A nested account is an account or relationship in which one financial institution gains access to another institution’s correspondent banking services through an intermediary institution rather than directly. The Wolfsberg Group explains nested relationships as arrangements where a respondent bank uses another financial institution’s correspondent account to access the payment system, and FATF’s correspondent banking guidance discusses the same risk under the broader issue of downstream or indirect access.

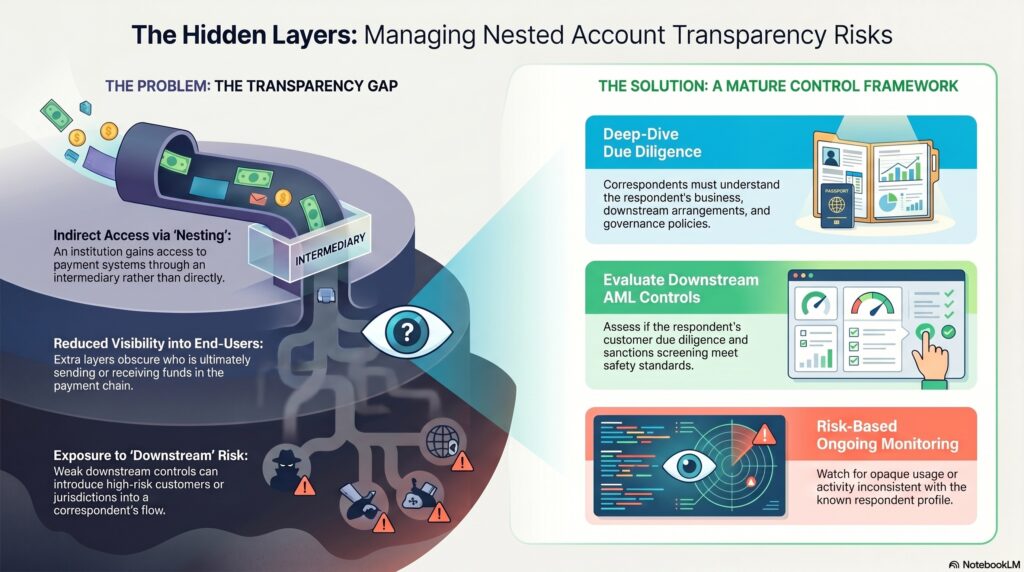

In the financial crime environment, nested accounts matter because they create an additional layer of distance between the institution providing payment access and the institution or customer ultimately using that access. That extra layer can reduce transparency over who is sending or receiving funds, what controls apply downstream, and whether higher-risk activity is entering the payment chain through a respondent the correspondent does not know directly. FATF’s guidance on correspondent banking stresses that correspondents need to understand the respondent’s business, controls, and access arrangements as part of a risk-based approach.

Watch on YouTube: Nested Account

From a professional perspective, the core risk is not that nesting is automatically improper. Nested arrangements can arise for legitimate commercial reasons, especially where smaller institutions rely on larger institutions for access to cross-border payments or major clearing systems. The real issue is whether the correspondent has enough visibility into the respondent’s downstream relationships and control environment to understand who may be using the account indirectly. Wolfsberg notes that nested activity can create heightened AML and sanctions risk where transparency is weak or where downstream institutions are not adequately understood.

This matters because nested accounts can be used to introduce higher-risk customers, institutions, or jurisdictions into a payment flow without a direct relationship between the end participant and the correspondent bank. If the respondent’s customer due diligence, sanctions screening, or transaction monitoring is weak, the correspondent may end up processing activity it would not have accepted directly. In that sense, nested accounts are mainly a control and visibility issue within correspondent banking rather than a standalone product type. This is an inference supported by FATF’s emphasis on respondent due diligence and risk-based monitoring in correspondent relationships.

A mature control framework therefore requires the correspondent to understand whether nesting is permitted, how it is governed, what kinds of downstream institutions or customers may have indirect access, and whether the respondent’s AML, sanctions, and monitoring controls are strong enough to manage that activity. Where nested usage is opaque, inconsistent with the respondent profile, or linked to higher-risk corridors, the risk of money laundering, sanctions evasion, fraud proceeds movement, and other illicit activity increases materially.

Ultimately, a nested account is significant in the financial crime environment because it can allow value to move through the banking system indirectly, making transparency and control more difficult. For that reason, nested arrangements should be understood as a key correspondent-banking risk area requiring strong due diligence, ongoing monitoring, and clear governance over downstream access.