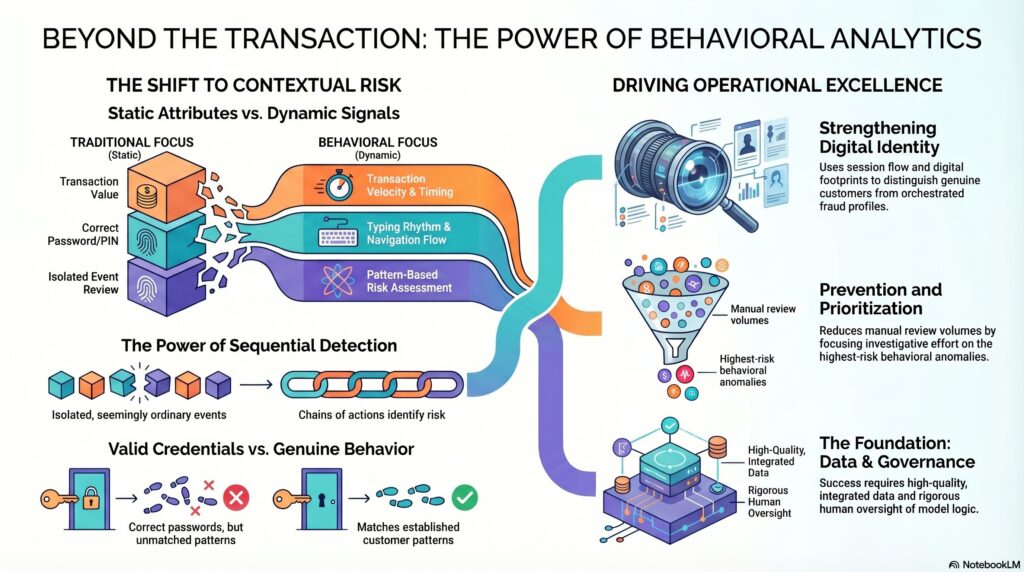

Behavioral analytics is the use of data about actions, patterns, habits, and interactions to identify conduct that is unusual, inconsistent, risky, or potentially suspicious. In the financial crime environment, it is used to assess how customers, users, devices, accounts, or counterparties behave over time and whether that behavior aligns with what would normally be expected. Rather than focusing only on static attributes such as name, address, or transaction value, behavioral analytics examines dynamic signals such as login habits, payment timing, transaction velocity, navigation patterns, device usage, beneficiary creation, account changes, and deviations from established activity. This makes it especially valuable in environments where criminal misuse may not be visible through traditional rule-based controls alone.

From a professional financial crime perspective, behavioral analytics is important because many modern fraud and AML risks are context-dependent rather than obvious on the face of a single event. A payment may appear ordinary in amount, but suspicious when it follows a password reset, a new-device login, a mobile-number change, and the creation of a new payee. A customer record may appear valid at onboarding, but riskier when later behavior suggests mule activity, synthetic identity abuse, or account takeover. In this way, behavioral analytics helps institutions move from isolated-event review to pattern-based risk assessment. FCA guidance on financial crime systems and controls, including transaction monitoring and responsible innovation, supports this broader move toward more effective, data-led controls.

One of the core strengths of behavioral analytics is that it can help distinguish valid credentials from valid behavior. Traditional access controls often rely heavily on whether the correct username, password, or authentication factor was used. That remains important, but FFIEC guidance makes clear that institutions should take a risk-based approach to authentication and access, not rely on any single factor in isolation. Behavioral analytics adds a deeper layer by examining whether the way an account is being accessed is consistent with the genuine customer’s established pattern. This is especially relevant in account takeover, credential stuffing, identity misuse, and other cyber-enabled financial crime typologies where criminals may successfully use correct credentials in an incorrect context.

In fraud prevention, behavioral analytics is particularly effective because fraud often reveals itself through sequences of actions rather than through one obviously fraudulent event. Criminals may log in from a new device, browse security settings, reset credentials, suppress alerts, create a new beneficiary, and then send a payment. Each step on its own may appear explainable. Viewed together, the behavior may be highly suspicious. This is why behavioral analytics is now closely associated with account takeover monitoring, payment fraud detection, application fraud, mule-account identification, and scam intervention. The FCA has also noted current use cases for advanced analytics and synthetic data in fraud detection, APP fraud, and AML, which reinforces the growing importance of behavior-based approaches in financial crime controls.

