Compliance is the framework through which an organization identifies, interprets, applies, and monitors the legal, regulatory, and internal requirements that govern its activities. In the financial crime environment, compliance is the discipline that translates obligations relating to anti-money laundering, sanctions, fraud prevention, anti-bribery and corruption, market conduct, customer due diligence, suspicious activity reporting, and related controls into practical operating standards. FCA guidance on financial crime systems and controls frames this as the need for firms to establish and maintain effective systems and controls to counter the risk that they might be used to further financial crime.

From a professional financial crime perspective, compliance is not simply about avoiding breaches or maintaining policies on paper. It is a core governance function that helps ensure the institution operates within its legal and ethical obligations while managing exposure to criminal misuse. FATF’s risk-based guidance for the banking sector makes clear that firms are expected to identify, assess, understand, and mitigate money laundering and terrorist financing risks in a proportionate way. In practice, compliance provides the structure through which that expectation is implemented, challenged, documented, and maintained over time.

In the financial crime environment, compliance typically spans several interdependent areas. These include customer due diligence, enhanced due diligence, sanctions screening, transaction monitoring, fraud risk governance, suspicious activity escalation, regulatory reporting, training, policy management, quality assurance, and oversight of remediation. Depending on the firm, compliance may also cover market abuse, conflicts of interest, communications surveillance, anti-bribery controls, and broader conduct risk. What connects these areas is the need to convert complex obligations into repeatable, evidence-based control processes. The FCA’s Financial Crime Guide and related materials repeatedly emphasize that governance, monitoring, training, and management information are all part of an effective compliance control environment.

Watch on YouTube: Compliance

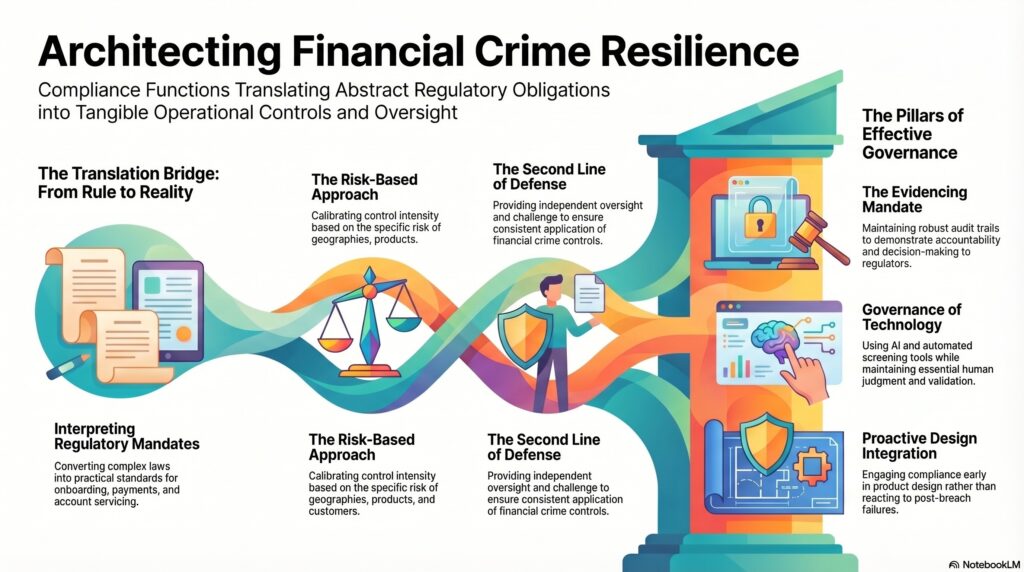

A central feature of compliance is that it operates between regulation and business activity. Laws and rules are often written at a high level, while actual customer onboarding, payments processing, trading, lending, or account servicing happens in detailed operational environments. Compliance helps bridge that gap by interpreting requirements, setting standards, advising on implementation, and challenging where business practices create unacceptable risk. This is why compliance is often most valuable not when it reacts to a breach, but when it is involved early in product design, control changes, escalation decisions, and risk assessments. FCA supervisory materials on financial crime consistently point to the importance of effective systems and controls rather than reactive correction alone.

The risk-based approach is fundamental here. Compliance is not expected to apply identical scrutiny to every customer, product, or transaction regardless of risk. Instead, it should help the firm determine where exposure is greatest and how controls should be calibrated accordingly. Higher-risk geographies, customer types, products, channels, and transaction patterns may require stronger due diligence, closer monitoring, or tighter escalation standards. FATF explicitly endorses this risk-based approach, and modern financial crime compliance depends on it because no institution can manage complex risks effectively through uniform treatment alone.

Compliance also plays a critical role in oversight and challenge. It is often positioned in the second line of defence, overseeing how the first line manages day-to-day financial crime risks and whether controls are being applied consistently. That means compliance is not usually the only owner of financial crime risk, but it is a key owner of policy, oversight, standards, escalation, and independent challenge. A mature compliance function should therefore be able to assess whether customer files are complete, whether transaction monitoring is meaningful, whether sanctions screening is effective, whether training is adequate, and whether weaknesses are being remediated in a timely way. FCA guidance directly links senior management oversight and effective internal control to credible financial crime frameworks.

Another important dimension is evidencing. In regulated environments, it is not enough for a firm to say that it takes compliance seriously. It must be able to show how it identified risks, what policies and procedures are in place, how controls operate, how decisions were made, who approved them, and what remediation occurred when problems were found. This makes documentation, management information, case records, training records, and audit trails central to compliance effectiveness. The FFIEC BSA/AML Manual in the U.S. similarly emphasizes program assessment, risk-based controls, and evidencing of compliance as core supervisory expectations.

Technology increasingly supports compliance, but does not replace it. Screening systems, monitoring tools, case-management platforms, behavioral analytics, and AI-supported investigations can improve scale and consistency, yet they still require strong governance, validation, and human judgment. FATF’s technology guidance notes that new technologies can enhance AML/CFT efforts, but also highlights implementation and governance challenges. In practice, compliance must ensure that technology is aligned to the firm’s risk profile, properly calibrated, understandable enough to defend, and subject to review when outputs are weak or unexpected.

Ultimately, compliance is central to the financial crime environment because it provides the structure through which obligations become operating reality. It helps firms understand risk, build defensible controls, oversee implementation, challenge weaknesses, and demonstrate accountability to regulators and stakeholders. Without effective compliance, even well-designed policies and sophisticated systems can fail in practice. For that reason, compliance should be understood not as an administrative function, but as a core component of organizational governance, control credibility, and financial crime resilience.