A Suspicious Activity Report (SAR) is a formal report made to the relevant authority when a firm knows, suspects, or has reason to suspect that activity may involve money laundering, terrorist financing, fraud, sanctions-related concerns, or other criminal conduct, depending on the jurisdiction and reporting regime. In the U.S., FinCEN describes the SAR as the principal reporting form used by financial institutions to report suspicious activity, and the FFIEC states that suspicious activity monitoring and reporting are critical internal controls. In the UK, the National Crime Agency says SARs alert law enforcement to potential instances of money laundering or terrorist financing and are a vital source of intelligence on a wide range of criminal activity.

In the financial crime environment, the SAR matters because it is the point where internal suspicion becomes a formal intelligence input to public authorities. Monitoring systems, red flags, frontline concerns, and investigations all matter, but they only become part of the national intelligence and enforcement framework when they are escalated into a SAR. The NCA’s March 2026 SARs Reporter Booklet says SARs provide intelligence such as phone numbers, addresses, company details, investment activity, bank accounts, and asset information, and that they have supported investigations into fraud, trafficking, terrorism financing, and other serious crime.

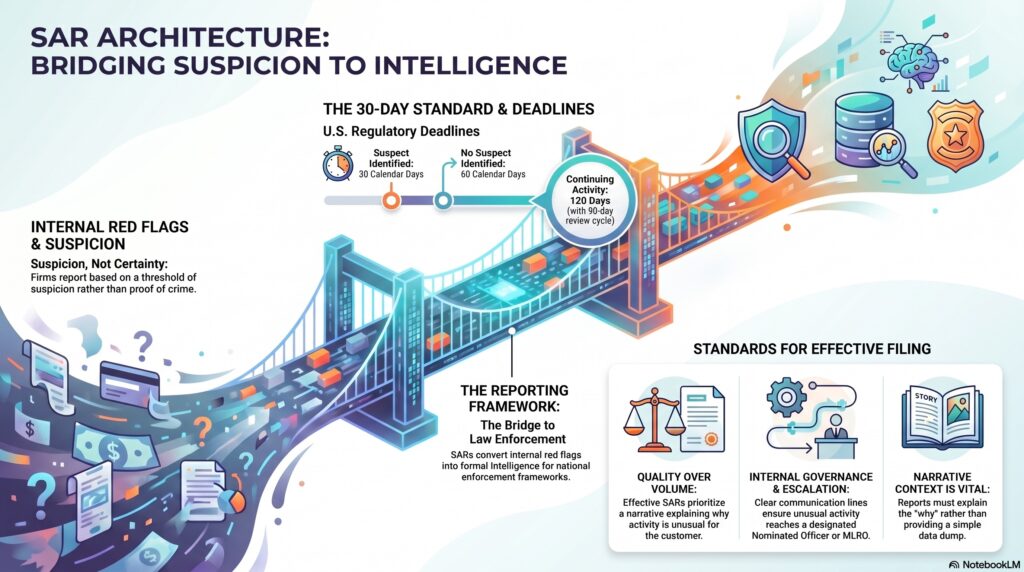

From a professional perspective, a SAR is not a conclusion that a crime has definitely occurred. It is a report that the institution has reached the threshold of suspicion based on the facts available. That threshold matters because firms are not expected to prove the offence before reporting. The FFIEC’s suspicious activity framework focuses on monitoring, identifying, researching, and reporting unusual activity that may expose the bank to illicit use, while FinCEN’s FAQs make clear that the SAR regime is designed to capture concerns once suspicion arises, not only after certainty exists.

Watch on YouTube: Suspicious Activity Report (SAR)

A key practical distinction is that the meaning and mechanics of SAR filing are jurisdiction-dependent. In the U.S., banks generally must file a SAR within 30 calendar days after the initial detection of facts that may constitute a basis for filing; if no suspect is identified at that point, filing may be delayed up to an additional 30 days, but not beyond 60 calendar days from initial detection. The FFIEC also notes that continuing suspicious activity is generally reviewed on a 90-day cycle, with follow-on filing deadlines at 120 days after the previous related SAR filing in the relevant circumstances.

In the UK, the FCA states that the nominated officer has a legal obligation to report knowledge or suspicions of money laundering to the National Crime Agency through a SAR, and the NCA describes SARs as a core intelligence channel used by financial institutions and other professionals. This makes the SAR central not only to AML operations, but also to internal escalation structures such as the MLRO or nominated officer function.

The SAR is also important because its value depends heavily on quality, not just filing volume. The FFIEC’s SAR Quality Guidance says the SAR should explain as fully as possible why the activity is unusual for the customer, taking into account the products and services involved and the customer’s expected activity. In practice, that means a good SAR is not just a data dump or alert summary. It should explain what happened, why it is suspicious, how it differs from expected behavior, and what relevant parties, accounts, dates, and instruments are involved.

This is why SARs sit at the center of a broader governance framework. A firm needs clear lines of communication for referral of unusual activity, designated individuals responsible for identifying, researching, and reporting suspicious activities, and processes for documenting decisions not to file where concerns were reviewed but did not meet the reporting threshold. The FFIEC examination procedures explicitly look for these governance features.

In practical financial crime terms, SARs are relevant across many typologies: structuring, fraud, mule activity, suspicious wire activity, market-related money laundering concerns, sanctions-adjacent evasion indicators, and other unexplained patterns. FinCEN’s October 2025 FAQs specifically addressed issues such as structuring SARs, continuing activity reviews, and decisions not to file, showing that the SAR framework remains a live and evolving supervisory topic.

Ultimately, the SAR is one of the most important reporting mechanisms in the financial crime environment because it connects private-sector detection to public-sector intelligence and enforcement. It is the formal pathway through which suspicion is documented, escalated, and made available for broader investigative use. Without effective SAR governance and filing quality, much of the value of transaction monitoring, red flags, and suspicious activity detection is lost.