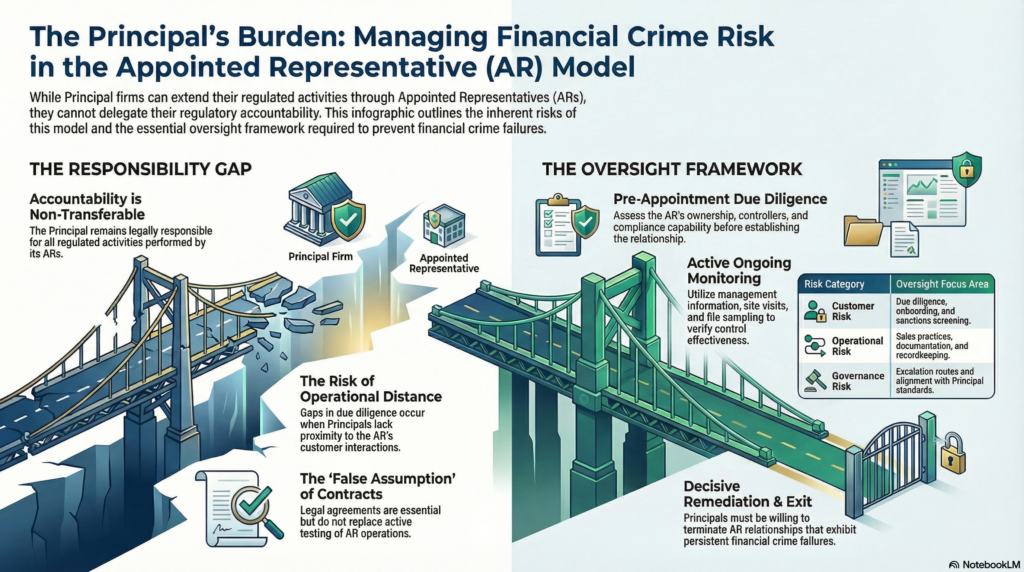

An Appointed Representative, commonly referred to as an AR, is a person or business that carries on certain regulated activities under the responsibility of an authorized firm, known as the principal. In the UK model, the principal remains responsible for the regulated activities carried out by its AR and is expected to exercise effective oversight over that relationship. The FCA’s current guidance is explicit that principals must ensure their ARs are fit and proper, comply with applicable rules, and are subject to robust oversight, including oversight of financial crime risk.

In the financial crime environment, the significance of the AR model lies in the fact that it extends regulated activity beyond the directly authorized firm while keeping legal and regulatory responsibility with the principal. That creates a specific control challenge. The principal may not perform every customer interaction, onboarding step, sales activity, or operational process itself, yet it remains accountable for how those activities are conducted. Where the AR model is poorly governed, this can create gaps in customer due diligence, sanctions screening, fraud controls, complaints handling, and general financial crime oversight. The FCA has highlighted exactly this concern in recent work, noting that principals need effective, documented controls covering their ARs, including controls for managing financial crime risks.

From a professional financial crime perspective, an AR relationship should not be viewed as a simple distribution or commercial arrangement. It is a delegated operating structure within a regulated framework, and that means the principal must understand the AR’s business model, customer base, products, delivery channels, jurisdictions, governance, and control environment in enough depth to assess whether the AR can be supervised safely. If the principal treats the AR as commercially convenient but operationally distant, the risk of control failure rises materially. In practice, the AR may become the point at which high-risk customers are onboarded, where weak sales practices emerge, where suspicious activity indicators are missed, or where poor documentation undermines the defensibility of the wider compliance framework. This is an inference drawn from the FCA’s published expectations around principal oversight and financial crime controls.

