The Financial Conduct Authority (FCA) is the UK regulator responsible for conduct supervision across financial services and for promoting market integrity, effective competition, and appropriate consumer protection. In the financial crime environment, the FCA is especially important because it sits at the point where consumer harm, market abuse, firm governance, and financial crime controls intersect. The FCA’s current financial crime page states that it is working to disrupt criminals and support firms to be an effective line of defence against financial crime, and its 2026/27 Annual Work Programme confirms that protecting market integrity and tackling market abuse remain active priorities.

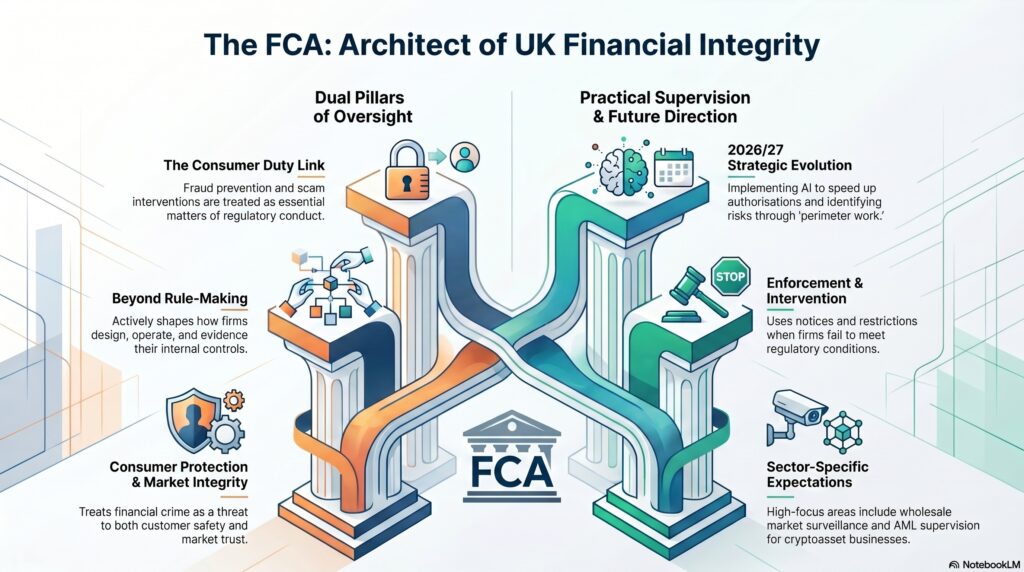

From a professional financial crime perspective, the FCA is not simply a rule-making body. It is a supervisory and enforcement authority that shapes how firms design, operate, and evidence their controls. Its expectations influence how firms approach money laundering, terrorist financing, fraud, bribery and corruption, sanctions, market abuse, and wider conduct risk. The FCA’s own published materials frame financial crime as damaging to both consumers and markets, and its sector-specific Regulatory Priorities reports continue to emphasise robust governance, surveillance, and controls as essential to preventing financial crime and market abuse.

A defining feature of the FCA’s role is that it treats financial crime as both a consumer protection issue and a market integrity issue. Fraud, weak AML controls, poor sanctions governance, and ineffective surveillance can cause direct customer harm, but they can also erode trust in UK markets and regulated firms. The FCA’s own outcomes and metrics framework links consumer confidence to minimised financial crime and cleaner markets with low levels of market abuse and misconduct. That dual focus is one reason the FCA is so central to the UK financial crime environment: it is concerned not only with whether firms comply, but with whether their controls support trustworthy markets and fair outcomes.

Watch on YouTube: Financial Conduct Authority

The FCA’s role is also highly practical. It publishes detailed guidance, thematic findings, sector priorities, and supervisory expectations that firms are expected to translate into operating controls. The Financial Crime Guide remains one of the FCA’s most important reference points for firms building AML, fraud, sanctions, and wider financial crime frameworks, and the FCA has continued updating that guide to reflect current risks and expectations. In parallel, its Regulatory Priorities reports now give firms clearer, sector-specific direction on where the FCA expects attention and remediation.

In wholesale and capital markets, the FCA is especially significant because of its focus on market abuse, surveillance, conduct oversight, and transaction reporting. Its current Wholesale Markets priorities say that combating financial crime and market abuse is a core FCA priority and expect firms to strengthen surveillance, governance, and controls, while recent FCA work has also focused on improving transaction and post-trade reporting. In the financial crime environment, this means the FCA is a major actor wherever misconduct takes the form of insider dealing, manipulation, poor information control, inaccurate reporting, or weak market surveillance.

The FCA is also important in payments and retail financial services because it increasingly links financial crime control with customer outcomes. Its Consumer Duty framework requires firms to put customers’ needs first and deliver good outcomes, and its priorities for payments firms explicitly tie financial crime controls, governance, and skills to protecting the integrity of the financial system. In practical terms, that means fraud prevention, scam interventions, safeguarding, and customer support are no longer treated only as operational issues; they are also matters of regulatory conduct and customer protection.

Another important aspect of the FCA’s role is its willingness to intervene directly where firms’ controls are weak. Its notices and restrictions activity, including recent action against a money transfer firm, show that the FCA is prepared to impose restrictions where firms no longer meet regulatory conditions or where consumer protection and financial crime concerns arise. The FCA also acts as the AML and counter-terrorist financing supervisor for UK cryptoasset businesses under the Money Laundering Regulations, which extends its financial crime relevance into newer parts of the market perimeter.

The FCA’s current direction also shows that its supervisory approach is evolving rather than static. In March 2026, it announced plans for using AI to speed authorisations and identify key risks earlier, while still keeping people at the heart of decision-making. Around the same time, it published perimeter work stressing that gaps in the perimeter can be exploited by fraudsters and bad actors, and that strengthening the perimeter would support efforts to tackle fraud and protect market integrity. These developments matter because they show the FCA is thinking not only about firm-by-firm compliance, but about how technology, market structure, and regulatory boundaries affect financial crime risk systemically.

Ultimately, the Financial Conduct Authority is central to the UK financial crime environment because it shapes the standards by which firms are expected to manage fraud, money laundering, sanctions, market abuse, and wider conduct risks. It combines rule-setting, supervision, thematic work, intervention, and enforcement in a way that influences both day-to-day control design and broader market behaviour. For firms operating in the UK, the FCA is not just a conduct regulator in the narrow sense; it is one of the principal authorities defining what a credible, proportionate, and effective financial crime control framework should look like.