Batch screening is the process of screening multiple records, transactions, customers, counterparties, or payment instructions together in a grouped or scheduled run rather than individually in real time. In the financial crime environment, batch screening is commonly used to test customer populations, payment files, account databases, beneficiary records, or other large datasets against sanctions lists, watchlists, politically exposed person data, adverse media sources, internal risk lists, or other screening criteria. It is an important operational control because financial institutions often need to screen large volumes of information efficiently while maintaining consistency, traceability, and appropriate escalation.

From a professional financial crime perspective, batch screening is best understood as a control mechanism designed for scale. Real-time screening is often used at the point of onboarding, payment execution, or customer interaction, where an immediate decision is required. Batch screening serves a different purpose. It allows institutions to review populations or activity sets periodically, after data updates, before processing files, or as part of ongoing control cycles. This is particularly valuable where the risk is not confined to a single event, but may emerge across a portfolio, a payment batch, a refreshed sanctions list, or a large population of existing customers whose risk status may have changed over time.

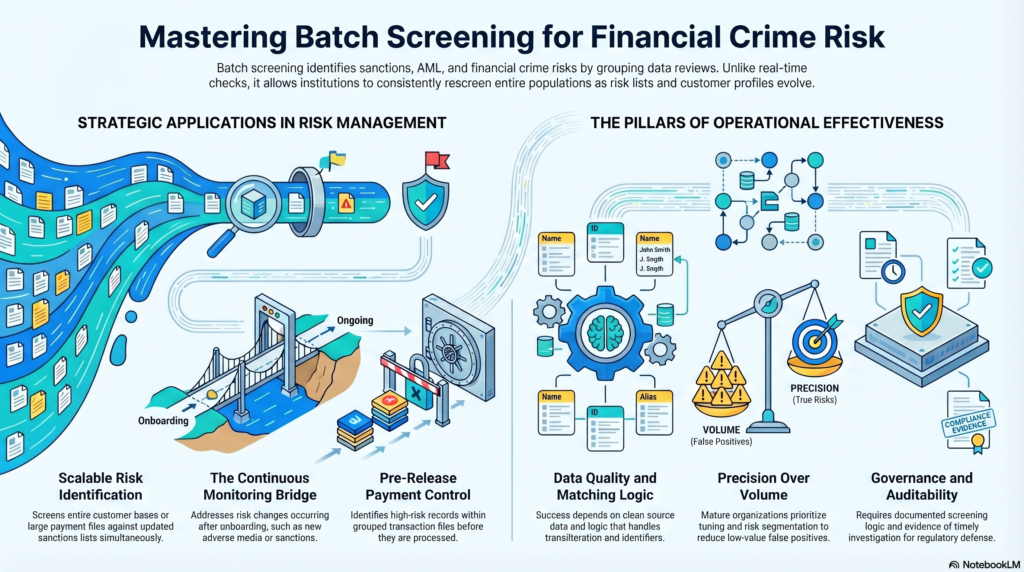

In practical terms, batch screening is widely used in several core financial crime scenarios. A firm may screen its full customer base overnight after receiving an updated sanctions or politically exposed person list. It may screen a batch of outgoing payments before file release. It may screen newly uploaded beneficiary records, historic customer databases following a data remediation exercise, or portfolios of counterparties associated with higher-risk sectors or jurisdictions. In each case, the purpose is to identify records that may require investigation, escalation, blocking, enhanced due diligence, or further review. The strength of batch screening lies in its ability to apply the same logic and screening criteria consistently across a large volume of data.

This consistency is one of the main reasons batch screening is so important in the financial crime environment. Financial crime controls often depend on whether names, entities, or counterparties can be identified as linked to sanctions exposure, law enforcement interest, politically exposed status, adverse media concerns, or other indicators of heightened risk. If screening were performed only when an account is opened or a payment is initiated, institutions could miss important changes that occur later. A customer who appeared low risk at onboarding may become high risk because of sanctions developments, new adverse media, beneficial ownership changes, or later associations with suspicious entities. Batch screening helps address that problem by allowing institutions to rescreen entire populations when new information becomes available.

