The Markets in Financial Instruments Directive, commonly referred to as MiFID and in its current main form as MiFID II, is the EU framework governing investment services, investor protection, and the organization and supervision of securities markets. The European Commission describes MiFID II as part of the revised MiFID framework alongside MiFIR and says it aims to reinforce the rules on securities markets. ESMA’s MiFID II rulebook shows that the framework covers general provisions, investor protection, and market transparency and integrity.

In the financial crime environment, MiFID matters because it shapes the conduct, transparency, governance, and control environment in which investment firms, trading venues, and market participants operate. It is not an AML statute in the narrow sense, but it is highly relevant to financial crime because weak investor-protection controls, poor conflicts management, inadequate order handling, weak surveillance, and opaque market structure can create conditions in which market abuse, misconduct, and wider integrity failures are harder to prevent or detect. This is an inference supported by MiFID II’s focus on investor protection and market transparency and integrity.

From a professional perspective, MiFID is best understood as a market-conduct and market-structure framework. It governs how investment firms behave toward clients, how orders are handled and executed, how information is disclosed, how firms manage conflicts of interest, how trading venues operate, and how competent authorities supervise those activities. ESMA’s MiFID II rulebook explicitly includes sections on provisions to ensure investor protection and on market transparency and integrity, which is why MiFID sits so close to the wider financial crime environment even though it is not primarily framed as an anti-money laundering regime.

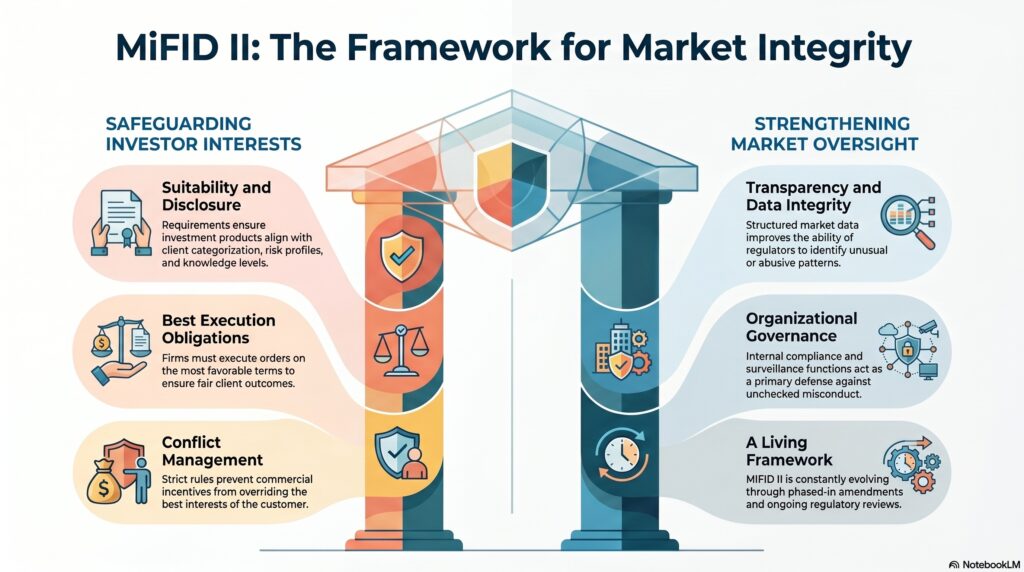

A major reason MiFID is significant is its role in investor protection. MiFID II imposes requirements around client categorization, disclosure, suitability and appropriateness in relevant cases, product governance, conflicts management, and order handling. These controls are important in the financial crime environment because misconduct often emerges where customer interests are subordinated to commercial incentives or where complex products and poor disclosure reduce transparency. ESMA’s materials on MiFID II suitability requirements and the FCA’s MiFID-related guidance both reflect this investor-protection focus.

Watch on YouTube: Markets In Financial Instruments Directive

MiFID is also important because of its order handling and best execution requirements. ESMA’s interactive rulebook includes Article 28 on client order handling rules and Article 27 on the obligation to execute orders on terms most favorable to the client. In practical terms, these provisions strengthen market integrity by reducing the scope for conflicted routing, poor client outcomes, and opaque execution decisions. In the financial crime environment, that matters because weak execution governance can make it harder to distinguish legitimate commercial behavior from conflicted or abusive practices. This is an inference supported by the MiFID II rulebook’s structure and content.

Another important dimension is market transparency and integrity. MiFID II and MiFIR together reshaped transparency and trading requirements across European markets, and ESMA’s current review materials note that amendments to the MiFID II/MiFIR framework are being phased in over time. Better transparency, clearer venue rules, and more structured market data improve the ability of firms and regulators to supervise activity and identify unusual patterns. In the wider financial crime environment, this helps reduce opacity that could otherwise support market abuse or other forms of misconduct.

MiFID is also highly relevant to organizational and compliance controls. ESMA has published guidance on the compliance function under MiFID II, and the FCA continues to interpret MiFID concepts and perimeter questions through its handbook guidance. That matters because MiFID is not only about external market rules; it also affects how firms structure internal governance, compliance oversight, conflicts controls, and operational responsibilities. In a financial crime context, strong organizational controls reduce the likelihood that misconduct, poor client treatment, or market-integrity failures are allowed to develop unchecked.

There is also a current-evolution point worth noting. The MiFID framework is not static. The European Commission and ESMA continue to work on implementing and delegated acts, and ESMA’s review page says revised elements of the MiFID II/MiFIR rulebook will phase in over coming years. That means firms cannot treat MiFID as a fixed historical regime; it remains a live framework with continuing implications for transparency, investor protection, and supervision.

In the UK, MiFID also retains practical relevance even after Brexit. FCA materials continue to interpret MiFID concepts, and the FCA’s prudential and organizational publications still refer to MiFID investment firms and MiFID-scope business. That means MiFID remains part of the regulatory language and control architecture used by UK firms and supervisors, even where the detailed regime has been onshored or adapted.

Ultimately, the Markets in Financial Instruments Directive matters in the financial crime environment because it is one of the core frameworks governing how securities and investment markets operate, how firms treat clients, how orders are handled, and how transparency and integrity are maintained. It is not a classic AML rulebook, but it is a central part of the environment in which market abuse, conflicts, opaque practices, and wider misconduct are prevented or exposed. For that reason, MiFID should be understood as a foundational market-conduct and market-structure framework with direct relevance to the broader financial crime control landscape.