Control effectiveness is the extent to which a firm’s controls actually prevent, detect, escalate, and remediate financial crime risk in practice. In the financial crime environment, it is not enough for a control to exist on paper or within a policy framework. A control is effective only if it operates as intended, is proportionate to the firm’s risk profile, and produces outcomes that meaningfully reduce exposure to fraud, money laundering, sanctions breaches, market abuse, or other forms of financial misconduct. The FCA’s Financial Crime Guide describes effective systems and controls as those that help firms detect, prevent, and deter financial crime, while the FCA’s 2024 policy update says its supervisory approach focuses on the effectiveness of firms’ systems and controls.

From a professional financial crime perspective, control effectiveness is about performance, not presence. A sanctions screening system may be installed, a transaction monitoring scenario may be configured, and a customer due diligence process may be documented, but those controls may still be ineffective if the data is poor, the calibration is weak, alerts are not investigated properly, or governance is too weak to identify and correct failures. The FFIEC BSA/AML Manual similarly frames internal controls in terms of whether they are designed to mitigate and manage money laundering, terrorist financing, and other illicit financial activity risks, and whether they support compliance with applicable requirements.

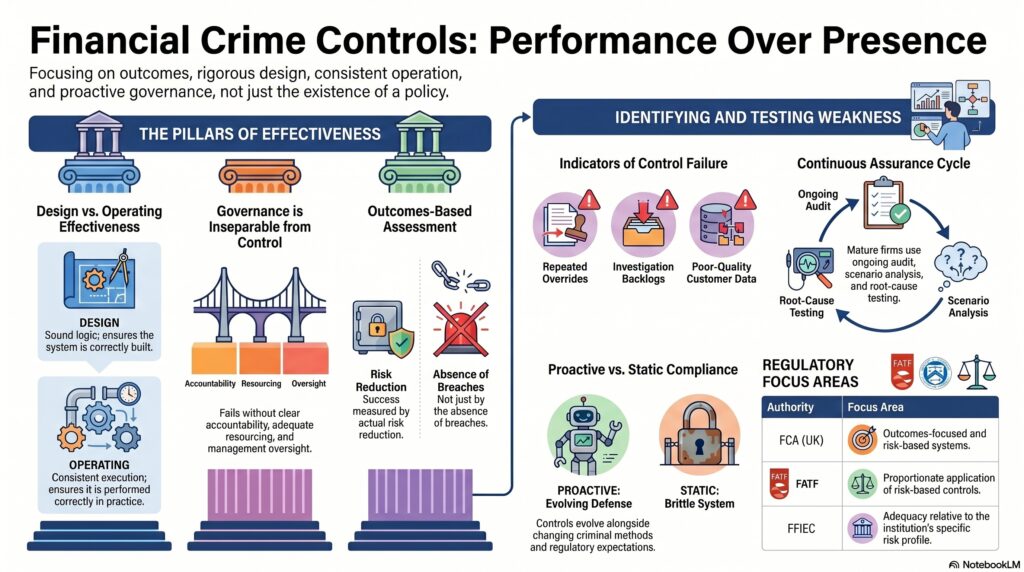

In the financial crime environment, control effectiveness should therefore be assessed across the full control lifecycle. This begins with design effectiveness: whether the control is logically capable of addressing the risk it is supposed to mitigate. It then extends to operating effectiveness: whether the control is actually being performed, consistently, by the right people or systems, with the right inputs, oversight, and escalation standards. A well-designed onboarding control, for example, may still be ineffective if staff override it too easily, if ownership data is unreliable, or if exceptions are poorly governed. FATF’s risk-based approach guidance makes clear that firms are expected to identify, assess, and understand their risks so that controls can be applied proportionately and effectively.

Watch on YouTube: Control Effectiveness

This is why control effectiveness cannot be measured solely by whether a breach has occurred. A control may appear to “work” simply because no problem has yet surfaced, when in fact it is weak but untested. Conversely, a control may generate alerts, escalations, or customer friction that reflect healthy detection rather than failure. Professional assessment therefore focuses on whether the control is appropriate for the risk, whether it produces reliable outputs, and whether management can evidence that it is achieving its intended purpose. The FCA’s guidance is explicitly outcomes-focused and risk-based, which supports this broader interpretation of effectiveness.

In practical terms, common indicators of weak control effectiveness include repeated override of controls without challenge, poor-quality customer files, persistent false positives or false negatives, investigation backlogs, inconsistent escalation decisions, failure to detect known typologies, weak management information, poor remediation follow-through, and lack of testing after control changes. In the BSA/AML context, FFIEC examination procedures focus on whether internal controls are adequate relative to the institution’s risk profile and whether they support ongoing compliance, which reinforces the point that effectiveness must be assessed against actual exposure rather than generic standards alone.

Control effectiveness is also inseparable from governance. A control may fail not because the rule or system is inherently flawed, but because no one owns it clearly, testing is weak, resourcing is inadequate, or management tolerates known deficiencies. FCA and FATF materials both emphasize that effective financial crime risk management depends on governance, oversight, and proportionate systems and controls. In practice, that means firms need clear accountability for control design, operation, monitoring, quality assurance, and remediation.

A mature firm does not treat control effectiveness as a one-time assessment. It should be tested continuously through assurance reviews, quality assurance, internal audit, thematic testing, scenario analysis, alert sampling, root-cause analysis, and review of incidents and near misses. The purpose is not only to confirm that controls are functioning, but to determine whether they remain effective as products, customer behavior, criminal methods, and regulatory expectations evolve. The FCA’s recent financial crime policy materials expressly describe a proactive, data-led supervisory approach focused on system and control effectiveness, which underscores that control effectiveness is an ongoing management obligation rather than a static compliance exercise.

Ultimately, control effectiveness is one of the most important concepts in the financial crime environment because it distinguishes formal compliance from real protection. A firm may have policies, systems, and procedures, but unless those controls work in a measurable, defensible, and risk-based way, the institution remains exposed. Effective controls are those that are properly designed, properly operated, regularly tested, and supported by strong governance. In that sense, control effectiveness is the practical measure of whether a financial crime framework is genuinely protecting the firm, its customers, and the wider financial system.