The European Securities and Markets Authority (ESMA) is the EU’s financial markets regulator and supervisor. ESMA describes itself this way on its current website and states that its strategic priorities include strengthening supervision, enhancing retail investor protection, fostering effective markets and financial stability, enabling sustainable finance, and facilitating technological innovation and effective use of data.

In the financial crime environment, ESMA is significant because it sits at the center of the EU’s market integrity and securities supervision framework. Its role is not identical to that of a bank-centric AML supervisor, but it is highly relevant wherever financial crime intersects with securities markets, trading venues, investment firms, post-trade infrastructure, and investor protection. ESMA’s market integrity materials state that its work under the Market Abuse Regulation includes technical advice, guidelines, regulatory technical standards, opinions, and Q&As for preventing, detecting, and reporting abusive practices.

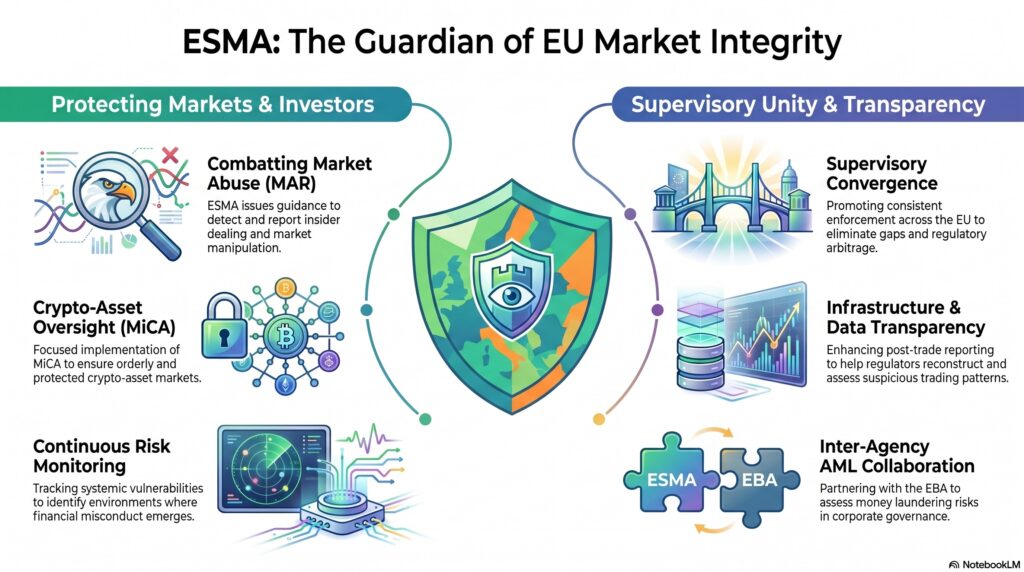

From a professional compliance perspective, ESMA is best understood as a markets-focused authority whose financial-crime relevance comes mainly through market abuse prevention, supervisory convergence, transparency, and infrastructure oversight. It is especially important in areas such as insider dealing, unlawful disclosure of inside information, market manipulation, suspicious transaction and order reporting, transparency regimes, post-trade reporting, CCP and trade repository oversight, and more recently crypto-asset market supervision under MiCA. ESMA’s 2026 work programme expressly says it will continue to focus on effective implementation of MiCA and on supervision of crypto-asset service providers to support investor protection and orderly crypto-asset markets.

A core reason ESMA matters in the financial crime environment is market abuse. Market abuse is a form of financial misconduct that can overlap with insider misuse of information, coordinated manipulation, misleading market signals, and abusive trading behavior. ESMA’s market integrity pages make clear that it plays a central role in the MAR framework by issuing technical advice, guidance, and standards that help national competent authorities and market participants apply the regime consistently. In practical terms, this means ESMA helps shape the rules and expectations around how firms prevent and detect misconduct in securities markets.

Watch on YouTube: European Securities And Markets Authority

That role is especially important because ESMA is also a supervisory convergence authority. It does not replace national competent authorities across the EU, but it works to make supervision more consistent across Member States. In the financial crime environment, this matters because fragmented supervision can create uneven standards, inconsistent enforcement, and opportunities for regulatory arbitrage. ESMA’s 2026 work programme says it enhances market integrity by promoting supervisory convergence under MAR and the Short Selling Regulation and by monitoring new threats to market integrity.

ESMA is also important because of its role in market infrastructure and transparency. Its activities include oversight or rulemaking involvement in areas such as EMIR, consolidated tapes, data reporting, central counterparties, and broader post-trade transparency. These functions are not AML controls in the narrow sense, but they strengthen the transparency and resilience of the markets in which misconduct can occur. Better reporting, stronger post-trade data, and more consistent infrastructure oversight improve the ability of regulators and firms to identify suspicious patterns, reconstruct events, and assess whether trading behavior was legitimate. This is an inference supported by ESMA’s activities pages and work programme priorities around effective markets, financial stability, and data use.

There is also a broader risk-monitoring dimension. In March 2026, ESMA published its first risk monitoring report of 2026 and said that risks of market and systemic stress remained high despite resilient market performance. This shows ESMA’s role is not limited to technical rulemaking; it also monitors systemic vulnerabilities and market conditions that can shape the environment in which fraud, manipulation, and wider financial misconduct emerge.

Although ESMA is not the main EU AML authority, it still has relevance to AML-adjacent issues through joint work with the other European Supervisory Authorities. For example, in February 2026 ESMA and the EBA published draft joint guidelines that included assessment of whether there are reasonable grounds to assume increased money laundering risk in fitness and propriety contexts. That illustrates how ESMA’s securities and governance work can intersect with money laundering concerns even when AML is not its primary standalone mandate.

A professionally mature view therefore places ESMA within the broader financial crime ecosystem as a market integrity, transparency, and supervision authority. It is less about retail account onboarding or classic bank AML controls, and more about the integrity of securities markets, the quality and consistency of supervision, the resilience of market infrastructure, and the prevention of abusive conduct. Where financial crime takes the form of insider dealing, manipulation, reporting failures, or misconduct in securities and derivatives environments, ESMA is a key institutional actor. This is an inference supported by ESMA’s own description of its activities and strategic priorities.

Ultimately, the European Securities and Markets Authority matters in the financial crime environment because it helps protect EU financial markets from misconduct that undermines investor confidence, market fairness, and supervisory visibility. Through market abuse oversight, supervisory convergence, infrastructure regulation, risk monitoring, and emerging work in areas such as MiCA, ESMA forms a core part of the EU framework for maintaining clean, transparent, and resilient capital markets.