The Markets in Financial Instruments Regulation, or MiFIR, is the EU regulation that sits alongside MiFID II and sets directly applicable rules for transparency, transaction reporting, trading obligations, and access to market infrastructure. ESMA’s rulebook identifies MiFIR as Regulation (EU) No 600/2014, and the European Commission describes it as part of the MiFID II/MiFIR framework for securities markets.

In the financial crime environment, MiFIR is important because it strengthens the data, transparency, and reporting architecture of capital markets. It is not a classic AML law, but it is highly relevant to market integrity and misconduct detection because it improves the visibility regulators and firms have into trading activity, post-trade transparency, and execution patterns. The FCA’s current UK MiFIR transaction-reporting materials state that transaction reports are used for detecting and investigating market abuse, preventing financial crime, monitoring the functioning of financial markets, and supervising firms.

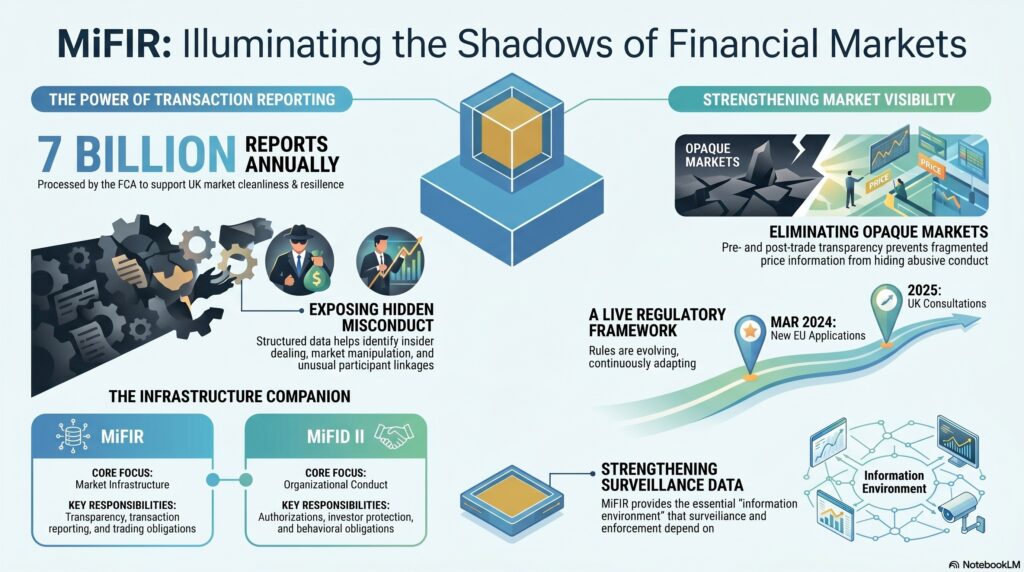

From a professional perspective, MiFIR is best understood as the market-infrastructure and transparency companionto MiFID II. MiFID II focuses more on authorization, organizational requirements, investor protection, and conduct obligations, while MiFIR provides directly applicable market rules on matters such as pre-trade and post-trade transparency, transaction reporting, trading obligations, and access. ESMA’s rulebook and the Commission’s legislation pages reflect this division clearly.

Watch on YouTube: Market In Financial Instruments Regulation

A major reason MiFIR matters in the financial crime environment is transaction reporting. Under UK MiFIR, firms must submit transaction reports after executing transactions in reportable instruments, and those reports include information on the instrument, price, and participants involved. The FCA’s 2025 consultation on improving the UK transaction reporting regime states that these reports are used for detecting and investigating market abuse and preventing financial crime, while the FCA’s 2025 press release notes that it receives more than 7 billion MiFID transaction reports a year used to support the cleanliness, transparency, and resilience of UK markets.

That matters because many forms of misconduct in capital markets are difficult to identify without high-quality trade data. Insider dealing, market manipulation, cross-venue trading patterns, suspicious order behavior, and unusual participant linkages often become more visible when regulators have consistent, structured transaction data. MiFIR therefore contributes to the wider financial crime environment by improving the evidential basis for surveillance and investigation. This is an inference supported by the FCA’s explicit use of MiFIR reporting for market-abuse and financial-crime purposes.

MiFIR is also important because of its role in pre-trade and post-trade transparency. The wider MiFID II/MiFIR framework is described by the European Commission as making financial markets more efficient, resilient, and transparent, and the FCA maintains UK MiFID transparency calculations and transparency waivers and deferrals under the onshored regime. Better transparency matters in the financial crime environment because opaque markets and fragmented price information can make abusive conduct harder to challenge and fair execution harder to evidence.

Another important aspect is that MiFIR is a live and evolving framework. The European Commission said revised MiFIR rules began applying from 28 March 2024, with certain elements phasing in over time, and ESMA’s current MiFID II/MiFIR review pages centralize the amendments and their implications. This matters because firms cannot treat MiFIR as a static post-crisis rulebook; they need to monitor ongoing changes in transparency, reporting, and market-structure obligations.

In the UK, MiFIR remains highly relevant through the onshored UK MiFIR regime. The FCA continues to operate transaction-reporting, transparency, and reporting-infrastructure processes under UK MiFIR, and its 2025 consultation makes clear that the onshored MiFIR transaction-reporting rules remain central to how it supervises markets and detects misconduct.

Ultimately, the Markets in Financial Instruments Regulation matters in the financial crime environment because it provides the reporting and transparency framework that helps make modern securities markets more observable, more governable, and harder to abuse in the dark. It does not replace AML, fraud, or market-abuse law, but it materially strengthens the information environment on which surveillance, enforcement, and market-integrity oversight depend.