The integration phase is the final stage of the classic money laundering cycle. UNODC describes money laundering as typically following three stages—placement, layering, and integration—and defines integration as the stage at which the money is made available to the criminal from what appear to be legitimate sources. FATF guidance and related materials also refer to all three stages when assessing money laundering threats and vulnerabilities.

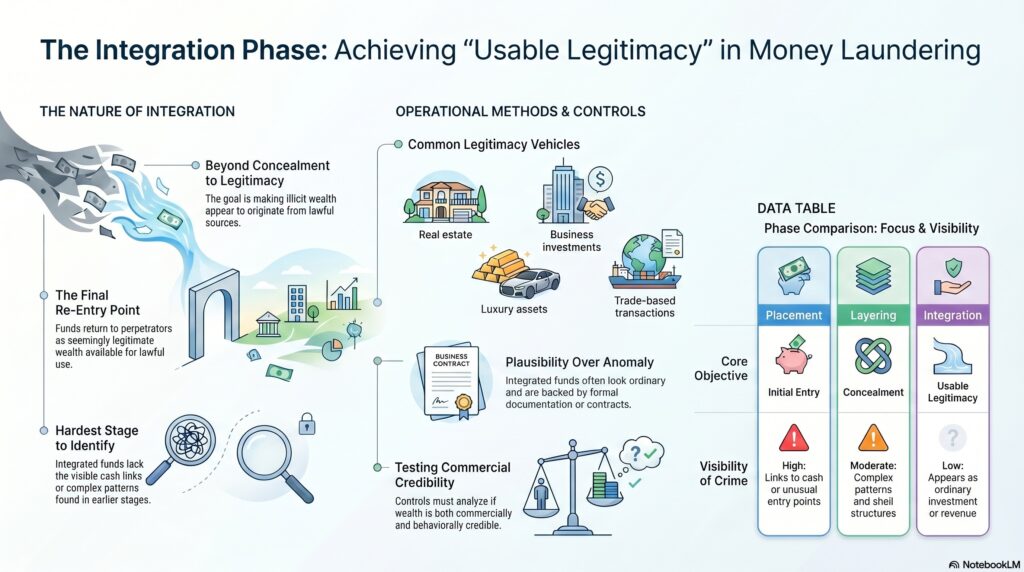

In the financial crime environment, the significance of the integration phase is that this is the point where criminal proceeds re-enter the legitimate economy with a reduced appearance of criminal origin. The funds have already been distanced from the predicate offence through placement and layering. By the time they reach integration, the objective is no longer simply concealment; it is usable legitimacy. UNODC’s educational materials describe integration as the stage in which the money returns to the perpetrators from what seems to be a legitimate source and can then be used for apparently lawful purposes.

From a professional AML perspective, integration matters because it is often the stage at which illicit wealth becomes hardest to distinguish from ordinary commercial or investment capital. At placement, there may still be visible links to cash, crime, or unusual entry into the financial system. At layering, there may still be complex transaction patterns, shell structures, or rapid fund movement that create suspicion. By contrast, integration is designed to produce credibility: investment returns, business revenue, asset sales, loan repayments, consulting fees, property proceeds, dividends, or other apparently legitimate explanations for wealth and liquidity. This is an inference supported by UNODC’s explanation that integrated funds reappear as if they came from legitimate sources.

Watch on YouTube: Integration Phase (of AML)

This is why the integration phase is especially important in risk assessment and investigations. A firm may encounter the proceeds not when they are first entering the system, but later, once they are already embedded in business, property, securities, luxury assets, trade flows, or corporate structures. FATF’s national risk assessment toolkit explicitly says countries should consider threats at all three stages of money laundering, including integration. In practical terms, that means an AML framework should not focus only on cash placement or complex layering patterns; it should also consider how illicit funds may present as apparently legitimate wealth or investment activity.

A professionally mature understanding of integration also recognizes that it is not always cleanly separated from layering. In practice, laundering often moves through blended cycles rather than neat sequential steps. FATF’s typology materials note that professional money launderers may be involved in one, or all, stages of the laundering cycle, including integration. That means firms should avoid treating integration as a purely theoretical end-state and instead view it as part of an adaptive process in which criminals seek progressively stronger legitimacy for their assets.

In operational terms, integration may involve the purchase or sale of real estate, business investment, loans between related parties, use of companies that generate apparently lawful revenue, securities transactions, trade-based transactions, or luxury-asset acquisition and disposal. FATF sectoral typology work has noted that some sectors are used particularly in the layering and integration stages, which reinforces the point that certain products or markets may be attractive precisely because they help convert concealed proceeds into apparently ordinary value.

The control challenge at the integration stage is therefore one of plausibility rather than obvious anomaly. By this point, the funds may no longer look unusual in isolation. They may be accompanied by documentation, contractual explanations, or transactional histories that make them appear legitimate. That is why effective AML controls need strong customer due diligence, source-of-funds and source-of-wealth assessment, beneficial ownership analysis, and ongoing monitoring capable of testing whether the apparent legitimacy of funds is commercially and behaviourally credible. This is an inference from the nature of integration as funds returning from what seem to be legitimate sources.

Ultimately, the integration phase matters in the financial crime environment because it is the point at which laundering succeeds most fully: illicit proceeds become usable within the formal economy with reduced suspicion and greater apparent legitimacy. For firms and authorities, that makes integration one of the hardest stages to identify and one of the most important to understand when assessing how criminal wealth is preserved, invested, and enjoyed over time.