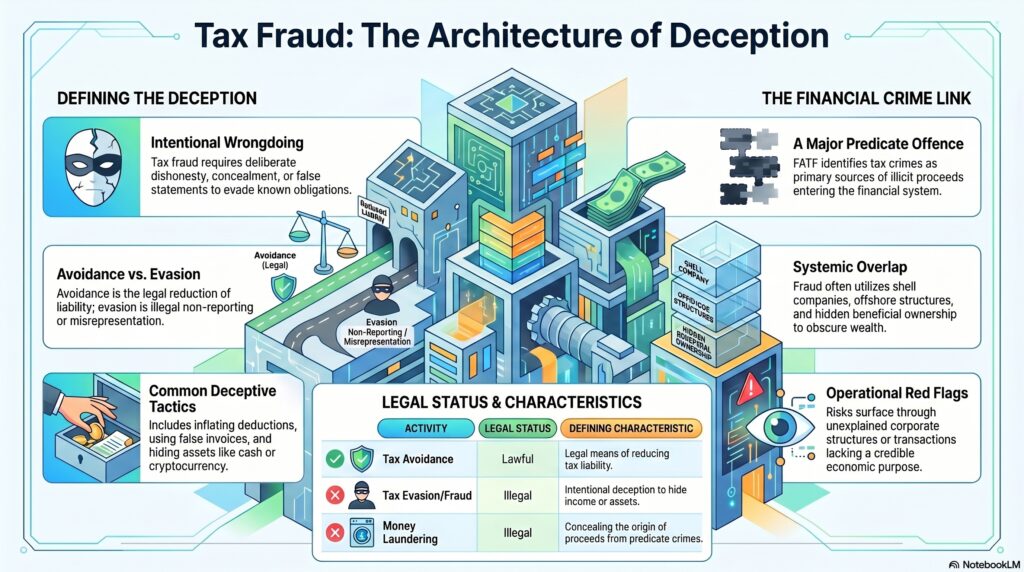

Tax fraud is the deliberate and dishonest evasion of tax obligations through deception, concealment, false statements, or other intentional wrongdoing. The IRS defines tax fraud as intentional wrongdoing with the specific purpose of evading a tax known or believed to be owing, and distinguishes illegal tax evasion from lawful tax avoidance. HMRC similarly describes tax fraud as deliberate and dishonest conduct aimed at defrauding the tax authority by evading tax, stealing public funds, or cheating the system.

In the financial crime environment, tax fraud matters because it is both a serious offence in its own right and a major predicate crime for money laundering. FATF’s Recommendations require countries to apply the money laundering offence to all serious offences, and FATF’s risk materials specifically identify tax crimes among the major predicate offences whose proceeds may enter the financial system for laundering.

From a professional perspective, tax fraud is not just underpayment of tax or a technical filing error. The defining feature is intentional deception. That can include hiding income, understating revenue, inflating deductions, using false invoices, concealing beneficial ownership, misrepresenting cross-border arrangements, or hiding assets, cash, or crypto from the tax authority. The IRS and HMRC both frame the issue around deliberate dishonesty rather than innocent mistake.

Watch on YouTube: Tax Fraud

This distinction matters because lawful tax avoidance and unlawful tax evasion/fraud are not the same. IRS materials state that tax avoidance is a legal means of reducing tax liability, while tax evasion is the illegal act of not reporting income, underreporting income, or providing false information. In the financial crime environment, that distinction is essential because not every tax-efficient structure is suspicious, but deceptive concealment and false reporting can indicate fraud and wider financial crime risk.

Tax fraud also matters because it often overlaps with other control concerns such as shell companies, offshore structures, false invoicing, hidden beneficial ownership, and movement of assets across accounts or jurisdictions. HMRC’s reporting channels expressly include hiding or moving assets, cash, or crypto and even sanctions-related import/export abuse as matters that may be part of tax fraud reporting. That shows how tax fraud can connect to broader illicit-finance typologies rather than existing as an isolated tax issue.

For firms, the practical relevance is that tax fraud may surface through customer due diligence, source-of-wealth reviews, unexplained corporate structures, unusual transaction patterns, false commercial narratives, or suspicious movement of value that lacks credible economic purpose. In AML terms, the question is not only whether tax was underpaid, but whether the financial system is being used to conceal proceeds or disguise the true ownership, location, or origin of wealth. This is an inference supported by FATF’s treatment of tax crimes as predicate offences and by its beneficial ownership work linking corporate opacity to tax crimes and other illicit conduct.

Ultimately, tax fraud is significant in the financial crime environment because it combines deliberate deception, unlawful financial gain, and strong links to money laundering risk. It undermines public revenue, distorts fair competition, and can generate illicit proceeds that are later concealed through the financial system. For that reason, tax fraud should be understood not merely as a tax-administration issue, but as a core financial crime typology with direct relevance to AML, due diligence, and suspicious activity detection.