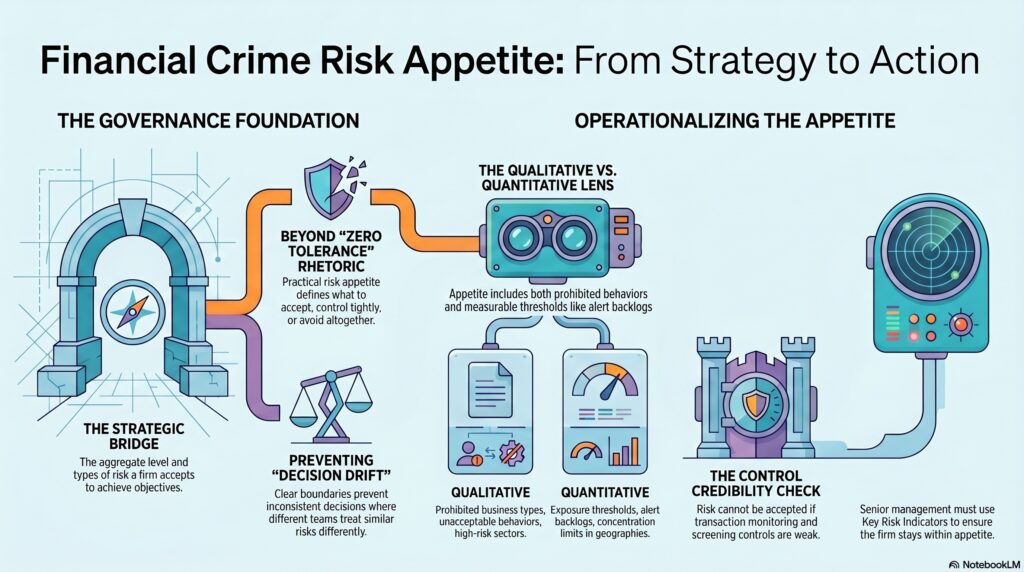

Risk appetite is the amount and type of risk a firm is willing to accept in pursuit of its objectives. Basel materials define it as the aggregate level and types of risk a bank is willing to assume, decided in advance and within its risk capacity, to achieve its strategic objectives and business plan. The Bank of England’s current regulatory expectations similarly say risk appetite must be well defined, clearly articulated, realistic, and linked to the firm’s overall strategy.

In the financial crime environment, risk appetite matters because it determines where the firm is prepared to do business, under what conditions, and with what level of control. It is the governance mechanism that turns abstract concern about money laundering, fraud, sanctions, bribery, market abuse, or customer harm into operational boundaries and decision rules. Without a clear risk appetite, firms often drift into inconsistent decisions: one team accepts a higher-risk customer, another rejects a similar one, and management cannot explain why. This is an inference supported by Basel’s definition of risk appetite as something set in advance and linked to strategic objectives.

From a professional perspective, risk appetite is not the same as risk tolerance, risk capacity, or zero tolerance rhetoric. A firm may say it has zero tolerance for financial crime, but in reality it still has to make decisions about serving higher-risk sectors, onboarding PEPs, operating in higher-risk jurisdictions, processing complex payment flows, or supporting products that carry elevated misuse risk. The practical question is not whether the firm likes risk, but which risks it will accept, which it will control more tightly, and which it will avoid altogether. The Basel and Bank of England materials support this by linking risk appetite to strategic objectives, measurable performance, and governance challenge.

Watch on YouTube: Risk Appetite

In the financial crime environment, risk appetite should shape several things directly. It should influence customer acceptance standards, jurisdictional exposure, product design, correspondent relationships, sanctions exposure, thresholds for escalation, use of enhanced due diligence, and the firm’s willingness to service higher-risk business models. The FCA’s Financial Crime Guide is built around effective systems and controls for managing financial crime risk, and its sanctions chapter specifically asks whether senior management has set a clear risk appetite in relation to sanctions risks, including exposure to sanctioned persons, activities, and jurisdictions.

This makes risk appetite a board and senior management issue, not just a compliance concept. A credible risk appetite should be approved, challenged, and monitored at senior level because it reflects how the firm intends to balance commercial opportunity against control capability and regulatory exposure. The Bank of England’s regulatory expectations say firms should demonstrate the internal governance process used to review, challenge, and agree their risk appetites.

A mature financial crime risk appetite is also both qualitative and quantitative. Qualitative statements might define prohibited business types, unacceptable customer behaviors, or sectors requiring senior approval. Quantitative elements might include thresholds for exposure, alert backlogs, unresolved sanctions matches, onboarding turnaround under enhanced due diligence, or concentration limits in higher-risk geographies or products. The Bank of England explicitly says risk appetite should be clearly articulated from both a quantitative and qualitative perspective.

Another important point is that risk appetite is only credible if it is aligned to control effectiveness. A firm cannot sensibly accept higher-risk customers or products if its transaction monitoring, sanctions screening, fraud controls, staffing, or escalation capability are weak. The FCA’s financial crime guidance and its more recent findings on risk assessment and controls both point back to the importance of understanding, assessing, and mitigating risk effectively, not just stating policy positions.

This is why risk appetite should connect directly to management information and governance reporting. Senior management should be able to see whether the firm is operating within appetite, where exceptions are occurring, whether residual risk is rising, and whether controls remain strong enough to support the exposure being accepted. The Bank of England’s current operational resilience work also refers to the effectiveness of key risk indicators in proactive risk appetite and tolerance monitoring, which reinforces that appetite must be observable and monitored rather than treated as a static statement.

Ultimately, risk appetite is central to the financial crime environment because it defines the boundaries within which the firm is prepared to take financial crime-related risk and the conditions under which that risk is considered acceptable. It is the bridge between business strategy and control reality. When well designed, it helps firms make consistent, defensible decisions. When vague or disconnected from actual capability, it becomes a paper exercise that leaves the firm exposed to inconsistent judgment, control strain, and avoidable regulatory risk.