The financial crime risks associated with ARs often arise from misalignment between responsibility and operational proximity. The principal holds the regulatory responsibility, but the AR may hold the direct customer relationship, generate the business, collect the information, and influence the way controls are applied in practice. That makes oversight particularly important at the point of onboarding and throughout the life of the relationship. If an AR is introducing customers, handling regulated sales, or interacting with higher-risk segments, the principal needs assurance that customer due diligence, suitability, conduct controls, and escalation standards are being applied to the same standard that would be expected inside the principal’s own business. The FCA’s supervisory approach to principals and ARs is built around this expectation of active oversight rather than passive reliance.

Watch on YouTube: Appointed Representative

A professionally mature principal therefore approaches AR oversight as a financial crime control framework in its own right. That begins with due diligence before appointment. The principal should understand the AR’s ownership, controllers, business activities, competence, compliance capability, complaints history, customer profile, and any features that create elevated fraud, AML, or sanctions risk. This is particularly important where the AR operates in sectors, products, or customer segments that are more vulnerable to abuse. The FCA’s good and poor practice material on AR oversight emphasizes stronger due diligence and ongoing monitoring rather than a one-time onboarding exercise.

Ongoing oversight is equally important because financial crime risk in AR relationships is not static. The principal should have visibility over business volumes, customer types, complaints trends, exception handling, file quality, financial crime referrals, and any changes in the AR’s business model. It should also understand whether the AR is expanding into new products, geographies, or customer groups that may alter the risk profile materially. Recent FCA reporting requirements even include data points related to AR exits for financial crime reasons, which underlines how directly the regulator connects AR oversight to financial crime governance.

One of the central risks in this model is the false assumption that principal responsibility can be satisfied through contracts alone. Contractual terms are important, but they do not replace real oversight. A principal may have a well-drafted agreement and still fail if it does not test how the AR operates in practice. Effective oversight requires management information, regular review, thematic testing, site visits where appropriate, file sampling, escalation routes, and the authority to intervene where concerns arise. The FCA’s published materials make clear that principals are expected to oversee ARs effectively and that this obligation includes ensuring compliance with the rules in relation to the AR’s activities.

In the financial crime environment, this means the principal should be able to answer several core questions at any time. Does the AR understand the principal’s standards for customer due diligence, sanctions, fraud prevention, and escalation? Are higher-risk relationships being identified and referred appropriately? Is there adequate recordkeeping? Are suspicious indicators being recognized and escalated, or is the AR functioning mainly as a sales channel with limited compliance discipline? Are there commercial incentives creating pressure to onboard or retain customers who should receive greater scrutiny? These are the types of questions that determine whether the AR model is operating safely or creating unmanaged risk.

The AR structure can also create governance complexity where roles and accountability are blurred. Staff may assume that the AR owns the customer relationship and therefore the risk, while the AR may assume that the principal’s authorization and framework provide sufficient protection without deeper internal control maturity. That ambiguity is dangerous. The regulatory position is much clearer: the principal remains responsible for the regulated activities of the AR. In a financial crime context, this means principals must be able to demonstrate not only that policies exist, but that AR activity is actually governed, monitored, and challenged in a way that is proportionate to the risk.

There is also an important escalation and exit dimension. If an AR relationship gives rise to persistent file quality issues, weak financial crime controls, unexplained customer risk, or repeated breaches of the principal’s framework, the principal must be prepared to remediate decisively and, where necessary, terminate the arrangement. FCA reporting guidance specifically contemplates AR relationships exited for financial crime reasons, which reinforces that this is not a theoretical possibility but a live supervisory concern.

Ultimately, the Appointed Representative model can be commercially legitimate and operationally effective, but only where the principal treats it as a controlled extension of its own regulated perimeter rather than as outsourced risk. In the financial crime environment, an AR should be understood as a relationship that transfers operational activity without transferring regulatory accountability. That makes principal oversight central. Strong AR governance requires rigorous due diligence, ongoing monitoring, clear reporting, effective financial crime controls, and a willingness to intervene when risk rises. Without those elements, the AR structure can become a channel through which fraud, AML failures, poor conduct, and wider control breakdown enter the regulated environment.