Fiat money is money issued by a state or central authority that is not convertible into, or backed by, a commodity such as gold or silver, and whose value depends on legal status, public confidence, and continued acceptance in payment. Federal Reserve materials describe fiat money as inconvertible and not backed by any commodity, while IMF materials refer to government-issued currencies as fiat money and note their role as a unit of account, medium of exchange, and store of value.

In the financial crime environment, fiat money matters because it is the baseline monetary system through which most regulated financial activity is conducted. Salaries, deposits, loans, card payments, domestic transfers, correspondent banking flows, and most reported suspicious activity ultimately settle in fiat currency or claims linked to it. That means AML, fraud, sanctions, and market-conduct controls are largely designed around the movement, storage, and misuse of fiat money within the banking and payments system. This is an inference based on the Federal Reserve’s description of fiat money as legal tender and the IMF’s description of fiat currency as the standard government-issued form of money.

Watch on YouTube: Fiat Money

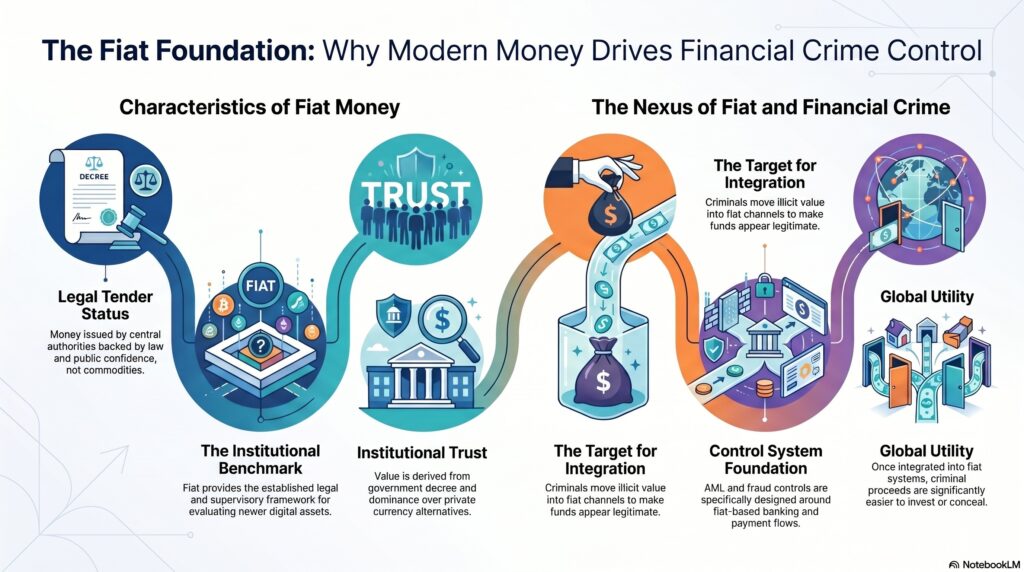

A key professional point is that fiat money derives its force from legal tender status and institutional trust, not from intrinsic value. Federal Reserve materials explain that fiat money serves as legal tender by government decree, and IMF sources note that government-issued fiat money displaced competing private currencies as central banks became dominant issuers. In practical terms, this legal and institutional foundation is what allows financial crime controls to be built around identifiable currencies, central-bank frameworks, regulated payment systems, and state-backed monetary authority.

This matters in the financial crime environment because criminal misuse of money usually involves trying to make illicit value appear legitimate within a fiat-based financial system. Money laundering, fraud proceeds placement, sanctions evasion, mule activity, and suspicious transfers generally aim to move criminal value into or through fiat-money channels that are widely accepted and legally recognized. The attraction is obvious: once funds are integrated into ordinary fiat payment and banking flows, they are easier to spend, transfer, invest, or conceal. This is an inference supported by the role of fiat money as the dominant means of payment and store of value in modern economies.

Fiat money is also important as the benchmark against which newer forms of digital value are assessed. Federal Reserve materials note that stablecoins do not have legal tender status in the way central bank fiat currencies do, and IMF materials describe CBDCs as a digital form of fiat money issued by a central bank. In compliance terms, that distinction matters because fiat money sits inside an established legal, prudential, and supervisory framework, while newer digital instruments may sit outside it, alongside it, or be linked back to it.

Ultimately, fiat money is central to the financial crime environment because it is the legally recognized monetary foundation of the regulated financial system. Financial crime controls are designed largely to protect the integrity of fiat-based payments, deposits, transfers, and settlement arrangements from misuse by criminals, sanctioned parties, fraudsters, and other bad actors. For that reason, fiat money is not just an economic concept; it is the monetary context within which most modern financial crime risk is created, monitored, and controlled.