Watch on YouTube: Behavioral Analytics

Behavioral analytics is also increasingly relevant to AML and transaction monitoring. Traditional AML systems have often relied on fixed rules and thresholds, such as transaction value limits or pre-defined scenario triggers. Those remain useful, but they can miss suspicious activity that is unusual relative to the customer’s own profile rather than unusual in absolute terms. Behavioral analytics strengthens this by comparing actual account behavior against expected behavior, normal historical activity, peer-group patterns, or linked-network behavior. For example, it may help identify rapid pass-through of funds, sudden shifts in account usage, unexpected counterparties, unusual transaction timing, or activity inconsistent with the customer’s business purpose. FCA guidance on transaction monitoring and systems and controls is directly relevant here because it emphasizes effective, risk-based monitoring rather than mechanical thresholding alone.

In digital identity and onboarding, behavioral analytics can support a more mature understanding of whether the person interacting with the institution is behaving like a genuine customer or like an orchestrated fraud profile. FATF’s guidance on digital identity links digital signals and assurance mechanisms to customer identification and verification within AML/CFT frameworks. While the FATF documents do not frame this only as “behavioral analytics,” they support the broader point that reliable digital identity and related signals can strengthen customer due diligence and reduce financial crime risk. In practice, institutions often use behavioral indicators such as typing rhythm, session flow, device consistency, time-to-complete application steps, and digital-footprint coherence as supplementary evidence when assessing identity integrity or application credibility. This is an inference based on FATF’s treatment of digital identity assurance within AML/CFT controls.

A major advantage of behavioral analytics is that it can improve both prevention and prioritization. In prevention, it helps firms intervene before a high-risk action is completed by identifying suspicious patterns early enough to add friction, escalate for review, or stop the activity outright. In prioritization, it helps firms focus investigative effort on alerts or events where the behavioral context suggests genuine risk rather than harmless anomaly. That can improve operational efficiency by reducing low-value manual review and surfacing the cases that are most likely to represent fraud, laundering, or account abuse. However, this benefit only exists if the underlying models, logic, and data are well governed. If the analytics are poorly designed, institutions may create large volumes of noise, miss genuine threats, or generate outcomes that are difficult to explain and defend.

Governance is therefore central. Behavioral analytics should not be treated as a black-box enhancement layered onto existing controls without oversight. In the financial crime environment, institutions need clear ownership for model design, threshold setting, validation, monitoring, tuning, and issue remediation. They also need to understand how behavioral indicators are being used in decision-making, what data supports them, and whether they are producing meaningful improvements in detection quality. FCA materials on responsible innovation and the use of AI in transaction monitoring reflect this wider expectation that firms remain accountable for the effectiveness of systems and controls even when more advanced analytics are introduced.

Data quality is another critical factor. Behavioral analytics depends on consistent, well-structured data across sessions, channels, transactions, devices, and customer records. If customer histories are fragmented, device data is weak, timestamps are inconsistent, or event logging is incomplete, the behavioral picture may be distorted. In that situation, the analytics may appear sophisticated while producing weak or misleading outputs. This is one reason why advanced detection methods often fail in practice when institutions attempt to deploy them on poor-quality or poorly integrated data environments. FATF’s broader technology guidance underscores that the effectiveness of new technologies depends on how they are implemented, governed, and interpreted.

There is also a customer-treatment dimension. Behavioral analytics can help institutions protect customers from scams, account takeover, and impersonation fraud by identifying subtle warning signs before loss occurs. But if controls are poorly calibrated, they can also create friction, false positives, and adverse outcomes for legitimate users whose behavior falls outside an assumed pattern. A professionally mature framework therefore applies behavioral analytics proportionately, with clear escalation routes, review standards, and customer communication where intervention occurs. The objective is not to block anything unusual, but to distinguish between genuinely risky behavior and legitimate variation in how customers use services.

Ultimately, behavioral analytics is important in the financial crime environment because it helps institutions understand not just what happened, but how it happened and whether that behavior makes sense in context. It strengthens fraud prevention, authentication, transaction monitoring, and identity assurance by focusing on patterns, sequences, and deviations rather than static data points alone. In an environment where criminals increasingly exploit valid credentials, genuine customer infrastructure, and ordinary payment channels, that contextual understanding is essential. For that reason, behavioral analytics should be seen as a core capability in modern financial crime frameworks, provided it is supported by strong data, effective governance, and informed human oversight.