Know Your Customer, or KYC, is the framework through which a firm identifies a customer, verifies who they are, understands the nature and purpose of the relationship, and assesses the risk the customer presents. In UK supervisory language, the FCA notes that “customer due diligence” and “Know Your Customer” are sometimes used interchangeably, and its Financial Crime Guide says effective CDD/KYC assessments are a cornerstone of wider financial crime compliance, including sanctions controls.

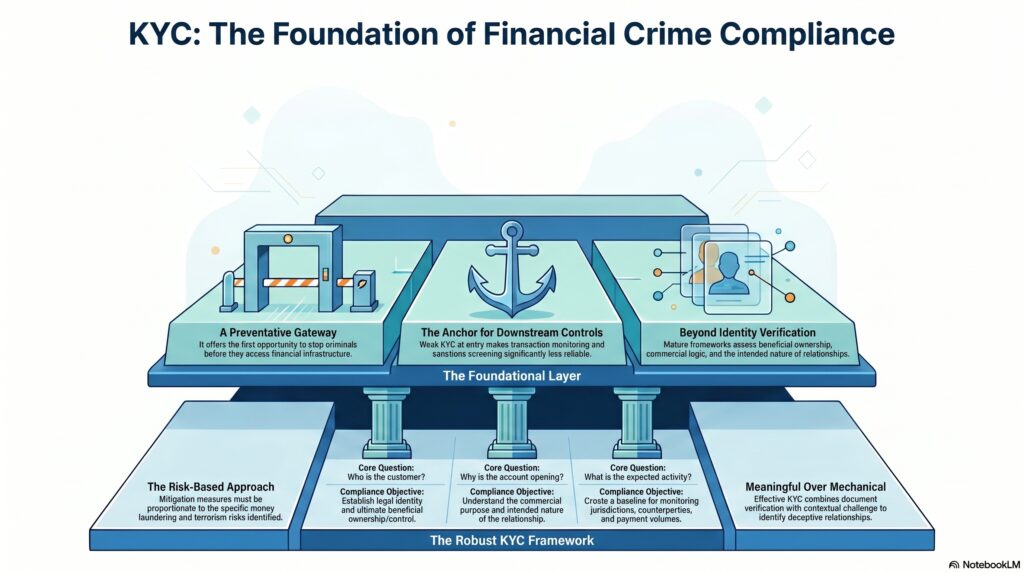

In the financial crime environment, KYC is significant because it is the point at which a firm decides who it is dealing with, why the relationship exists, and whether the risk is acceptable. If that understanding is weak at entry, every downstream control becomes less reliable. Transaction monitoring is harder to interpret, sanctions screening becomes less meaningful, suspicious activity review is weakened, and fraud prevention becomes more reactive than preventive. FATF’s standards and risk-based guidance place customer due diligence at the center of AML/CFT control design for exactly this reason.

From a professional perspective, KYC is broader than identity verification alone. Verifying a passport, company registration, or proof of address is only one part of the process. A mature KYC framework also seeks to understand the customer’s beneficial ownership, purpose of account, expected activity, geographic exposure, products used, and the commercial logic of the relationship. The FCA’s Financial Crime Guide says customer due diligence includes measures to obtain information on the purpose and intended nature of the business relationship, not just identity details.

This is why KYC is a foundational control in the financial crime environment. Criminals often try to enter the financial system using stolen identities, synthetic identities, opaque corporate structures, nominees, front companies, or misleading explanations about source of funds and intended account use. A strong KYC process is one of the first serious opportunities to stop that access before the customer can obtain payment services, banking products, market access, or broader financial infrastructure. If KYC is weak, the institution may onboard a relationship on a false premise and only discover the real risk after suspicious activity has already begun. This is an inference supported by FATF’s emphasis on preventive measures and beneficial ownership transparency.

Watch on YouTube: Know Your Customer (KYC)

KYC is also inseparable from the risk-based approach. FATF says countries, competent authorities, and banks should identify, assess, and understand their money laundering and terrorist financing risks and apply mitigation measures proportionate to those risks. That means KYC should not be identical for every customer. Lower-risk relationships may justify simpler measures in limited cases, while higher-risk customers, structures, products, or jurisdictions may require more information, enhanced due diligence, stronger challenge, and more frequent review.

In practical terms, a robust KYC process usually answers a series of core questions. Who is the customer? If the customer is a legal entity, who ultimately owns or controls it? Why is the relationship being opened? What products or services will be used? What volume and pattern of activity should the firm expect? Which jurisdictions, counterparties, or payment corridors are likely to be involved? Do the customer’s explanations make commercial and behavioral sense? The FCA’s guidance makes clear that firms should gather enough information to provide a meaningful basis for subsequent monitoring.

KYC is therefore not just an onboarding requirement; it is the baseline for ongoing monitoring. If a firm understands the customer properly at the outset, it is far better placed to spot when the customer’s behavior changes in ways that may indicate fraud, sanctions exposure, mule activity, suspicious fund movement, or other financial crime. FCA guidance published in late 2024 explicitly says effective CDD and KYC assessments are relevant to wider financial crime controls, and notes their importance for sanctions compliance in particular.

The U.S. framework expresses similar ideas through the CDD Rule. FinCEN says the rule strengthens customer due diligence requirements for covered U.S. financial institutions and is intended to improve financial transparency and prevent criminals and terrorists from misusing companies to disguise illicit activity. FinCEN guidance also makes clear that customer due diligence is designed to help institutions understand the customer relationship and support ongoing monitoring, rather than requiring a fixed checklist of the same information in all cases.

That flexibility is important professionally because KYC should be meaningful rather than mechanical. A firm that only collects standard documents without understanding the customer may appear compliant while still missing material risk. By contrast, a strong KYC process combines document verification with contextual understanding and challenge. It asks whether the customer profile, ownership structure, expected activity, and stated purpose of the relationship make sense together. That is often where higher-risk or deceptive relationships become visible. This is an inference from the cited FCA and FinCEN materials on relationship understanding and subsequent monitoring.

Ultimately, KYC is one of the most important control disciplines in the financial crime environment because it establishes whether a firm truly understands who its customer is and what risk that customer brings. It is not just a front-end administrative task. It is the foundation on which sanctions screening, transaction monitoring, fraud controls, suspicious activity escalation, and broader financial crime governance depend. Without effective KYC, the rest of the framework operates on incomplete or unreliable assumptions.