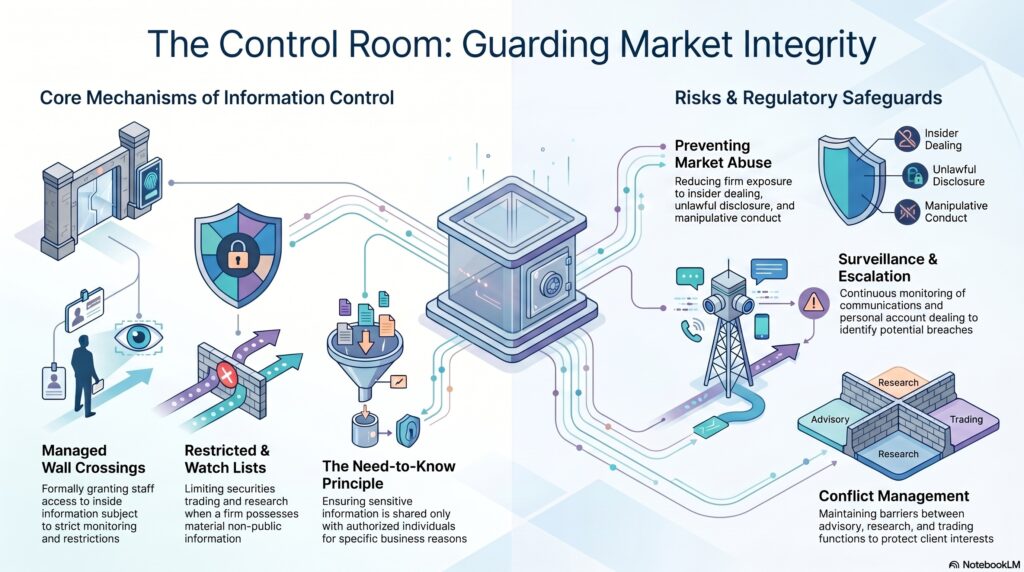

A control room is a compliance function, typically found in investment banks, broker-dealers, and other capital-markets firms, that manages the flow of confidential or inside information across the firm and helps maintain effective information barriers. In practice, the control room often oversees wall crossings, restricted and watch lists, employee dealing restrictions, information-barrier controls, and related surveillance or escalation processes designed to reduce the risk of insider dealing, unlawful disclosure, market abuse, and conflicts of interest. The FCA’s thematic work on flows of confidential and inside information focuses on exactly these risks, while SEC examination findings describe information-barrier surveillance as often sitting within a control group or similar compliance structure.

In the financial crime environment, the control room is significant because it sits at the point where commercially sensitive information and regulatory risk meet. Investment banking, advisory, research, sales, and trading functions may all handle information that is confidential, price-sensitive, or otherwise capable of being misused. The control room exists to help ensure that this information is shared only on a need-to-know basis, that wall crossings are controlled, and that trading or communications restrictions are applied where necessary. FCA speeches and market-abuse materials emphasize the importance of access controls, surveillance capabilities, and strong information-control arrangements across advisory and investment-banking platforms.

From a professional compliance perspective, the control room is not merely an administrative list-management team. It is a governance and market-integrity function. Its role is to make sure that the firm can conduct legitimate business involving sensitive information without allowing that information to leak into trading, research, personal account dealing, or other areas where misuse could occur. That means the control room is closely tied to conflicts of interest management, market abuse prevention, personal account dealing controls, and communications oversight. FCA Market Watch 83, published in September 2025, specifically highlighted the effectiveness of information barriers and noted that weak physical arrangements can heighten the risk of poor information control.

Watch on YouTube: Control Room

A central task of the control room is often the management of wall crossings. This is the process by which staff are formally brought “over the wall” and given access to confidential or inside information for a legitimate business reason, usually subject to restrictions and monitoring. Once this occurs, the firm may need to place securities on restricted or watch lists, limit dealing by relevant staff, and increase surveillance around associated activity. SEC examination findings on broker-dealer information barriers discuss over-the-wall processes and heightened surveillance as important controls to prevent misuse of material non-public information.

The control room also supports the practical application of the need-to-know principle. In a large markets business, not everyone who could technically access information should be permitted to do so. Control-room processes help determine who should receive information, under what conditions, and with what resulting restrictions. This is especially important where advisory, financing, underwriting, research, and trading activities sit within the same broader organization. The FCA’s thematic review on confidential and inside information directly addresses how firms define and manage such information, and recent FCA commentary continues to stress the importance of strong information barriers.

In the financial crime environment, this has direct relevance to market abuse. If inside information is shared too broadly, controlled poorly, or not linked to appropriate restrictions, the firm increases its exposure to insider dealing, unlawful disclosure, and manipulative conduct. A control room helps reduce that risk by coordinating restrictions, approvals, surveillance, and escalation. The Central Bank of Ireland’s overview of the Market Abuse Regulation emphasizes prohibitions on insider dealing, market manipulation, and unlawful disclosure of inside information, which are exactly the types of risks control-room structures are designed to help prevent.

A mature control-room framework usually depends on more than restricted lists alone. It also requires clear policies, documented wall-crossing processes, role-based access controls, employee training, personal account dealing controls, surveillance of communications and trading, and governance over when information can be shared or de-restricted. SEC examination material shows that firms may embed information-barrier surveillance either in a control group or a broader surveillance function, but in both cases the quality of review and escalation is critical.

Ultimately, the control room is important in the financial crime environment because it helps firms handle sensitive information without allowing that information to distort trading, compromise clients, or undermine market integrity. It is a core part of the information-barrier framework that supports conflict management, market-abuse prevention, and defensible governance in wholesale and capital-markets businesses. Where it is weak, firms risk poor information control, ineffective restrictions, and greater exposure to insider dealing and related misconduct.