Beneficial ownership refers to the natural person or persons who ultimately own, control, or benefit from a legal entity or arrangement, even where that ownership or control is exercised indirectly through layers of companies, nominees, trusts, or other structures. The FCA’s Financial Crime Guide describes a beneficial owner as the natural person who ultimately owns or controls the customer, and FATF’s transparency work is aimed at identifying the real individuals behind legal persons and arrangements so they cannot be used by money launderers, tax evaders, sanctions evaders, and corrupt actors.

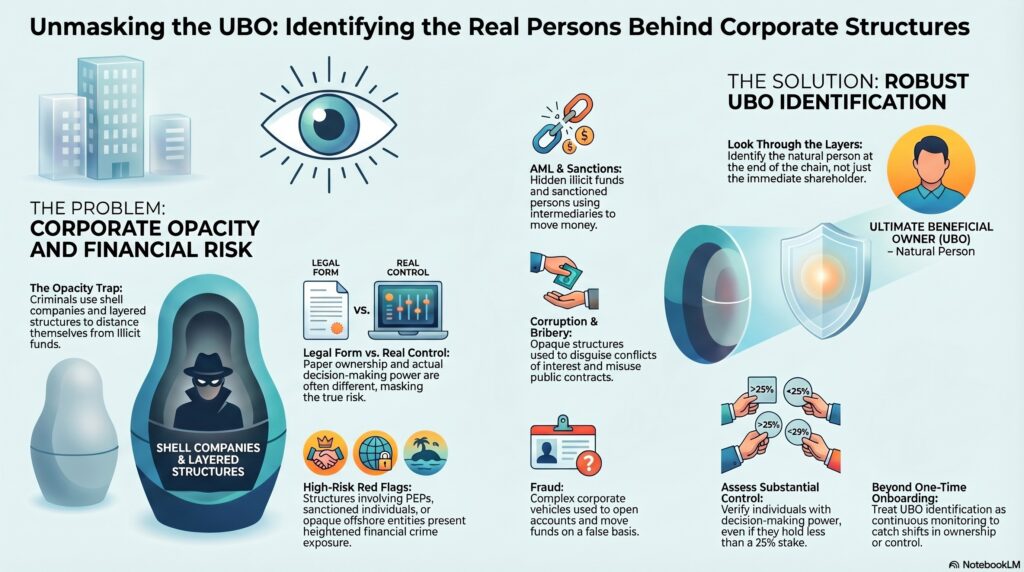

In practice, the term Ultimate Beneficial Owner, or UBO, is used to emphasize that the objective is to identify the person at the end of the ownership or control chain, not merely the immediate shareholder or legal owner on paper. That distinction is critical in the financial crime environment because legal ownership and real control are not always the same. A company may be owned by another company, which is in turn owned by a trust, nominee, or offshore entity, yet the true decision-maker and economic beneficiary may still be a single individual or small group of individuals hidden behind that structure. FATF’s guidance repeatedly focuses on obtaining adequate, accurate, and up-to-date beneficial ownership information for exactly this reason.

From a professional financial crime perspective, beneficial ownership is a core transparency issue. Criminals rarely advertise their involvement in a business or account directly. Instead, they often rely on opacity: shell companies, front companies, nominee shareholders, layered ownership structures, trusts, informal control arrangements, and cross-border entities designed to make it difficult to identify who is really behind a customer relationship. FATF explicitly links stronger beneficial ownership transparency to identifying corrupt actors, money launderers, sanctions evaders, and tax evaders who hide behind shell companies and complex structures. That makes beneficial ownership analysis central not only to AML compliance, but also to sanctions, fraud, bribery and corruption, tax crime, and wider financial integrity.

This is why beneficial ownership matters so much at onboarding. A firm may identify the legal entity customer correctly and still fail to understand the real risk if it does not determine who ultimately owns or controls that entity. A company with ordinary registration documents and apparently legitimate business activity may still present heightened risk if its UBO is a politically exposed person, a sanctioned individual, a fraud facilitator, or a person linked to adverse media or high-risk jurisdictions. FCA guidance makes clear that firms must identify customers and, where applicable, their beneficial owners, then verify their identities and understand the purpose of the relationship.

