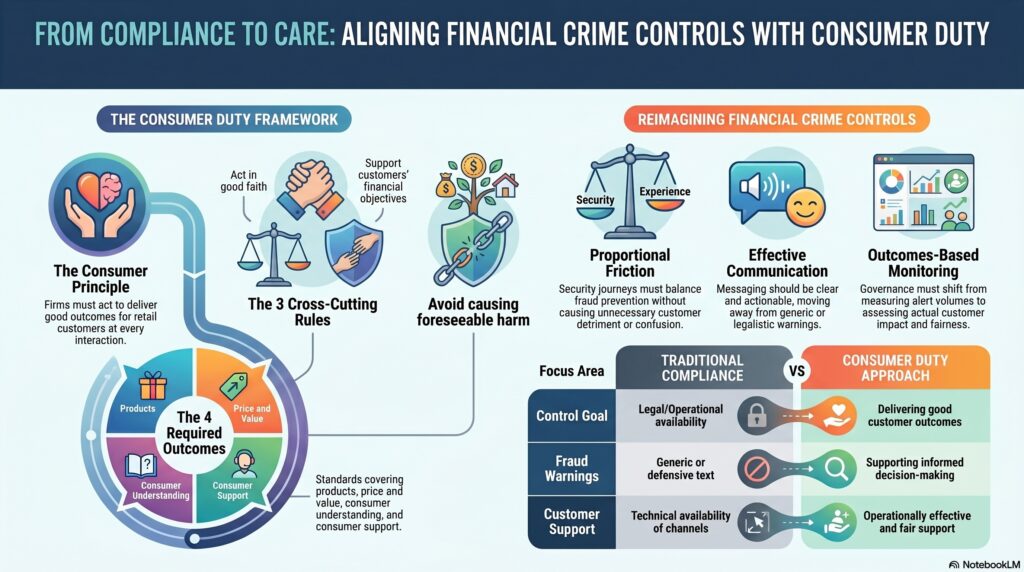

The Consumer Duty is the FCA’s framework for setting higher and clearer standards of consumer protection across financial services. The FCA states that the Duty requires firms to put customers’ needs first and, at its core, includes a consumer principle that says: “A firm must act to deliver good outcomes for retail customers.” It is supported by 3 cross-cutting rules—act in good faith, avoid causing foreseeable harm, and enable and support customers to pursue their financial objectives—and 4 outcomes covering products and services, price and value, consumer understanding, and consumer support.

In the financial crime environment, Consumer Duty is not an AML rule in the narrow sense, but it is highly relevant because many financial crime controls directly affect retail customer outcomes. Fraud prevention measures, scam warnings, account restrictions, onboarding checks, payment friction, communications, investigations, and reimbursement handling can all protect customers from harm or, if poorly designed, create avoidable detriment. The FCA’s current Consumer Duty materials emphasize customer outcomes, proportionality, and customer-journey design, including how firms apply friction throughout the journey. That matters because financial crime controls often sit exactly at those points of customer interaction.

From a professional compliance perspective, the Consumer Duty changes the way firms should think about financial crime controls. The question is no longer only whether a control is legally compliant or operationally available. The question is also whether it helps deliver good outcomes for retail customers. A fraud warning that is vague or confusing may satisfy a formal process requirement yet fail to support customer understanding. A scam intervention that arrives too late may not avoid foreseeable harm. A vulnerable customer process that is overly rigid may frustrate a customer’s financial objectives rather than enable them. This is an inference from the FCA’s formulation of the cross-cutting rules and the four outcomes.

Watch on YouTube: Consumer Duty

The connection is especially strong in fraud and scam prevention. APP fraud, impersonation scams, account takeover, and other forms of customer harm often arise in situations where firms must balance security, friction, speed, and customer autonomy. The Consumer Duty framework makes that balance more explicit. Firms should not assume that faster and lower-friction journeys are always better if they expose customers to foreseeable harm, nor should they assume that heavy friction is automatically defensible if it causes unnecessary customer detriment or confusion. The FCA’s 2025/26 focus areas specifically include reviewing customer journey design and how firms apply friction, which is directly relevant to financial crime controls.

Consumer understanding is another major area of overlap. Financial crime prevention depends heavily on warnings, disclosures, prompts, service communications, reimbursement explanations, and interactions during high-risk moments. Under the Consumer Duty, firms are expected to support informed decision-making and communicate in a way customers can understand. In practice, that means financial crime messaging should not be generic, legalistic, or purely defensive. Scam warnings, unusual-activity prompts, and fraud-related service communications should be designed to help customers understand what is happening and what action to take. The FCA’s current focus on the consumer understanding outcome reinforces that this is an active supervisory concern.

The Duty is also relevant to customer support. Financial crime incidents often become customer-service events as well as control events. A customer who has been scammed, locked out, wrongly flagged, or affected by account restrictions may be vulnerable, distressed, or financially exposed. The Consumer Duty requires firms to provide support that meets customers’ needs and enables them to pursue their financial objectives. In financial crime terms, this means investigations, fraud reporting channels, account recovery, reimbursement handling, and escalation pathways should be operationally effective and fair, not simply technically available. This is an inference from the FCA’s customer support outcome and cross-cutting rules.

There is also an important governance implication. The Consumer Duty is not just about frontline treatment; it requires firms to monitor outcomes and assess whether customers are actually receiving the intended protections. The FCA’s implementation and review materials stress outcomes monitoring, board and management responsibilities, and evidence of embedding the Duty. For financial crime teams, that means firms should not only measure alert volumes or fraud loss figures, but also assess whether controls are producing good customer outcomes—for example, whether scam interventions are timely, whether warnings are understood, whether vulnerable customers are supported, and whether high-friction controls are proportionate.

A mature firm therefore treats Consumer Duty as a lens through which financial crime controls should be designed and challenged. Customer due diligence, transaction monitoring, fraud prevention, authentication, communications, and reimbursement processes may all be legally necessary, but they should also be tested for fairness, comprehensibility, proportionality, and actual customer impact. The Duty does not displace AML, sanctions, or fraud obligations; it influences how those obligations should be implemented where retail customers are affected. That is consistent with FCA guidance stating that firms must consider the Duty alongside other applicable rules.

Ultimately, the Consumer Duty matters in the financial crime environment because it connects financial crime control design with customer outcomes. It requires firms to think beyond formal compliance and ask whether their fraud, scam, onboarding, and support arrangements actually protect retail customers, avoid foreseeable harm, and enable informed financial decision-making. In that sense, the Duty is not a separate topic from financial crime control; it is an important standard for judging whether those controls are working in a way that is fair, proportionate, and defensible.