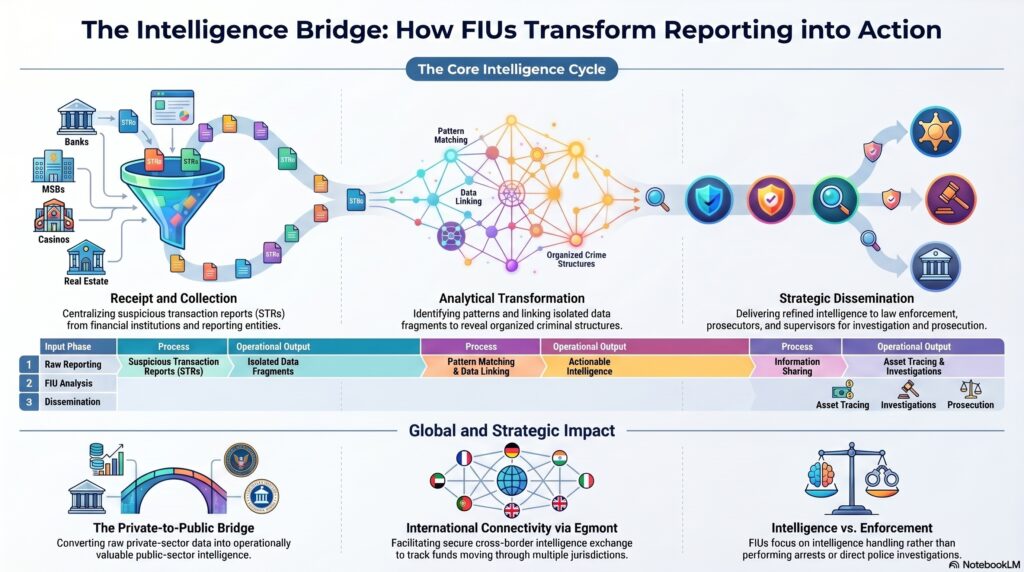

In the financial crime environment, the FIU is significant because it sits at the point where private-sector reporting becomes public-sector intelligence. Financial institutions, money services businesses, and other reporting entities generate suspicious transaction reports and other information, but those reports only become operationally valuable when they are received, assessed, connected to other data, and turned into intelligence that can support investigations, asset tracing, disruption, and strategic risk understanding. Egmont states that FIUs serve as national centres for receipt and analysis and are responsible for disseminating analysis results, while FinCEN describes its own mission in terms of collecting, analyzing, and disseminating financial intelligence.

From a professional perspective, an FIU is not merely a filing repository. Its role is analytical and intelligence-led. A high-quality FIU does more than store suspicious transaction reports. It examines patterns, identifies links between entities and transactions, combines reporting with other relevant information, and produces outputs that help law enforcement, prosecutors, supervisors, and other competent authorities understand financial crime activity. FATF’s standards treat the FIU as a core institutional component of an effective AML/CFT framework precisely because reporting alone is not enough; intelligence must be processed and used.

A central reason FIUs matter is that they improve the state’s ability to understand financial crime as a system, not just as isolated incidents. An individual suspicious transaction report may reveal only a fragment of risk. Once combined with other STRs, account data, predicate crime information, cross-border intelligence, and open-source or law-enforcement information, it may reveal organized laundering structures, terrorist-financing activity, corruption proceeds, sanctions-adjacent evasion patterns, fraud networks, or mule-account ecosystems. This is an inference supported by the FIU’s mandated role in receipt, analysis, and dissemination of relevant information.

Watch on YouTube: Financial Intelligence Unit (FIU)

FIUs are also important because they help connect the domestic AML framework with the international intelligence-sharing environment. The Egmont Group describes itself as a united body of FIUs and says it provides a platform for the secure exchange of expertise and financial intelligence to combat money laundering, terrorist financing, and associated predicate crimes. FinCEN likewise describes the Egmont Group as an international network designed to improve communication, information sharing, and training coordination among FIUs. In practice, this means FIUs are often the main institutional channel through which one jurisdiction can request or share financial intelligence with another.

That international role matters because financial crime is frequently cross-border. Funds move through multiple institutions and jurisdictions, legal entities may be incorporated in one place and bank elsewhere, and predicate crimes such as fraud, corruption, trafficking, and sanctions evasion often generate payment trails that do not stay within a single country. A strong FIU helps reduce the fragmentation that would otherwise occur between domestic reporting systems and international cooperation channels. This is an inference from the Egmont Group’s role as a secure exchange platform for FIUs and FATF’s treatment of FIUs as a central national function.

A professionally mature understanding of FIUs also distinguishes them from law enforcement. The Egmont Group states that it does not conduct financial investigations itself and that domestic investigative authorities manage those inquiries. That distinction is important: an FIU is usually an intelligence function, not a police force or prosecutor. Its job is to receive, analyze, and disseminate financial intelligence, not necessarily to carry out arrests or prosecutions. Depending on the jurisdiction, the FIU may sit within a finance ministry, central authority, or other government structure, but its role remains focused on intelligence handling and dissemination.

In practical compliance terms, the FIU is one of the main reasons suspicious transaction and suspicious activity reporting matters. Reporting entities file because the FIU is the designated national body capable of turning those reports into intelligence. If the FIU is weak, under-resourced, or poorly connected to competent authorities, the value of the reporting regime is diminished. If the FIU is strong, reporting can support not only individual case development but also strategic analysis of typologies, sectors, geographies, and emerging risks. Egmont’s recent publication on the role of FIUs in national risk assessment processes underscores that FIUs also contribute to strategic understanding of country-level financial crime threats.

The U.S. example illustrates this clearly. FinCEN functions as the U.S. FIU and states that its mission is to safeguard the financial system from illicit activity and promote national security through the collection, analysis, and dissemination of financial intelligence. It also says that it carries out that mission by receiving and maintaining financial transactions data, analyzing and disseminating it for law enforcement purposes, and building global cooperation with counterpart organizations.

Ultimately, the FIU is a core institution in the financial crime environment because it is the national mechanism that converts financial reporting into actionable intelligence. It links private-sector reporting with public-sector analysis, supports domestic and international cooperation, and helps authorities understand not just single suspicious transactions but broader criminal networks and risk patterns. Without an effective FIU, AML/CFT systems lose much of their operational value.