Watch on YouTube: Beneficial Ownership and Ultimate Beneficial Owner (UBO)

A professionally mature approach also recognizes that beneficial ownership is about control as well as ownership. A person can be the UBO even if they do not hold the largest visible shareholding, provided they ultimately exercise substantial influence, decision-making power, or economic control over the entity. This is especially important in complex structures where share percentages alone do not tell the full story. FinCEN’s beneficial ownership rule framework, for example, uses both ownership and substantial control concepts, and its fact sheet states that a beneficial owner includes an individual who directly or indirectly exercises substantial control over a reporting company or owns or controls at least 25 percent of its ownership interests.

That distinction is operationally important because many high-risk structures are designed specifically to defeat simplistic threshold-based ownership checks. If firms focus only on visible percentage ownership, they may miss people who direct the entity through voting agreements, nominee arrangements, family members, informal influence, trusts, or layered corporate vehicles. In the financial crime environment, beneficial ownership analysis therefore requires institutions to understand not just shareholding, but governance, rights, control mechanisms, and the commercial logic of the structure. This is an inference supported by FATF’s emphasis on transparency of both legal persons and legal arrangements, and by FinCEN’s use of substantial control alongside ownership.

Beneficial ownership is also central to ongoing monitoring, not just initial due diligence. Ownership and control structures can change over time through share transfers, board changes, trust amendments, restructuring, nominee replacement, or changes in who actually directs the business. A customer who was acceptable at onboarding may become higher risk if a new UBO emerges, if control shifts to a higher-risk jurisdiction, or if previously hidden ownership becomes visible through adverse media or external inquiry. The FCA’s financial crime materials and FATF’s guidance both stress the importance of adequate, accurate, and up-to-date beneficial ownership information, which means firms cannot treat beneficial ownership as a one-time box-ticking exercise.

In the financial crime environment, weak beneficial ownership controls create several kinds of exposure. First, they increase AML risk because institutions may unknowingly provide services to criminals using corporate opacity to distance themselves from illicit funds. Second, they increase sanctions risk because sanctioned persons may conceal control through intermediaries or layered holdings. Third, they increase corruption and bribery risk because hidden ownership can be used to disguise conflicts of interest, politically exposed influence, or misuse of public contracts. Fourth, they increase fraud risk because complex or opaque structures can be used to open accounts, obtain facilities, or move funds on a false basis. FATF’s beneficial ownership work is expressly designed to counter this kind of misuse of legal entities and arrangements.

A mature control framework for beneficial ownership therefore requires more than collecting company registry extracts. Firms need to identify the ownership chain, determine where control really sits, assess whether the structure makes commercial sense, and verify the relevant individuals to a level proportionate to risk. This often includes reviewing corporate documents, registers, trust information, governance rights, shareholder arrangements, and supporting evidence that explains how ownership and control operate in practice. Where structures are unusually layered, cross-border, opaque, or inconsistent with the stated business purpose, enhanced scrutiny is often necessary. FATF’s guidance on legal persons and legal arrangements reflects this emphasis on verification and practical understanding rather than simple formal ownership recording.

The U.S. position also illustrates how dynamic this area is. FinCEN states that beneficial ownership information refers to identifying information about the individuals who directly or indirectly own or control a company, but as of March 2025 the BOI reporting regime was changed so that U.S. companies and U.S. persons became exempt from the requirement to report BOI to FinCEN, while certain foreign companies remained subject to reporting requirements. That change is specifically about the reporting regime; it does not eliminate the broader importance of beneficial ownership in AML and customer due diligence.

Ultimately, beneficial ownership and the concept of the Ultimate Beneficial Owner are fundamental in the financial crime environment because they answer one of the most important compliance questions: who is really behind the customer?Without that answer, onboarding decisions, sanctions screening, transaction monitoring, risk rating, and suspicious activity assessment are all built on incomplete foundations. In practical terms, beneficial ownership analysis is the mechanism by which institutions move beyond legal form and identify the real human beings who own, control, or benefit from an entity or arrangement. That is why it remains a core part of credible AML, sanctions, and wider financial crime control frameworks.