Dual-use goods are goods, software, or technology that can be used for both legitimate civilian purposes and military, weapons-related, or other security-sensitive purposes. The European Commission defines dual-use items as goods, software, and technology that can be used for both civilian and military applications, while the U.S. Bureau of Industry and Security describes dual-use items as having civil applications as well as terrorism-, military-, or weapons-of-mass-destruction-related applications.

In the financial crime environment, dual-use goods are important because they sit at the intersection of export controls, sanctions, proliferation finance, trade-based money laundering risk, and broader national-security concerns. A transaction involving dual-use goods may be perfectly lawful, but it may also create elevated risk if the end-user, end-use, destination, intermediary chain, or financing structure is opaque, deceptive, or linked to sanctions evasion or proliferation activity. The EU’s dual-use regime expressly states that controls are intended to contribute to international peace and security and prevent the proliferation of weapons of mass destruction.

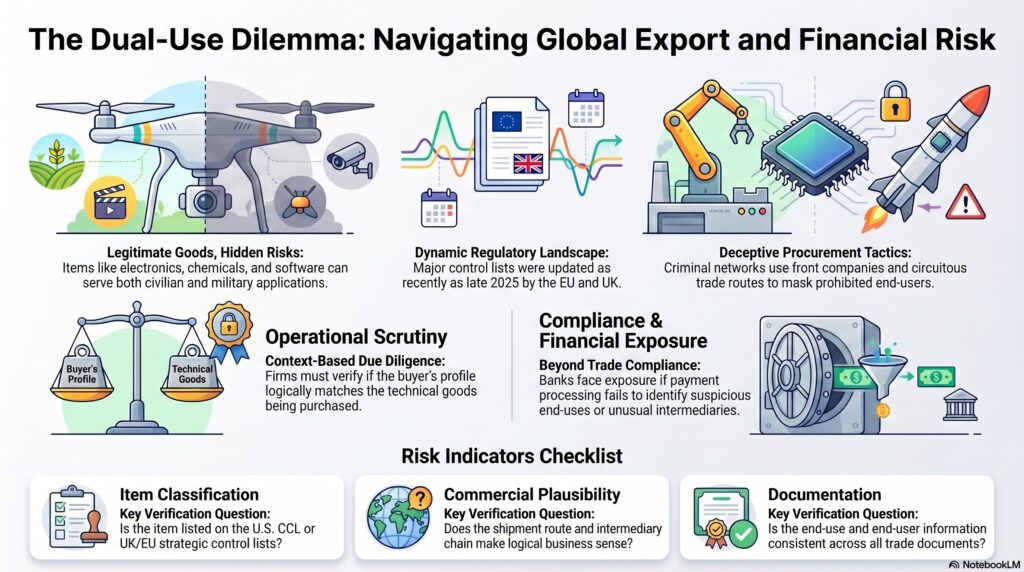

From a professional compliance perspective, the significance of dual-use goods is not that the goods are inherently prohibited. The significance is that they require closer scrutiny because the same item may support ordinary commercial activity in one context and military or proliferation-related activity in another. That makes context critical. A firm needs to understand not only what the item is, but also who is buying it, where it is going, how it will be used, whether intermediaries are involved, and whether the trade pattern makes commercial sense. This is an inference supported by the UK, EU, and U.S. export-control frameworks, all of which treat dual-use items as subject to licensing or control depending on item classification, destination, and end-use.

Watch on YouTube: Dual-Use Goods

This is why dual-use goods are especially relevant in sanctions and proliferation-finance risk management. Criminal networks, sanctioned actors, and procurement agents may attempt to acquire dual-use goods through front companies, intermediaries, misdeclared shipments, or circuitous trade routes in order to conceal the true end-user or end-use. The regulatory frameworks in the EU, UK, and U.S. are designed to address exactly that concern through controls on export, re-export, brokering, transit, technical assistance, and technology transfer.

In operational terms, dual-use risk often arises through trade and payment activity that appears commercially ordinary on the surface. A payment for electronics, machine tools, chemicals, software, components, or technical data may seem routine, yet those items may fall within a controlled category if their technical characteristics make them suitable for sensitive military or proliferation-related use. The UK’s strategic export controls guidance explains that dual-use controls cover not only goods, but also software and technology, and that the UK maintains a consolidated list of strategic military and dual-use items requiring export authorisation.

For financial institutions, this means dual-use goods are rarely just a trade-compliance issue for exporters. They can also become a banking and payments issue. Banks financing, processing, or supporting trade involving controlled goods may face exposure if customer due diligence, sanctions controls, trade-finance review, or escalation procedures are not strong enough to identify suspicious end-use, unusual intermediaries, high-risk destinations, or inconsistencies in trade documentation. This is an inference drawn from the structure of the export-control regimes and their focus on goods, brokering, transit, technical assistance, and end-use controls.

A mature control framework therefore treats dual-use goods as a risk indicator requiring enhanced review where relevant. Important questions include whether the item is on a control list, whether the destination is high risk, whether the customer’s business profile matches the goods being purchased, whether the shipment route is commercially plausible, whether intermediaries are necessary and credible, and whether the documentation around end-use and end-user is consistent. The U.S. BIS points firms to the Export Administration Regulations and the Commerce Control List for classification of controlled dual-use items, while the UK and EU maintain corresponding control lists and licensing frameworks.

Another important feature is that dual-use controls are dynamic rather than static. The EU updated its control list again in September 2025, and the UK published an updated strategic export control list in December 2025. That means firms involved in export compliance, trade finance, sanctions screening, or higher-risk cross-border payments cannot rely on outdated classifications or assumptions.

Ultimately, dual-use goods matter in the financial crime environment because they combine legitimate commercial utility with heightened misuse potential. They can be part of lawful industrial trade, but they can also feature in sanctions evasion, proliferation procurement, deceptive trade structures, and other forms of illicit activity. For that reason, dual-use goods should be understood as a high-context risk area where product knowledge, customer understanding, end-use analysis, and export-control awareness all need to come together.