Communications surveillance is the monitoring, review, analysis, and retention of business communications in order to identify misconduct, financial crime risk, regulatory breaches, and control failures. In the financial crime environment, it typically covers channels such as email, recorded voice, chat, messaging platforms, collaboration tools, and other electronic communications used in the course of business. Its importance lies in the fact that many forms of misconduct are planned, discussed, directed, concealed, or evidenced through communication rather than through transactional data alone. The FCA’s market abuse materials and Market Watch guidance make clear that surveillance arrangements are a key part of firms’ safeguards against market abuse.

From a professional financial crime perspective, communications surveillance is not simply a recordkeeping exercise. It is a control function that helps firms detect intent, context, coordination, and awareness. A trade or payment may look unusual on its own, but the surrounding messages can reveal whether it was discussed as a workaround, whether someone knew it was suspicious, whether false explanations were prepared, or whether multiple parties were coordinating misconduct. This is why communications surveillance is especially relevant to market abuse, insider dealing, manipulation, fraud, bribery and corruption, sanctions evasion, and certain AML investigations. The FCA’s Financial Crime Guide frames firms’ systems and controls broadly, while its market abuse publications focus specifically on surveillance arrangements as part of that control environment.

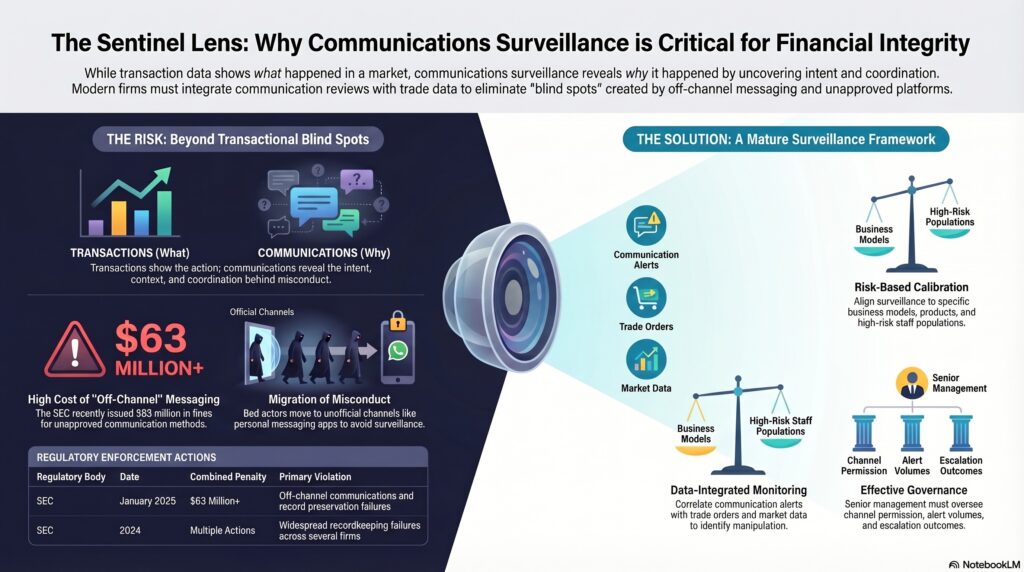

In capital markets, communications surveillance is most closely associated with market abuse prevention and detection. Trading data can show what happened in the market, but communications often help explain why it happened and whether there was improper intent or coordination. Messages between traders, sales staff, clients, brokers, or other market participants may indicate insider dealing, unlawful disclosure of inside information, spoofing, manipulative strategies, or attempts to conceal true purpose. ESMA’s market integrity materials emphasize that the market abuse framework is intended to guarantee integrity and investor confidence, while FCA supervisory commentary highlights the need for effective surveillance arrangements rather than a narrow focus on transaction data alone.

Communications surveillance also has a strong connection to recordkeeping compliance. A firm cannot surveil or investigate communications effectively if relevant records are not captured and preserved. Recent SEC enforcement actions on off-channel communications show how seriously regulators view this issue. In January 2025, the SEC announced that twelve firms agreed to pay more than $63 million combined over failures involving unapproved communication methods and record preservation, and it stated that the failures involved personnel at multiple levels, including supervisors and senior managers. Similar SEC actions were taken in 2024 against additional firms over widespread recordkeeping failures.

Watch on YouTube: Communications Surveillance

That recordkeeping dimension is critical in the financial crime environment because misconduct often migrates toward channels perceived as less visible or less controlled. Off-channel communications, personal devices, consumer messaging apps, and other unofficial channels can create blind spots in surveillance and weaken a firm’s ability to reconstruct events. The SEC’s recent enforcement position makes clear that missing or unpreserved business communications deprive regulators of material evidence in investigations. In practical terms, this means communications surveillance is inseparable from channel governance: firms need not only to review communications, but to ensure that relevant communications occur on approved, retained, and reviewable channels in the first place.

A professionally mature communications surveillance framework therefore depends on more than keyword searches across archived mailboxes. It should be risk-based and aligned to the firm’s business model, products, client base, and principal misconduct risks. In a trading environment, that may mean focusing on inside information, order handling, pricing discussions, benchmark conduct, and pre-arranged trading patterns. In a broader financial crime environment, it may also include fraud indicators, bribery language, suspicious payment instructions, sanctions-related circumvention attempts, or coded efforts to avoid escalation. FCA Market Watch 69 emphasizes that surveillance arrangements should be proportionate to the firm’s business, but still effective in detecting the relevant risks.

Communications surveillance is also increasingly data-integrated rather than standalone. The FCA’s 2024 market abuse surveillance TechSprint highlighted approaches that correlate communications with trade orders and market data to identify coordinated manipulative activity. That reflects an important development in the control environment: firms are moving away from treating communications review as separate from trade surveillance and toward models that combine communications, trading behavior, and other risk signals. This is especially valuable where misconduct is only visible when intent and action are examined together.

From an operational standpoint, good communications surveillance requires clear scope, reliable capture, structured review, escalation standards, and defensible documentation. Firms need to know which channels are in scope, which staff populations are higher risk, what lexicons or models are being used, how alerts are triaged, how investigations are documented, and when concerns are escalated into compliance, legal, HR, or regulatory reporting channels. Weakness in any of those areas can reduce the control to a formal exercise without meaningful detection value. FCA supervisory commentary on market abuse surveillance has repeatedly focused on implementation quality rather than policy existence alone.

Governance is therefore central. Senior management should understand which communication channels are permitted, how off-channel use is controlled, how surveillance is calibrated, what the alert volumes and escalation outcomes look like, and whether the framework is actually detecting issues that matter. Inadequate governance can leave firms exposed to both misconduct risk and recordkeeping failures. The SEC’s off-channel enforcement actions are a clear illustration of this: regulators were not only concerned with missing records, but with the cultural and supervisory weaknesses that allowed unapproved communications to become normalized.

Ultimately, communications surveillance is a core control in the financial crime environment because many serious risks are communicated before they are executed. It helps firms detect intent, coordination, awareness, and concealment in ways that transaction monitoring alone cannot. When properly designed, it strengthens market abuse controls, fraud investigations, recordkeeping discipline, and broader conduct oversight. When weak or fragmented, it creates blind spots that can allow misconduct to develop on channels that are poorly captured, poorly reviewed, or deliberately avoided.