The Dodd–Frank Wall Street Reform and Consumer Protection Act is the major U.S. post-crisis financial reform statute enacted in 2010 to strengthen financial stability, increase transparency, address regulatory gaps, and improve consumer and market protections. The enrolled Act itself identifies those reform purposes, and the SEC has described Dodd–Frank as creating extensive new responsibilities aimed at reducing systemic risk, enhancing transparency, and better protecting investors.

In the financial crime environment, Dodd–Frank is significant not because it is a single AML law, but because it reshaped the regulatory architecture around banks, derivatives, consumer finance, market oversight, whistleblowing, and systemic-risk supervision. Those reforms affect how misconduct is detected, how risky products are governed, how customer harm is addressed, and how regulators gain visibility into conduct that may intersect with fraud, manipulation, abusive practices, and broader financial crime. The SEC has said the Act created a new regulatory framework for derivatives and expanded its responsibilities in areas including credit ratings, asset-backed securities, private fund advisers, and executive compensation, while the CFTC’s current organizational materials reflect its ongoing role in overseeing derivatives markets for fraud, manipulation, and abusive practices.

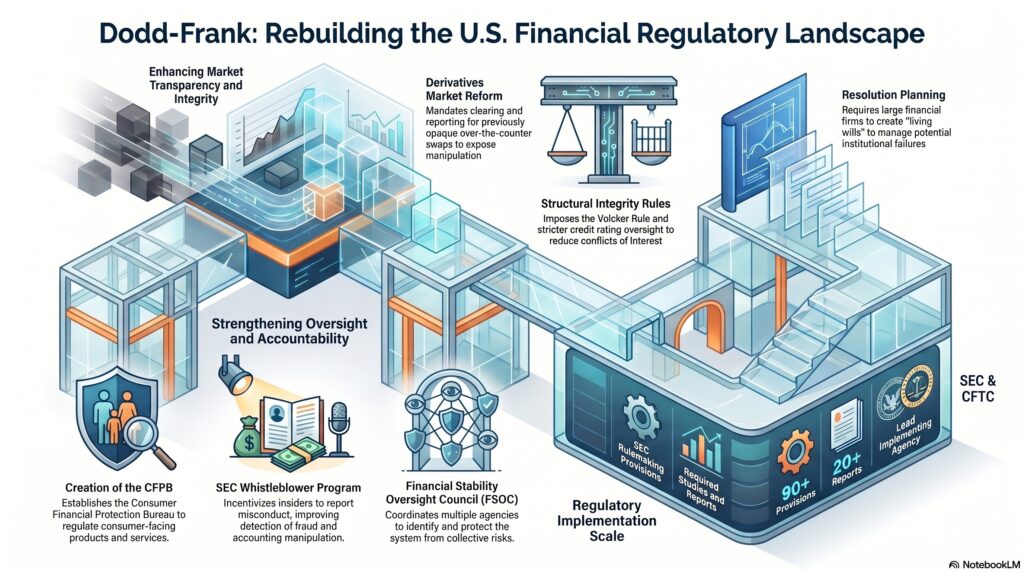

A central financial-crime-relevant feature of Dodd–Frank is its treatment of the derivatives markets. The Act established major reforms for swaps and related derivatives trading, including clearing, trading, and reporting requirements intended to make previously opaque over-the-counter activity more visible and better regulated. The SEC has explicitly stated that the Act created a new regulatory framework for derivatives and required mandatory clearing and trading of certain derivatives through regulated entities, while the CFTC continues to describe its role as oversight of futures, options, and swaps markets. In practical terms, that matters because opacity and weak oversight in complex markets can make manipulation, misreporting, concealment of exposures, and related misconduct harder to detect.

Dodd–Frank is also highly relevant because it created the Consumer Financial Protection Bureau (CFPB). The SEC’s summary of the Act states that Dodd–Frank created the CFPB to regulate consumer financial products and services, particularly in response to failures revealed by the mortgage crisis. In the financial crime environment, that matters because many frauds, abusive practices, and unfair treatment issues occur in consumer-facing products, and stronger consumer-protection architecture can reduce the scope for misconduct and improve how harms are addressed.

Watch on YouTube: Dodd–Frank Wall Street Reform and Consumer Protection Act

Another major area of relevance is systemic-risk oversight and resolution planning. The enrolled Act created the Financial Stability Oversight Council (FSOC) and the SEC later described FSOC as serving an important role in coordinating work to protect against risk and support financial stability. Dodd–Frank also introduced a resolution framework for covered financial companies under Title II. In financial-crime terms, these reforms matter because weak institutional resilience, poor governance, and opaque interconnected exposures can magnify the consequences of fraud, manipulation, or other major misconduct once stress emerges in the system.

The Act also has strong relevance to market integrity and accountability. The SEC has said Dodd–Frank increased its role in regulating credit rating agencies, strengthened regulation of asset-backed securities, and imposed new restrictions through the Volcker Rule and other reforms. These changes matter in the financial crime environment because they address structural weaknesses that can create room for conflicts of interest, misleading disclosures, abusive risk transfer, and distorted incentives. This is an inference from the SEC’s description of Dodd–Frank reforms in credit ratings, securitization, and proprietary activities as measures aimed at integrity, transparency, and financial stability.

Dodd–Frank is also important because of its whistleblower framework. The SEC stated that Section 922 of the Act established the SEC whistleblower program, which pays awards to eligible whistleblowers whose original information leads to successful enforcement actions. In the financial crime environment, this is highly significant because internal misconduct, fraud, accounting manipulation, market abuse, and governance failures are often first identified by insiders rather than by surveillance systems alone. A stronger whistleblower regime improves the chance that concealed misconduct will surface before it causes wider harm.

From a professional compliance perspective, Dodd–Frank is best understood as a framework statute rather than a single-topic law. It did not just create one new rule. It redistributed authority, imposed rulemaking obligations, created new institutions, enhanced reporting and transparency, and changed the oversight model across multiple parts of the U.S. financial system. The SEC said the Act required the largest and most complex rulemaking agenda in its history and involved some 90 provisions requiring SEC rulemaking plus more than 20 studies or reports. That scale is one reason Dodd–Frank remains central to discussions of governance, transparency, consumer protection, market conduct, and systemic oversight.

In the financial crime environment, the practical significance of Dodd–Frank is therefore indirect but substantial. It strengthens the institutional conditions in which financial crime controls operate: more transparent derivatives markets, stronger consumer-finance oversight, more explicit systemic-risk coordination, greater scrutiny of ratings and securitization, enhanced whistleblower channels, and broader supervision of market participants. None of this means Dodd–Frank is itself an AML manual. It means the Act reshaped the regulatory ecosystem in ways that affect how fraud, manipulation, abusive conduct, and broader financial instability are prevented and exposed. That conclusion is an inference drawn from the Act’s structure and the SEC’s description of its implementation priorities.

Ultimately, the Dodd–Frank Act matters in the financial crime environment because it is one of the defining U.S. reform statutes for post-crisis governance, transparency, and accountability. It changed how regulators supervise risk, how markets are structured, how consumers are protected, and how misconduct can be surfaced and addressed. For firms operating in the U.S. regulatory environment, Dodd–Frank is not simply historical background; it remains a foundational part of the control and oversight landscape within which modern financial crime risk is managed.