The European Market Infrastructure Regulation (EMIR) is the EU framework that lays down rules for over-the-counter derivatives, central counterparties (CCPs), and trade repositories. The European Commission describes EMIR in exactly those terms, and the core regulation remains Regulation (EU) No 648/2012.

In the financial crime environment, EMIR is important because it strengthens the post-trade transparency, risk management, and resilience of derivatives markets. Its primary purpose is not AML in the narrow sense, but it is highly relevant to the wider financial crime framework because opaque derivatives activity, weak collateralisation, poor reporting, and fragmented post-trade infrastructure can make manipulation, concealment of exposures, and other misconduct harder to detect and supervise. The European Commission’s overview presents EMIR as the main EU rulebook for OTC derivatives, CCPs, and trade repositories, while ESMA treats it as a core market-infrastructure and reporting framework.

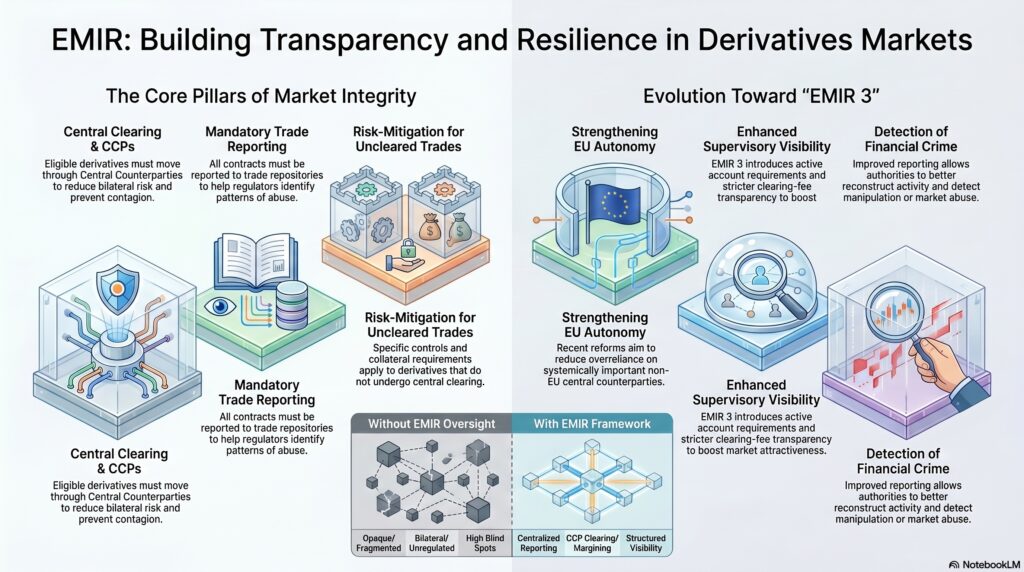

From a professional compliance perspective, EMIR should be understood as a market infrastructure and transparency regime. It introduced obligations around clearing certain OTC derivatives through CCPs, reporting derivatives contracts to trade repositories, and applying risk-mitigation techniques to uncleared OTC derivatives. Those elements matter in the financial crime environment because they reduce opacity, improve supervisory visibility, and create more structured control over derivatives exposures that could otherwise remain difficult to monitor.

Watch on YouTube: European Market Infrastructure Regulation

A key part of EMIR’s significance is the trade reporting framework. By requiring derivatives contracts to be reported to trade repositories, EMIR helps regulators and supervisors reconstruct activity, monitor exposures, and identify patterns that may point to wider market misconduct or control weakness. In practical terms, better derivatives reporting improves the evidential environment in which market abuse, manipulation, false reporting, and other serious conduct issues can be assessed. This is an inference from the Commission’s description of EMIR as the rulebook for OTC derivatives and trade repositories, combined with ESMA’s role in EMIR implementation and supervision.

EMIR is also important because of its emphasis on central clearing and CCP resilience. Central clearing reduces bilateral counterparty risk by moving eligible derivative contracts into a framework where a CCP stands between the parties and applies margining, default management, and risk controls. In the wider financial crime environment, this matters because stronger clearing infrastructure supports market stability and reduces the kind of opacity and contagion risk that can amplify misconduct or disorder in stressed markets. The Commission’s post-trade services overview and the Council’s 2024 adoption of revamped EMIR rules both emphasize resilience and the attractiveness of EU clearing markets.

Recent reforms are also important. The Council adopted revised EMIR rules in November 2024, and the Commission has described EMIR 3 as a framework intended to improve the attractiveness and resilience of EU clearing markets and reduce the EU’s overreliance on systemically important UK CCPs. ESMA materials from 2025 and 2026 also refer repeatedly to EMIR 3, including work on clearing thresholds, the active account requirement, post-trade risk reduction services, and clearing-fee transparency.

That current reform agenda matters in the financial crime environment because it shows EMIR is not a static historical regime. It is an evolving supervisory framework for the infrastructure through which large volumes of derivatives risk are processed, reported, and managed. Better reporting, more resilient clearing arrangements, and stronger supervisory standards improve the ability of authorities and firms to detect unusual patterns, understand interconnected exposures, and maintain market integrity. This is an inference from the Commission’s and ESMA’s current EMIR 3 workstreams.

A professionally mature view therefore places EMIR alongside other market-conduct and market-infrastructure controls rather than treating it as a pure financial crime statute. It does not replace AML, sanctions, or fraud obligations, but it strengthens the transparency and control environment in which those wider risks may surface in derivatives markets. Where reporting is weak, clearing arrangements are fragile, or post-trade visibility is poor, misconduct and supervisory blind spots become more likely. Where EMIR works well, the market infrastructure becomes easier to oversee and harder to exploit through opacity or weak post-trade controls. This is an inference supported by the official purpose of EMIR and the emphasis on transparency, resilience, and supervision in the cited sources.

Ultimately, the European Market Infrastructure Regulation is significant in the financial crime environment because it helps make derivatives markets more transparent, more resilient, and more governable. It creates the framework for clearing, reporting, and risk mitigation that supports supervisory visibility and market integrity across OTC derivatives and related post-trade infrastructure. For that reason, EMIR should be understood as a core component of the wider European control environment for market misconduct, systemic risk, and post-trade transparency.