Watch on YouTube: Batch Screening

At the same time, batch screening is not simply a technical exercise in running names through a database. Its effectiveness depends heavily on the quality of the data being screened, the quality of the lists against which it is screened, and the matching logic used to identify possible hits. Poor source data, inconsistent formatting, missing identifiers, weak transliteration handling, duplicate records, or overly simplistic matching rules can all undermine outcomes. In the financial crime environment, this matters because a screening process that appears comprehensive on paper may in practice be missing relevant matches or overwhelming investigators with low-value false positives. A batch process is only as strong as its input data, matching design, and downstream review capability.

One of the most important distinctions in batch screening is the difference between efficiency and effectiveness. Batch screening is operationally efficient because it allows large numbers of records to be screened together. But that does not automatically make it an effective financial crime control. If a firm screens millions of records but cannot investigate the results promptly, cannot distinguish true matches from false positives, or cannot escalate confirmed concerns in a timely way, the control may create an appearance of assurance without delivering meaningful risk reduction. This is particularly important in sanctions and watchlist environments, where delayed or poorly handled batch-screening results can create legal, regulatory, and reputational exposure.

Batch screening is especially relevant to sanctions compliance. Institutions frequently use it to rescreen customer bases and transaction datasets whenever sanctions lists are updated or when there is heightened geopolitical risk. In this context, the timing of the batch run, the quality of the data, and the speed of post-match review become critical. A large-scale rescreening exercise may identify potential matches that require urgent investigation, restrictions on account activity, or immediate escalation. This means batch screening is not merely a passive monitoring tool. It can trigger significant operational and legal consequences if credible matches are identified.

It is also highly relevant to AML and customer due diligence. Batch screening can be used to identify politically exposed persons, adverse media hits, connected-party risks, beneficial ownership concerns, or internal watchlist matches across a customer population. It can support remediation exercises, periodic KYC reviews, and retrospective checks after risk models or screening parameters are changed. In this sense, batch screening often acts as a bridge between static onboarding controls and dynamic ongoing monitoring. It allows the institution to revisit existing relationships in light of new intelligence, new regulatory expectations, or improved detection logic.

From a payments perspective, batch screening is often applied to grouped transaction files, beneficiary uploads, or recurring payment instructions. Here, the control objective is slightly different. The institution is not just trying to understand the long-term risk profile of a customer; it is trying to determine whether a file or payment set contains records that should be held, investigated, or blocked before processing. In this environment, batch screening must operate within operational deadlines. If it is too slow, it creates payment disruption. If it is too weak, suspicious payments may be processed without effective review. This balance between control strength and operational throughput is one of the central challenges in designing batch-screening frameworks.

A further complexity is the management of false positives. Large batch runs often generate high volumes of potential matches, especially where names are common, records are incomplete, or matching thresholds are highly sensitive. Inexperienced organizations may respond by loosening filters too far in order to reduce alert volumes, but that can increase the risk of missing genuine matches. More mature organizations focus instead on data quality, tuning, risk segmentation, and effective case handling. The goal is not simply to reduce alert numbers, but to improve the quality of the screening output so that investigators can focus on the most credible and highest-risk cases.

Governance is essential in this area. Batch screening should be supported by clear ownership, documented screening logic, list-management controls, review timeframes, escalation standards, and evidence of outcome tracking. Institutions should know when batch runs occur, what populations are covered, what lists are included, how exceptions are handled, and how quickly potential matches are reviewed. They should also understand where batch screening fits in relation to real-time screening, manual review, and broader financial crime monitoring. Without this governance structure, batch screening can become a mechanical routine that generates data without driving meaningful control action.

There is also a strong audit and evidencing dimension. Because batch screening is often used to support sanctions, AML, and watchlist compliance, institutions may need to demonstrate that screening occurred, that the relevant populations were included, that current lists were used, and that matches were handled appropriately. This means recordkeeping around batch runs, parameters, outputs, and case resolutions is an important part of the control environment. A firm that cannot evidence how and when it performed a batch screening exercise may struggle to defend its compliance position even if the process itself was intended to be robust.

Ultimately, batch screening is a critical control in the financial crime environment because it allows institutions to apply screening logic consistently across large populations of customers, transactions, and counterparties. It supports sanctions compliance, customer due diligence, payment control, and periodic risk reassessment at a scale that manual review alone could not achieve. But its value depends on more than running large datasets through a system. Effective batch screening requires strong data quality, intelligent matching logic, timely investigation, clear governance, and a control framework capable of turning bulk screening results into real financial crime risk decisions.