A cash-intensive business is a business whose operating model involves a high volume of cash receipts, cash payments, or both as a normal part of trading activity. Typical examples include convenience retail, hospitality, bars, restaurants, transport services, car washes, amusement and gaming venues, and certain parts of the personal-services sector. In the financial crime environment, cash-intensive businesses are important not because cash use is inherently improper, but because heavy cash activity can make the source, purpose, and legitimacy of funds harder to verify and easier to disguise within ordinary commercial operations. Regulators and standard-setters consistently treat customer type, business activity, cash usage, geography, and transaction profile as relevant AML risk factors within a risk-based framework.

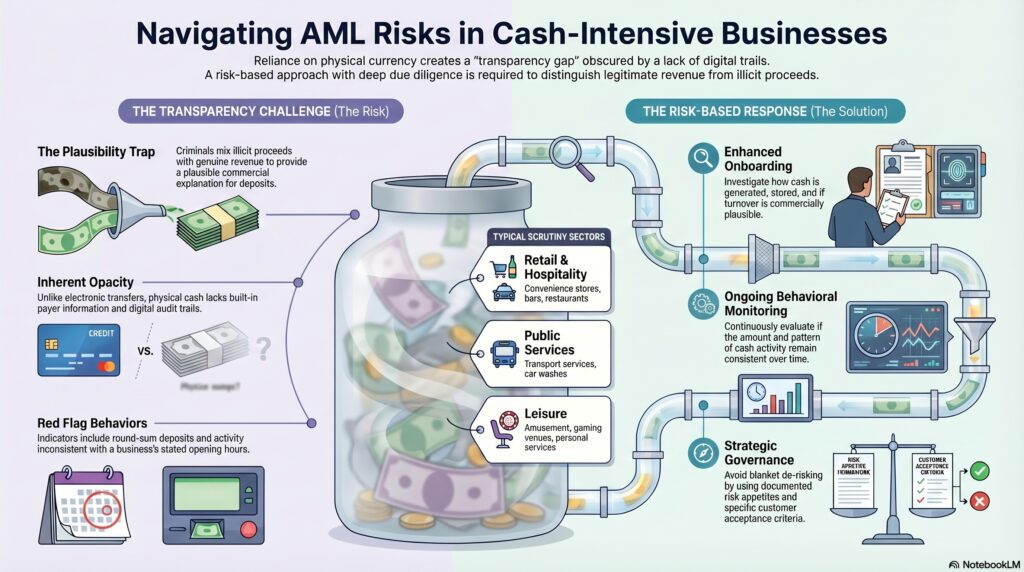

From a professional financial crime perspective, the core risk is that a cash-intensive business can provide a plausible commercial explanation for large volumes of physical currency entering the financial system. That creates an opportunity for criminal proceeds to be mixed with genuine business takings, deposited into business accounts, and then presented as legitimate revenue. This risk is especially relevant to money laundering, tax evasion, fraud proceeds placement, and wider financial opacity. FATF’s guidance on risk-based AML supervision and national risk assessment work recognizes cash activity and the informal economy as factors that can increase vulnerability to abuse.

A cash-intensive business is therefore not automatically a high-risk business, but it is usually a business type that requires closer scrutiny. The distinction matters. Many legitimate businesses depend heavily on cash because of customer preference, sector norms, location, or the nature of the service provided. The financial crime question is not whether the business handles cash, but whether the amount, pattern, frequency, and explanation for that cash activity are credible and consistent with the stated business model. A small food outlet making modest daily cash deposits may be entirely normal. A newly formed company with limited visible activity but unusually high and erratic cash deposits may present a very different risk picture. This reflects the risk-based approach regulators expect firms to apply to customer relationships and CDD.

One of the reasons cash-intensive businesses require careful assessment is that cash is inherently less transparent than many electronic payment channels. Cash does not carry built-in payer information, payment narrative, or digital audit trails in the way that account-to-account transfers often do. Once deposited into a bank account, however, it begins to acquire the appearance of legitimacy, especially if it is described as ordinary business turnover. This makes cash-heavy sectors potentially attractive to criminals seeking to place illicit funds into the financial system while relying on the outward normality of a retail or service business. FATF’s material on cash activity and the informal economy underscores that extensive cash use can create vulnerabilities that should be understood within AML systems.

Watch on YouTube: Cash-Intensive Business

In practical terms, institutions dealing with cash-intensive businesses need to assess several dimensions of risk. These include the nature of the business, expected daily and monthly cash volumes, location, customer base, ownership structure, source of funds, source of wealth where relevant, use of third parties, and whether the activity is consistent with the firm’s understanding of the customer. The FCA’s financial crime guidance emphasizes that firms should know their customers, understand the nature of the business relationship, and maintain systems and controls proportionate to the risk. In a cash-intensive context, that means firms should not accept vague or generic explanations for substantial cash flows where more specific and credible information should reasonably be available.

Cash-intensive businesses also raise particular issues at onboarding. It is not enough to identify the legal entity and collect standard corporate documents. A professionally mature due diligence process should seek to understand why the business is cash-heavy, how cash is generated, who handles it, how it is stored, how often it is deposited, whether third-party cash collection services are used, and whether the turnover profile is commercially plausible. Beneficial ownership and control are also important, because cash-heavy structures can be used to obscure the involvement of higher-risk individuals or concealed controllers. This is consistent with the wider risk-based due diligence approach reflected in FATF and FCA guidance.

Ongoing monitoring is equally important, because the risk profile of a cash-intensive business is not static. A business that appears normal at onboarding may later display suspicious patterns such as unusually frequent round-sum cash deposits, activity inconsistent with stated opening hours or sector norms, large spikes in cash turnover without clear business explanation, significant divergence between cash deposits and declared business scale, or rapid movement of deposited cash onward to other accounts. These types of indicators do not prove criminality on their own, but they are precisely the sorts of behaviors that should feed into transaction monitoring, account review, and investigative escalation. The FCA’s guide treats effective monitoring as a key element of financial crime systems and controls.

There is also a wider access and de-risking dimension. The FCA has noted concerns that some small businesses, including cash-intensive businesses, may face difficulty accessing payment accounts because firms view them as higher risk from a financial crime perspective. That is an important reminder that cash intensity should not be treated as an automatic exclusion category. A mature compliance framework applies enhanced scrutiny where justified, but still distinguishes between legitimate higher-risk businesses and relationships that are genuinely unacceptable. Blanket assumptions can create poor customer outcomes without necessarily improving financial crime controls.

Governance is therefore essential. Firms should have documented risk appetite, customer acceptance criteria, escalation standards, and monitoring approaches for cash-intensive businesses. Relationship managers, onboarding teams, fraud teams, and AML investigators should have a shared understanding of what normal cash activity looks like for different sectors and what deviations require challenge. Management information should also identify concentrations in cash-heavy sectors, unusual deposit behavior, and cases where the rationale for cash usage is weak or deteriorating. This aligns with the broader expectation that institutions assess inherent risk factors and describe associated controls consistently across their business.

Ultimately, a cash-intensive business is significant in the financial crime environment because heavy reliance on cash can make legitimate turnover and illicit proceeds harder to distinguish. That does not make such businesses inherently improper, but it does mean they require stronger understanding, more credible due diligence, and closer behavioral monitoring than many low-cash business models. For financial institutions, the key issue is not simply whether a customer handles cash, but whether the volume, explanation, and pattern of that cash activity make commercial sense and remain consistent over time.