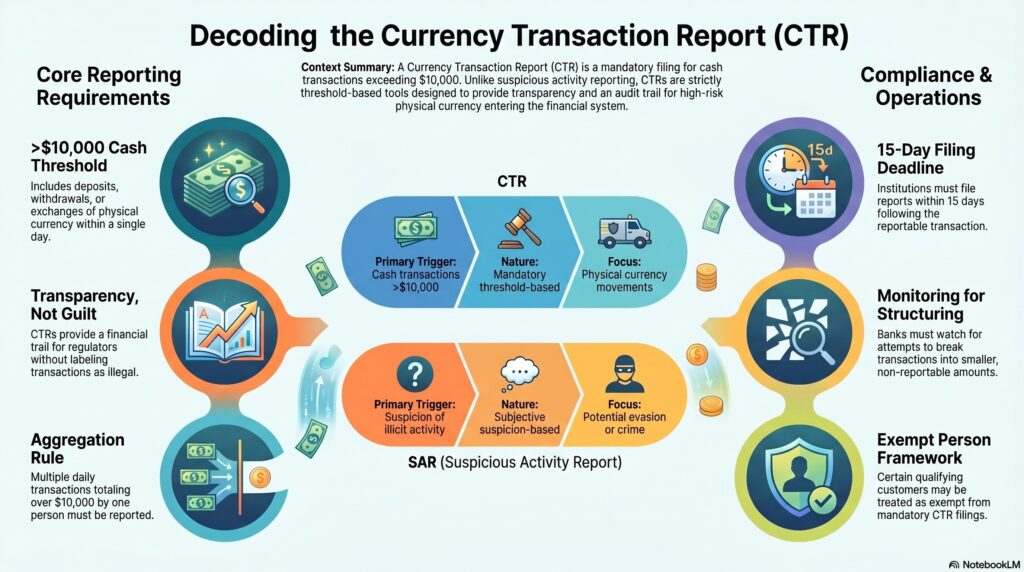

A Currency Transaction Report (CTR) is a U.S. Bank Secrecy Act reporting requirement used to document certain cash transactions conducted through financial institutions. Under 31 CFR 1010.311, a financial institution other than a casino must file a report for each deposit, withdrawal, exchange of currency, or other payment or transfer involving more than $10,000 in currency by, through, or to the institution, unless an exemption applies. FinCEN’s customer guidance also states that multiple currency transactions that aggregate to more than $10,000 in a single day by or on behalf of one person are reportable.

In the financial crime environment, the CTR is significant because it creates a formal record of large cash activity entering or moving through the financial system. It is not a suspicious activity report, and the existence of a CTR does not mean the transaction is illegal. FinCEN expressly notes that large currency transactions are not illegal and that the CTR requirement is part of the BSA framework that helps create a financial trail for investigators and regulators. That makes the CTR a transparency and intelligence tool rather than a finding of wrongdoing.

From a professional AML perspective, CTRs matter because cash remains inherently high-risk from a money laundering standpoint. Unlike many electronic payment methods, cash does not carry the same built-in audit trail about payer, purpose, or originating account history. Once large amounts of cash are deposited into the banking system, however, they begin to look more like ordinary funds unless the activity is properly recorded, reviewed, and understood. CTR reporting helps preserve visibility at that point of entry. This is one reason the BSA treats large cash transactions differently from many non-cash transfers.

A key professional distinction is that a CTR is threshold-based, while a SAR is suspicion-based. A financial institution files a CTR because the transaction meets the reporting threshold for currency, not because the institution necessarily suspects criminality. By contrast, suspicious activity reporting is required where the institution knows, suspects, or has reason to suspect that a transaction involves illicit activity or attempts to evade BSA requirements. FinCEN’s later SAR FAQ materials specifically note that structuring transactions to evade CTR filing can trigger SAR obligations.

Watch on YouTube: Currency Transaction Report (CTR)

This distinction is operationally important because some of the most significant financial crime issues connected to CTRs arise not from the reportable cash transaction itself, but from attempts to avoid CTR reporting. The BSA regulations include provisions on aggregation and structured transactions, and the FFIEC manual separately notes that structuring transactions to evade BSA reporting can lead to civil and criminal penalties. In practice, this means institutions should not view CTR filing as the end of the control process. They must also monitor for attempts to break transactions into smaller amounts or otherwise avoid reporting.

CTRs are especially relevant in sectors and customer profiles where cash activity is expected but still requires explanation, such as cash-intensive businesses, certain retail operations, gaming-related activity, or customers whose stated business model plausibly generates physical currency. In these cases, the reporting obligation itself may be routine, but the institution still needs to understand whether the level, pattern, and frequency of cash activity are consistent with the customer profile. A CTR does not replace customer due diligence, ongoing monitoring, or suspicious activity review. It complements them by ensuring large cash movements are formally documented. This is an inference supported by the CTR filing rules and the FFIEC focus on policies, procedures, and processes for preparing, filing, and retaining CTRs.

There is also a strong operational-control dimension. The FFIEC BSA/AML Manual states that examiners assess whether a bank’s policies, procedures, and processes adequately address the preparation, filing, and retention of CTRs, and whether management has addressed errors reported through FinCEN’s BSA E-Filing System. This means CTR compliance is not just about knowing the threshold. It also depends on data quality, aggregation logic, exception handling, timely filing, retention, and governance over the end-to-end reporting process.

Timing is another important point. The eCFR states that a report required by §1010.311 must be filed within 15 daysfollowing the reportable transaction. In practice, this makes CTR compliance a live operational requirement, not a retrospective annual exercise. Institutions need systems capable of identifying reportable currency transactions promptly, aggregating them correctly, and routing them into the filing process without delay.

There are also exemptions. The CTR obligation does not apply in the same way to all transactions and counterparties, and banks may treat certain qualifying customers as exempt persons under the BSA rules. The eCFR provisions for banks state that no bank is required to file a report otherwise required by §1010.311 with respect to a transaction in currency between an exempt person and the bank, subject to the limits and conditions of the exemption framework. This is important because a mature CTR control framework must distinguish between mandatory filings, available exemptions, and suspicious attempts to misuse the exemption concept.

Ultimately, the CTR is a foundational BSA reporting tool because it ensures that large cash transactions are captured in a structured, reportable form that supports transparency, regulatory oversight, and law-enforcement visibility. In the financial crime environment, its importance lies not in suggesting that cash is inherently criminal, but in recognizing that large cash movements can be a key point of vulnerability in the laundering cycle. For that reason, CTR reporting should be understood as a core part of the U.S. cash-transparency framework, closely linked to customer due diligence, structuring detection, suspicious activity escalation, and broader AML governance.