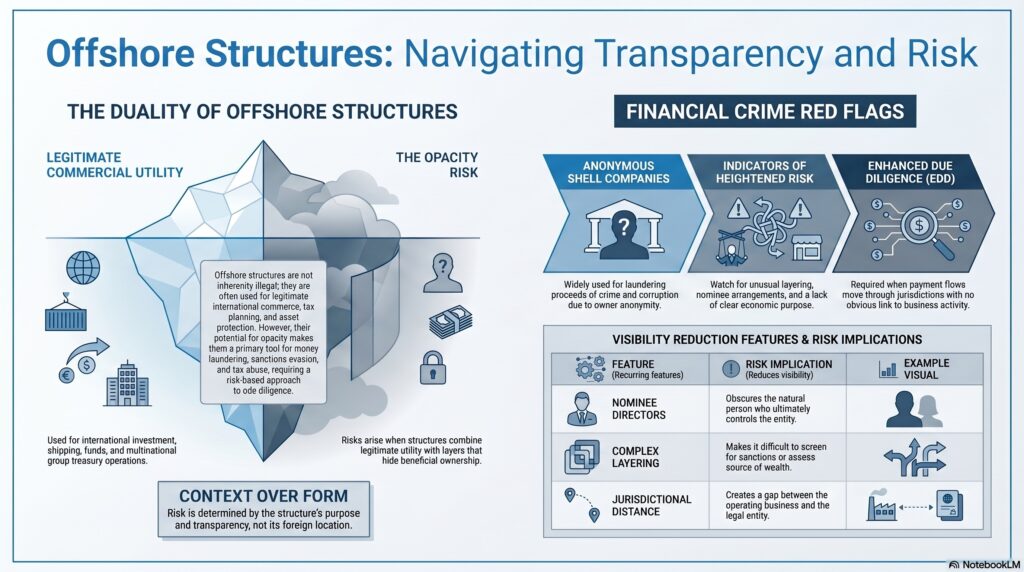

In the financial crime environment, offshore generally refers to assets, entities, accounts, structures, or financial activity located in a jurisdiction outside the customer’s or institution’s home country, often in places used for cross-border holding, trading, tax planning, asset protection, or corporate structuring. The term does not automatically mean illegal or improper. OECD materials refer to offshore financial centres as jurisdictions where a majority of financial transactions are conducted by resident financial corporations on behalf of non-resident clients, and also describe offshore banking centres as places whose financial institutions deal primarily with non-residents.

In the financial crime environment, the significance of “offshore” lies in the fact that offshore structures can combine legitimate commercial utility with increased risks around opacity, beneficial ownership, tax abuse, sanctions evasion, and money laundering. FATF’s beneficial ownership work states that strengthened transparency standards are intended to help identify corrupt actors, sanctions evaders, money launderers, and tax evaders who hide behind shell companies, complex structures, and trusts. The FCA’s Financial Crime Thematic Reviews also identify complex and opaque offshore company structures as a control concern for firms.

From a professional perspective, offshore does not describe one specific legal form. It can refer to offshore companies, trusts, foundations, holding entities, bank accounts, funds, insurance wrappers, or wider structures established outside the main operating jurisdiction. What matters from a financial crime standpoint is not that the structure is foreign, but why it exists, who controls it, how transparent it is, and whether its use makes commercial sense. FATF’s guidance on transparency and beneficial ownership repeatedly emphasizes the need to distinguish legal ownership from the natural persons who ultimately own or control the structure.

Watch on YouTube: Offshore

This is why offshore arrangements are often a focus of customer due diligence and enhanced due diligence. An offshore company may be entirely legitimate, for example in international investment, shipping, funds, treasury, or multinational group structures. But if the structure is unusually layered, lacks clear economic purpose, uses nominee arrangements, or obscures the ultimate beneficial owner, it can create heightened financial crime risk. FATF’s best-practices material notes that anonymous shell companies are among the most widely used methods for laundering the proceeds of crime and corruption.

A key professional point is that offshore is not the same as suspicious by default. The risk is contextual. Many international businesses operate through offshore or low-tax jurisdictions for lawful reasons. The financial crime question is whether the structure’s purpose, ownership, transactions, and governance are credible and proportionate to the customer’s profile. The FCA’s financial crime guidance is built around a risk-based approach, and its thematic review examples specifically warn against failing to understand the reasons for complex and opaque offshore structures.

In practical terms, offshore risk often arises through several recurring features: distance between the operating business and the legal entity; multiple layers of ownership across jurisdictions; use of trusts or foundations; nominee directors or shareholders; weak transparency around beneficial owners; and payment flows that move through jurisdictions with no obvious commercial link to the customer’s stated activity. These factors do not prove wrongdoing, but they can indicate that the offshore element is being used to reduce visibility. This is an inference supported by FATF’s beneficial ownership guidance and the FCA’s concerns about opaque structures.

Offshore arrangements are also relevant because they can complicate sanctions screening, tax transparency, source-of-wealth assessment, and cross-border investigations. If ownership and control are spread across multiple jurisdictions, firms may find it harder to determine who really benefits from the structure, whether sanctioned persons exercise control indirectly, or whether the stated source of funds is credible. FATF’s beneficial ownership work is explicitly aimed at preventing misuse of legal persons and arrangements by sanctions evaders, corrupt actors, and money launderers.

A mature financial crime framework therefore treats offshore exposure as a risk indicator requiring explanation, not as a conclusion in itself. Firms should understand the rationale for the offshore element, verify beneficial ownership, assess whether the structure matches the customer’s business or wealth profile, and monitor whether payments, assets, and counterparties behave consistently with that explanation over time. Where the offshore component is unnecessarily complex, commercially unclear, or resistant to transparency, the risk of misuse increases materially. This is an inference grounded in the cited FATF and FCA materials.

Ultimately, offshore in the financial crime environment refers to cross-border financial and corporate arrangements that may be legitimate but can also create opacity and control challenges. Its relevance lies not in the foreign location alone, but in whether the offshore structure helps explain the business honestly or helps conceal who owns, controls, or benefits from it.