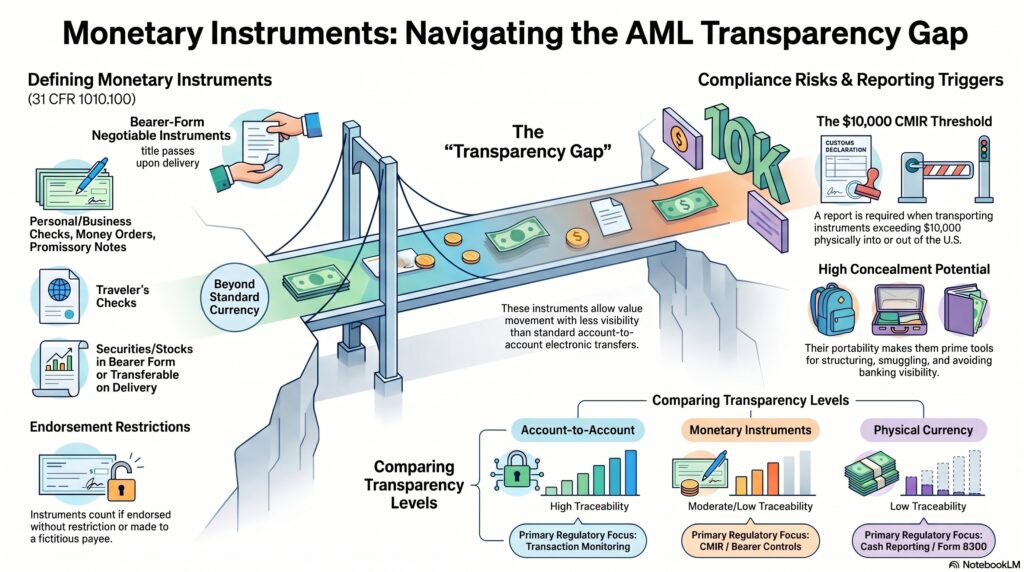

Monetary instruments are forms of money or money-like payment paper that can be transferred, transported, exchanged, or used to move value. In the U.S. Bank Secrecy Act framework, the term has a specific regulatory definition. Under 31 CFR 1010.100(dd), monetary instruments include currency, traveler’s checks, and certain negotiable instruments such as personal checks, business checks, official bank checks, cashier’s checks, third-party checks, promissory notes, and money orders when they are in bearer form, endorsed without restriction, made out to a fictitious payee, or otherwise structured so title passes on delivery. They also include securities or stock in bearer form or otherwise transferable on delivery.

In the financial crime environment, monetary instruments matter because they sit between pure cash and fully traceable account-based payment activity. They are not all the same from a control perspective, but they share one important feature: under certain conditions they can be used to move value with less transparency than standard account-to-account transfers. That is why they appear so often in AML, smuggling, structuring, cash-reporting, and cross-border transportation rules. This is an inference supported by the BSA definition and the specific reporting regime for transporting currency or monetary instruments.

A key reason the term is important is that some monetary instruments can function as portable stores or carriers of value. Currency is the most obvious example, but bearer-form checks, money orders, and similar negotiable instruments can also be moved or transferred in ways that make ownership and destination harder to track. FinCEN’s older rulemaking materials on prepaid access explicitly note that the BSA definition of monetary instruments includes currency and a variety of bearer negotiable instruments, securities, and similar items.

Watch on YouTube: Monetary Instruments

This is why monetary instruments are central to certain reporting obligations. Under 31 CFR 1010.340, a report is generally required when currency or other monetary instruments exceeding $10,000 are physically transported, mailed, shipped, or caused to be transported into or out of the United States. IRS and eCFR materials identify this as the Report of International Transportation of Currency or Monetary Instruments (CMIR) requirement.

From a professional AML perspective, the importance of monetary instruments lies in their potential use for concealment, movement, and conversion of value. A person trying to avoid standard banking visibility may prefer portable instruments, bearer-style negotiable paper, or cross-border transport of value rather than a direct electronic transfer. That does not make monetary instruments inherently suspicious, but it does make them highly relevant to controls around cash-equivalent movement, cross-border reporting, structuring, and suspicious activity review. This is an inference supported by the regulatory definition and CMIR reporting rules.

Monetary instruments are also relevant because the term is used differently depending on context. In the BSA definition, it is relatively broad and includes specific negotiable forms. In some tax and structuring contexts, certain monetary instruments are treated as “cash equivalents” for reporting purposes. IRS materials on Form 8300 industries note that, in designated reporting transactions, certain monetary instruments are included in the definition of cash.

Ultimately, monetary instruments are important in the financial crime environment because they represent transferable value in forms that may be easier to carry, endorse, conceal, or move than ordinary account-based funds. Their legal definition matters operationally because it determines when special reporting, monitoring, and AML controls apply.