FedNow is the Federal Reserve’s instant payment service for U.S. depository institutions. The Federal Reserve says the FedNow Service enables individuals and businesses to send and receive payments within seconds, 24x7x365, with recipients able to use the funds immediately. It is designed as instant payment infrastructure for eligible financial institutions and uses ISO 20022 messaging.

In the financial crime environment, FedNow is significant because it changes the timing and control profile of domestic payments. Traditional payment rails often provide more time for review, exception handling, or post-initiation intervention. FedNow compresses that window dramatically. The speed and always-on availability that make instant payments attractive for payroll, bill settlement, emergency disbursements, and account-to-account transfers also make them more sensitive to fraud, mule activity, account compromise, and scam execution. The Federal Reserve’s own fraud education materials for instant payments emphasize that instant payments create distinct fraud challenges because of their speed and immediacy.

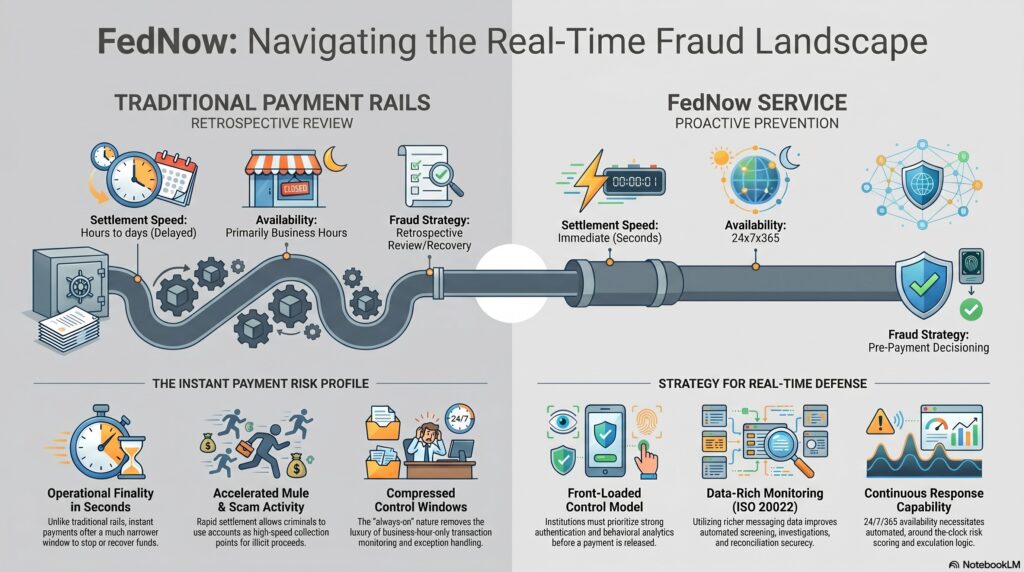

From a professional financial crime perspective, the most important feature of FedNow is not simply that it is fast, but that it is real-time and operationally final in practice. Once an instant payment is successfully executed and funds are made available, the institution’s opportunity to stop loss or recover funds is far narrower than in slower payment environments. That makes fraud prevention and pre-payment decisioning much more important. A weak fraud-control model that might be tolerable in a delayed-settlement environment becomes materially riskier in an instant-payments environment. This is an inference supported by the Federal Reserve’s description of FedNow as an instant service with immediate fund availability and its separate emphasis on fraud controls for instant payments.

Watch on YouTube: FedNow

FedNow is therefore especially relevant to authorized push payment-style scams, account takeover, social engineering, and mule-account risk. If a customer is deceived into sending a payment, or if a criminal gains control of a legitimate account, the payment can move in seconds and become available to the recipient immediately. In practical terms, that means the receiving account can function as a rapid collection point for fraud proceeds. Financial institutions using FedNow need strong controls not only for outbound payment initiation, but also for inbound receiving-account monitoring, because fast receipt of funds can signal mule or scam-related behavior just as much as fast origination can signal victimization. This is an inference from the service’s instant-payment characteristics and the Federal Reserve’s fraud guidance.

A mature financial crime framework for FedNow depends on front-loaded controls. These typically include strong authentication, account and device security, payee-risk analysis, behavioral analytics, transaction-risk scoring, sanctions and screening checks where relevant, and escalation logic that can act before payment release. Because the service operates around the clock, firms also need continuous monitoring and response capability rather than controls designed mainly for business-hour payment operations. The Federal Reserve’s materials note optional FedNow features including fraud prevention tools, request for payment functionality, and liquidity management support, which indicates that participants are expected to think carefully about operating controls rather than treating FedNow as a simple faster version of legacy payments.

FedNow also has implications for AML and suspicious activity monitoring. The payment itself may be domestic and legitimate, but instant settlement can accelerate the movement and layering of funds once illicit proceeds enter the system. This means firms need monitoring that is sensitive to rapid pass-through behavior, unusual beneficiary creation, sudden changes in account use, concentration of inbound payments, and activity inconsistent with customer profile. In other words, instant payments increase the importance of contextual and behavioral monitoring because there is less time to rely on retrospective review. This is an inference supported by the Federal Reserve’s instant-payment design and fraud-risk materials.

Another important feature is interoperability of data and messaging. FedNow uses ISO 20022, which supports richer data structures and can improve automated processing and information exchange. In the financial crime environment, richer payment data can strengthen screening, investigations, reconciliation, and downstream monitoring, provided firms actually use that data well. Better message content can improve detection quality, but it does not remove the need for strong governance, calibration, and operational capability.

Ultimately, FedNow is important in the financial crime environment because it brings instant-payment speed and continuous availability into mainstream U.S. domestic payments. That creates clear benefits for customers and institutions, but it also raises the stakes for fraud prevention, scam detection, mule-account monitoring, and real-time risk management. In a FedNow environment, institutions cannot depend heavily on delayed review or recovery after the fact. They need controls capable of making sound decisions before or during payment execution, when the opportunity to prevent harm still exists.