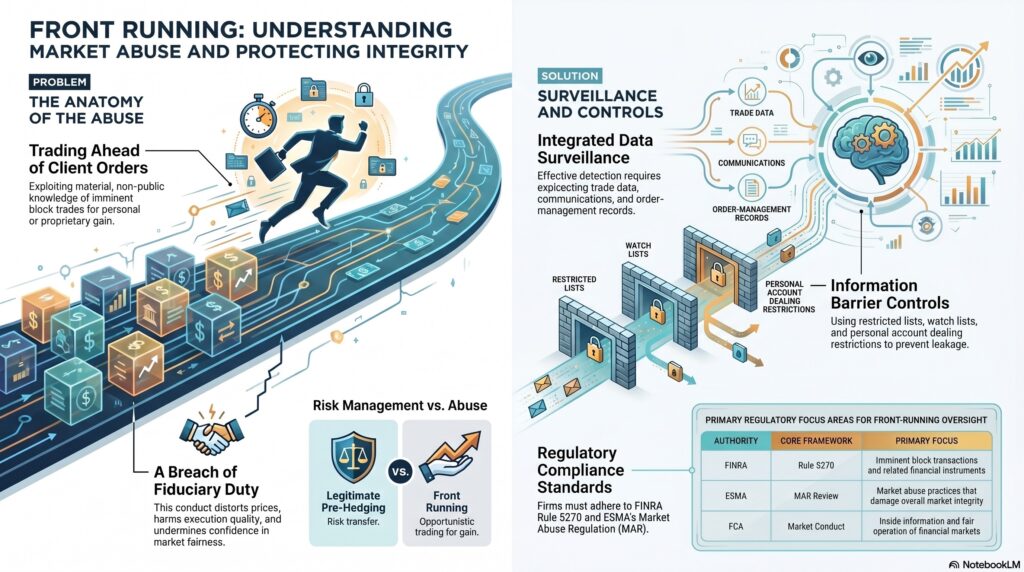

Front running is a form of market abuse in which a person trades ahead of a client order or other imminent transaction using material, non-public information about that pending activity. FINRA Rule 5270 prohibits a member or associated person from trading a security or related financial instrument while in possession of material, non-public market information concerning an imminent block transaction before that information is public or stale. ESMA has also described front running as a market abuse practice in its MAR review work.

In the financial crime environment, front running is significant because it is fundamentally an abuse of informational advantage and fiduciary position. The person engaging in it is not merely making a lucky trade; they are exploiting confidential order knowledge to profit ahead of the client or market. That makes front running both a conduct failure and a market-integrity failure. It can distort prices, harm execution quality, disadvantage clients, and undermine confidence in the fairness of financial markets. ESMA’s market abuse framework is aimed at preventing abusive practices that damage market integrity, and FINRA treats front running as part of manipulative trading risk.

From a professional compliance perspective, front running usually arises where someone has advance knowledge of a pending order, block trade, or quote-related activity and uses that knowledge to trade first. The classic example is a broker or trader who knows a large client order is about to move the market and trades for a proprietary, personal, or affiliated account ahead of it. FINRA’s rule is specifically focused on imminent block transactions and extends to related financial instruments, showing that the misconduct is not limited to the exact instrument in the customer order.

Watch on YouTube: Front Running

This is why front running is closely connected to information-barrier controls, control-room functions, personal account dealing restrictions, and surveillance over trading and communications. If confidential order information can move too freely across a firm, or if staff can trade without effective restriction and review, the risk of front running rises materially. The FCA’s Market Conduct sourcebook and ESMA’s broader MAR materials both sit within a framework concerned with inside information, abusive conduct, and fair market operation.

A key practical distinction is between legitimate risk management and abusive pre-positioning. ESMA’s work on pre-hedging acknowledges that some trading ahead of a client transaction may occur for risk-management reasons in specific contexts, but it also states that where such activity lacks a genuine risk-management rationale it could amount to market abuse, including front running. That distinction matters because not all pre-trade activity is automatically improper; the issue is whether the conduct is genuinely connected to lawful execution or risk transfer, or whether it is opportunistic trading that exploits confidential information for gain.

In operational terms, front running is difficult to detect unless firms can connect several data sources. Trade surveillance alone may identify unusual proprietary or employee trading before a client block order. Communications surveillance may reveal awareness of the pending order or improper coordination. Order-management and control-room records may show who had access to the information and when restrictions should have applied. This is why front-running controls usually depend on integrated surveillance across orders, executions, positions, restricted lists, and communications rather than on a single alert type. This is an inference supported by FINRA’s focus on block-transaction information and ESMA’s treatment of front running as market abuse.

For firms, the control response should include strong information barriers, restricted and watch lists, personal account dealing controls, front-office supervision, surveillance of proprietary and employee trading, and clear escalation where client-order information may have been misused. In U.S. broker-dealer environments, FINRA Rule 5270 is a core rule reference, and FINRA’s manipulative trading guidance continues to identify it as a live obligation.

Ultimately, front running matters in the financial crime environment because it converts confidential market information into unfair trading advantage. It harms clients directly, distorts price formation, and weakens trust in the integrity of execution and markets. For that reason, it should be treated as a serious market abuse risk requiring strong information controls, surveillance, and governance.