Detection management capabilities are the combined people, processes, data, technology, governance, and investigative arrangements that allow a firm to identify, triage, assess, escalate, and refine indicators of financial crime risk. In the financial crime environment, this is broader than having a monitoring system or a few alert rules. It is the institution’s overall ability to convert raw signals into defensible risk decisions and timely intervention. The FCA’s Financial Crime Guide states that effective systems and controls help firms detect, prevent, and deter financial crime, while the FFIEC frames internal controls and suspicious-activity processes around monitoring, identifying, researching, and reporting unusual activity.

From a professional perspective, detection management capabilities matter because financial crime is rarely visible through a single isolated datapoint. Suspicious behavior often emerges through combinations of signals: unusual onboarding characteristics, abnormal account behavior, sanctions or adverse media links, alert history, communications, geographies, counterparties, and transactional patterns. A firm may have screening, transaction monitoring, fraud tools, and case-management platforms, but if those components are fragmented or poorly governed, its actual detection capability can still be weak. FCA guidance on transaction monitoring and financial crime systems and controls reflects this by focusing on how firms implement and monitor systems, not merely whether those systems exist.

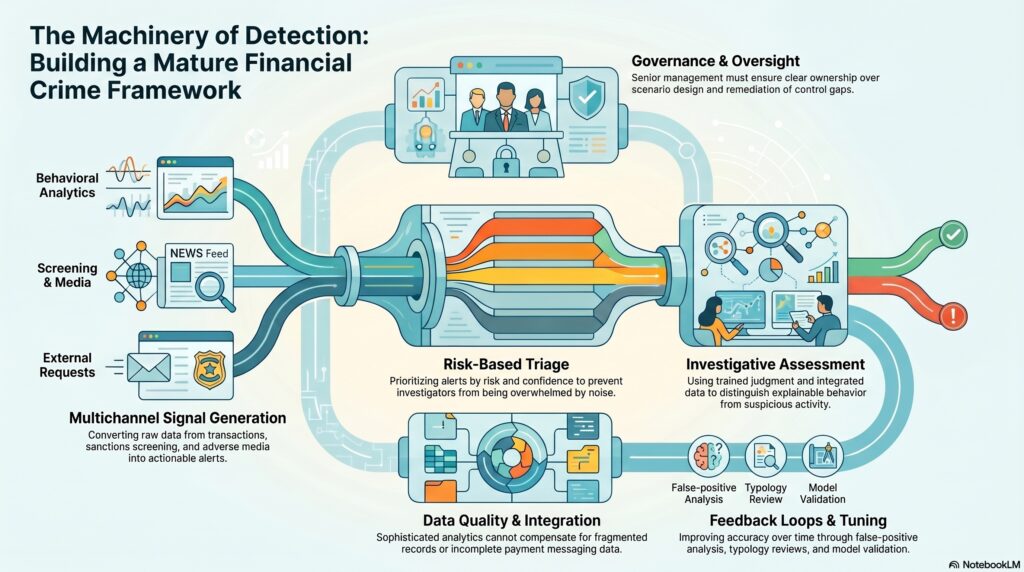

A mature detection management capability usually starts with signal generation. This includes alerts and indicators arising from transaction monitoring, sanctions screening, customer due diligence, behavioural analytics, fraud monitoring, communications surveillance, employee escalation, adverse media, or law-enforcement requests. But signal generation is only the beginning. Strong firms also need triage, meaning a structured way to prioritize alerts according to risk, context, confidence, and potential harm. Without triage, firms can become overwhelmed by alert volumes and lose the ability to distinguish high-value cases from background noise. The FFIEC suspicious-activity examination procedures explicitly emphasize mapping the process used to monitor for, identify, research, and report suspicious activity, which reflects the importance of end-to-end design.

Watch on YouTube: Detection Management Capabilities

The next critical element is investigative capability. Detection is not effective unless the firm can assess what an alert actually means. That requires trained investigators, clear escalation criteria, usable case-management tools, access to relevant customer and transaction data, and enough subject-matter judgment to distinguish explainable behavior from activity that is unusual, suspicious, or prohibited. In practical terms, many control failures occur not because a signal was absent, but because the organization could not evaluate it properly, did not connect it to wider activity, or closed it without sufficient challenge. This is consistent with FFIEC expectations around researching and reporting suspicious activity and with the FCA’s broader focus on effective controls rather than formal process alone.

Detection management capabilities also depend heavily on data quality and integration. If customer records are fragmented, beneficial ownership data is weak, payment messages are incomplete, device data is unavailable, or screening results are not linked to monitoring outputs, the institution’s ability to detect meaningful patterns deteriorates quickly. FATF’s risk-based guidance and technology guidance both support the view that firms need usable information, proportionate controls, and well-governed implementation if technology is to improve AML/CFT outcomes. In other words, sophisticated analytics cannot compensate for structurally poor data.

Another important dimension is coverage. Effective detection management means understanding which risks are actually being monitored and which are not. A firm may have strong sanctions screening but weak fraud analytics, or good transaction monitoring for cash activity but weak controls for electronic payments, trade finance, cryptoasset activity, or nested correspondent flows. FCA guidance and FFIEC materials both point toward risk-based coverage, meaning that the scope and intensity of monitoring should reflect the institution’s business model, products, customers, delivery channels, and geographic exposure. Detection capability is therefore inseparable from the firm’s financial crime risk assessment.

A professionally mature framework also includes feedback loops and tuning. Detection capabilities should improve over time through quality assurance, typology reviews, root-cause analysis, alert sampling, false-positive analysis, model validation, and incorporation of emerging criminal techniques. FCA policy materials on transaction monitoring explicitly reference implementation, monitoring, and responsible innovation, including new approaches such as artificial intelligence. That reflects an important principle: detection management is not static. If typologies evolve but scenarios and review logic do not, the control environment becomes progressively less effective.

Governance is central throughout. Detection management capabilities require clear ownership over scenario design, threshold setting, screening logic, alert handling, escalation, reporting, remediation, and change control. Senior management should understand not just how many alerts are produced, but whether the system is surfacing the right risks, whether investigators are keeping pace, whether backlogs are growing, whether true positives are being learned from, and whether control gaps are being remediated. FCA and FFIEC materials both emphasize systems and controls, internal controls, and compliance with monitoring and suspicious-activity processes, which all point back to governance quality as a determinant of effectiveness.

Ultimately, detection management capabilities are the practical machinery through which a firm turns financial crime risk into observable, actionable intelligence. They determine whether unusual behavior is noticed, whether serious cases are prioritized, whether investigators can make sound judgments, and whether lessons from past cases improve future detection. In the financial crime environment, this is one of the clearest indicators of whether a firm’s control framework is real and operational or merely formal.