Money laundering is the process of disguising the criminal origin of illicit funds so they can be used as if they came from legitimate sources. UNODC defines it as the processing of criminal proceeds to disguise their illegal origin, and notes that it typically follows three stages: placement, layering, and integration. The FCA treats money laundering risk as the risk that a firm may be used to further money laundering and places it within the broader financial crime control framework for regulated firms.

In the financial crime environment, money laundering is significant because it is the mechanism that allows criminals to enjoy the proceeds of predicate offences without immediately exposing the underlying crime. Fraud, corruption, drug trafficking, tax crime, cybercrime, trafficking, market abuse, and many other serious offences generate illicit proceeds, but those proceeds are less useful to the criminal if they remain obviously connected to the offence. Money laundering is the process that attempts to break that connection. FATF’s work is built around helping countries identify, assess, and mitigate money laundering risks because those risks threaten the integrity of the financial system.

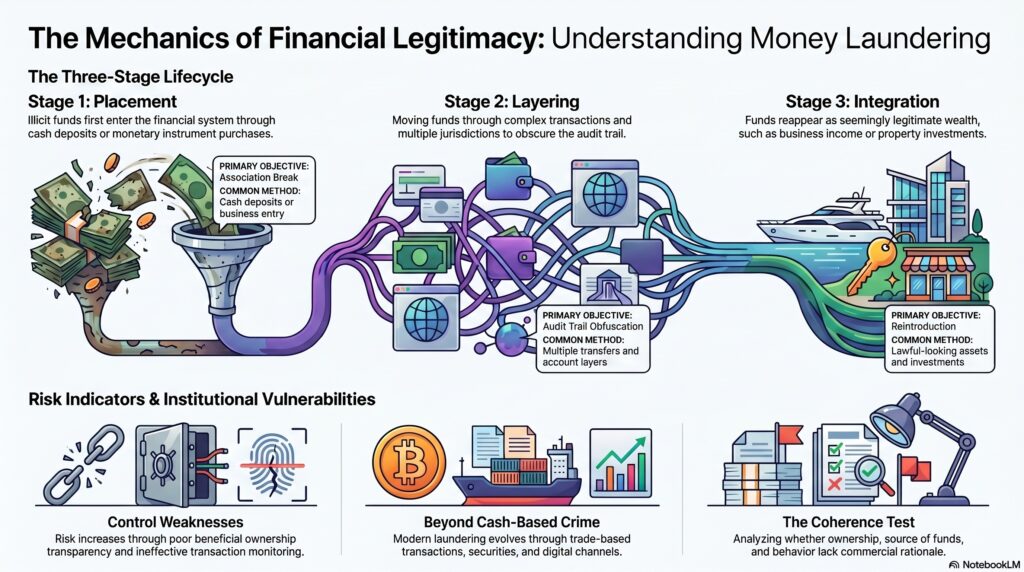

From a professional perspective, money laundering is not simply about moving money. It is about creating apparent legitimacy. The aim is not only concealment, but also usability. Criminals want to convert illicit proceeds into funds, assets, or wealth that can be spent, invested, transferred, pledged, or held with reduced suspicion. UNODC’s overview of the three-stage model captures this clearly: placement moves the funds away from direct association with the crime, layering disguises the trail, and integration makes the money available from what seem to be legitimate sources.

Watch on YouTube: Money Laundering

The classic model begins with placement, where illicit funds first enter the financial system. This may involve cash deposits, purchases of monetary instruments, movement through businesses, or conversion into other forms of value. The second stage is layering, where the funds are moved through multiple transactions, accounts, entities, or jurisdictions to obscure the audit trail. The final stage is integration, where the funds reappear in a form that appears legitimate, such as business income, investments, property proceeds, or other lawful-looking assets. In practice, these stages may overlap, but they remain a useful analytical framework for understanding laundering behavior.

For financial institutions, the central risk is that the firm becomes a channel through which illicit proceeds are placed, disguised, or integrated. That risk may arise through weak customer due diligence, poor beneficial ownership transparency, ineffective transaction monitoring, weak sanctions controls, or poor escalation of suspicious activity. The FCA’s systems-and-controls rules require firms to maintain policies and procedures that enable them to identify, assess, monitor, and manage money laundering risk, and its Financial Crime Guide remains the main supervisory reference point for doing so.

A professionally mature AML framework therefore focuses on several connected questions. Who is the customer really? What is the purpose of the relationship? What activity should be expected? Do the ownership structure, source of funds, and transaction behavior make sense together? Are there unexplained changes in activity, unusual counterparties, high-risk jurisdictions, rapid pass-through movements, or complexity that lacks commercial rationale? These questions matter because money laundering often succeeds when firms verify fragments of information but fail to assess the coherence of the overall picture. This is an inference supported by the FCA’s focus on systems and controls for managing money laundering risk and FATF’s focus on understanding risk exposure.

Money laundering is also broader than traditional cash-based crime. Modern laundering can occur through payments, correspondent banking, trade transactions, corporate structures, securities activity, digital channels, and professional intermediaries. FATF’s materials on trade-based money laundering, for example, describe it as disguising proceeds of crime and moving value through trade transactions to legitimize illicit origins. That illustrates a wider point: laundering techniques evolve with financial systems, which is why effective controls must be risk-based and adaptable rather than limited to one typology.

Ultimately, money laundering is one of the central threats in the financial crime environment because it is the process through which criminal proceeds are hidden, legitimized, and brought into wider economic use. It is not just a criminal-law concept; it is a control risk for every institution that handles customers, transactions, assets, or market activity. For that reason, money laundering should be understood as the core problem that AML frameworks are designed to prevent: the transformation of illicit wealth into apparently legitimate value within the financial system.