An Electronic Funds Transfer (EFT) is, in U.S. consumer-finance law, a transfer of funds initiated through an electronic terminal, telephone, computer, or magnetic tape for the purpose of instructing a financial institution to debit or credit a consumer’s account. Regulation E, which implements the Electronic Fund Transfer Act, uses that definition and covers common consumer payment activities such as ATM transactions, direct deposits, point-of-sale transfers, telephone transfers, and certain ACH-based payments.

In the financial crime environment, EFT is important because it describes a broad category of electronic payment movement that sits at the center of modern retail and commercial financial activity. EFTs are convenient, scalable, and operationally efficient, but those same characteristics also make them attractive for fraud, account abuse, mule activity, and suspicious movement of funds. The Federal Reserve notes that electronic payment systems support ordinary transactions across consumers, businesses, and institutions, which means financial crime controls must work within a high-volume payment environment rather than around occasional exceptional events.

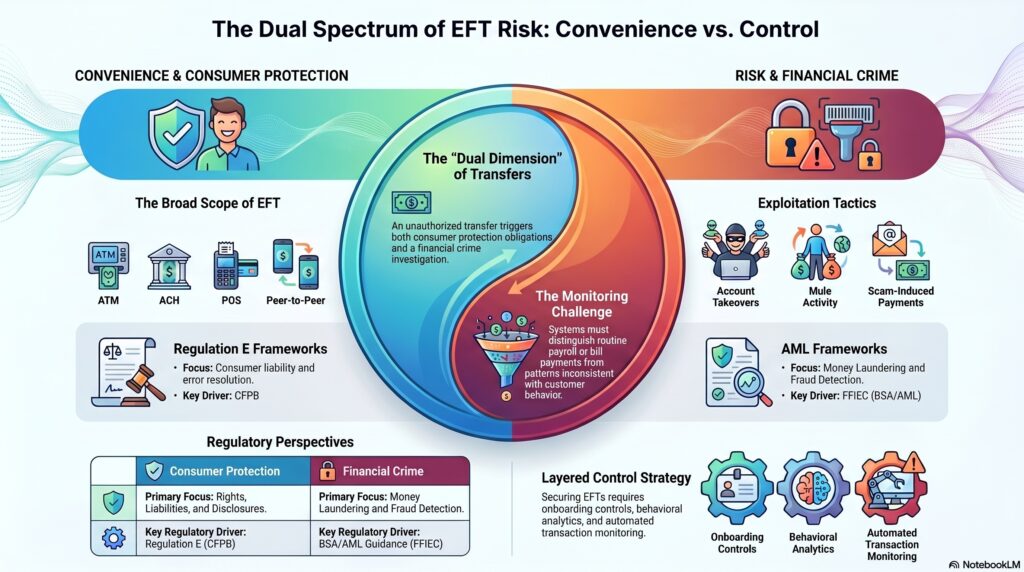

From a professional perspective, EFT should not be understood as a single payment rail. It is a broad category that can include different mechanisms and use cases, depending on the legal and operational context. Regulation E focuses on consumer EFTs, while AML and payment-operations frameworks often look more broadly at funds transfers, ACH activity, card-based activity, and related electronic payment flows. The FFIEC distinguishes “funds transfers” as a separate BSA/AML concept tied to payment orders and interbank movement, while CFPB and Federal Reserve materials frame EFT more specifically around consumer protections, liabilities, disclosures, and error resolution.

Watch on YouTube: Electronic Funds Transfer (EFT)

That distinction matters in the financial crime environment because the legal treatment of EFTs and the operational risks attached to them are not identical. Regulation E is heavily concerned with consumer rights, liability, disclosures, and error resolution, whereas AML and fraud frameworks focus more on how electronic transfers can be misused to move criminal proceeds, extract funds, or exploit customer accounts. In practice, the same electronic payment activity may therefore have both a consumer-protection dimension and a financial crime-control dimension. For example, an unauthorized EFT may trigger Regulation E error-resolution obligations while also indicating account takeover, social engineering, or mule-account activity.

EFTs are especially relevant to fraud because they often combine speed with familiarity. Customers use electronic transfers for payroll, bill payment, recurring debits, online purchases, peer-to-peer transfers, and general account management. Because these are routine activities, suspicious transfers may not stand out immediately unless the institution understands the customer’s normal behavior and the context of the transaction. The CFPB materials show how broad the EFT category is in the consumer environment, while the FFIEC’s funds transfer overview emphasizes the need for effective monitoring and reporting systems to manage AML risk associated with transfer activity.

In fraud terms, EFTs can be exploited through unauthorized debits, unauthorized credits, credential compromise, account takeover, ACH abuse, scam-induced payments, and misuse of preauthorized transfers. Regulation E’s framework around consumer liability and error resolution exists precisely because EFTs can be misused in ways that directly harm account holders. At the same time, the FFIEC’s AML guidance highlights that transfer activity can present money laundering and terrorist financing risk, especially where systems do not adequately monitor for unusual patterns or where the institution cannot explain the purpose and expected behavior of the account.

This makes EFT a particularly important concept at the intersection of payments, fraud, and AML. A transfer may be an ordinary payroll deposit, a legitimate bill payment, or a recurring subscription debit. It may also be the mechanism through which a victim loses funds, a mule account receives proceeds, or suspicious payments are layered across multiple accounts. The control challenge is therefore not to treat all EFTs as high risk, but to distinguish ordinary electronic activity from patterns that are inconsistent with the customer profile, account purpose, or normal transaction behavior. That is an inference supported by the breadth of EFT use and the FFIEC’s expectation that institutions manage transfer-related AML risks through effective systems and monitoring.

A mature financial crime framework typically addresses EFT risk through layered controls. These include onboarding controls, customer authentication, account-access security, transaction monitoring, behavioral analytics, sanctions screening where relevant, ACH or transfer-specific exception monitoring, and clear case escalation procedures. In consumer contexts, firms also need strong Regulation E compliance processes for error resolution and customer protection. The CFPB makes clear that Regulation E establishes basic rights, liabilities, and responsibilities for consumers and institutions involved in electronic fund transfer services, which means EFT risk management must consider both crime prevention and customer treatment.

Ultimately, EFT is a core concept in the financial crime environment because it describes the electronic movement of money through systems that are now fundamental to everyday banking. Those systems support legitimate consumer and commercial activity at scale, but they also create opportunities for fraud, account abuse, and suspicious fund movement. For that reason, EFT should be understood not just as a payment convenience or a legal definition, but as a major control surface where consumer protection, fraud prevention, and AML oversight all meet.